Kaveri posted it’s results and an investor presentation yesterday. Both are on the bse website

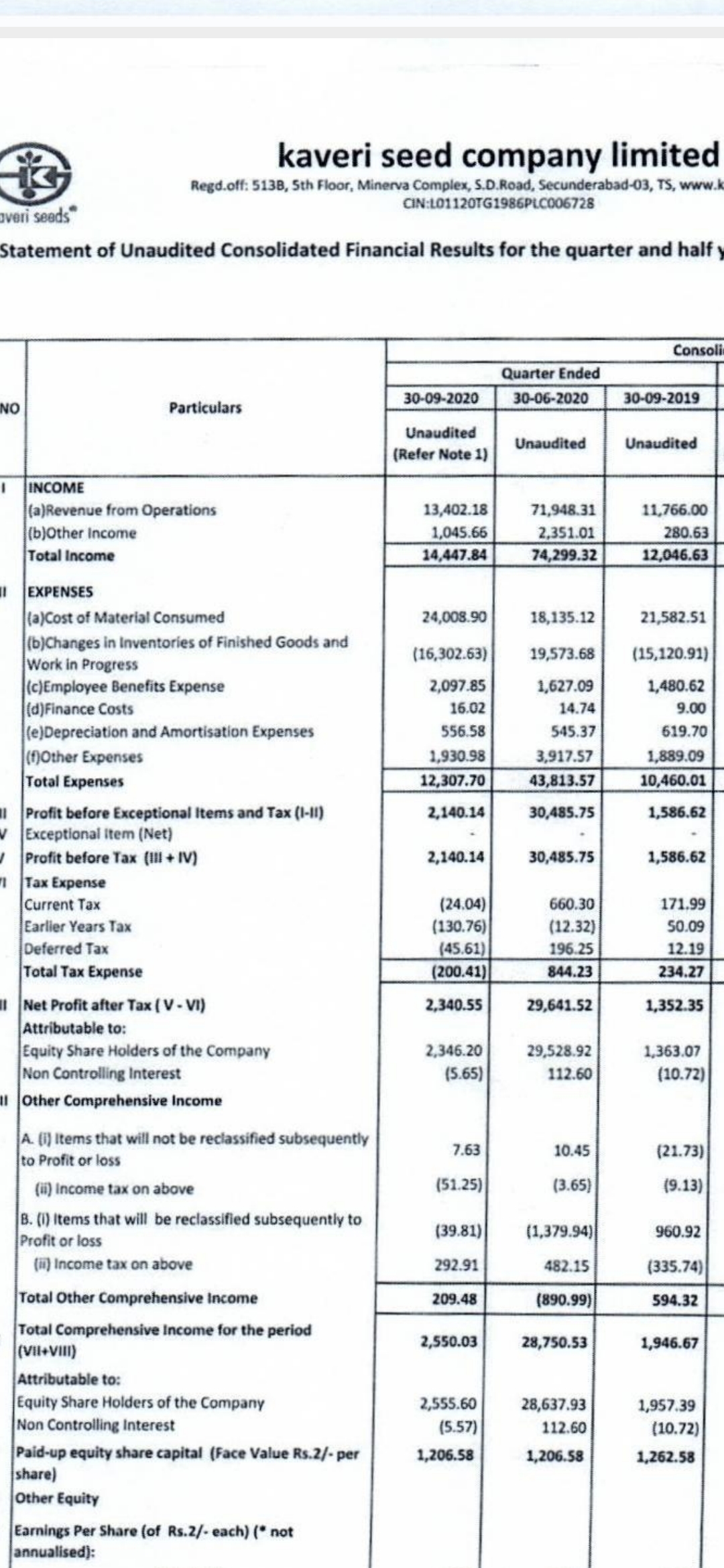

Even excluding other income and deferred taxes everything looks good considering this is usually a weak quarter and there was an increase in employee benefits(what crisis? Haha). Remember that you need to compared YoY and not QoQ due to the nature of their business.

Company has gone a long way from posting losses and poor profits in quarters apart from Q1.

Management was spot on with their commentary and guidance and have been for a few quarters now.

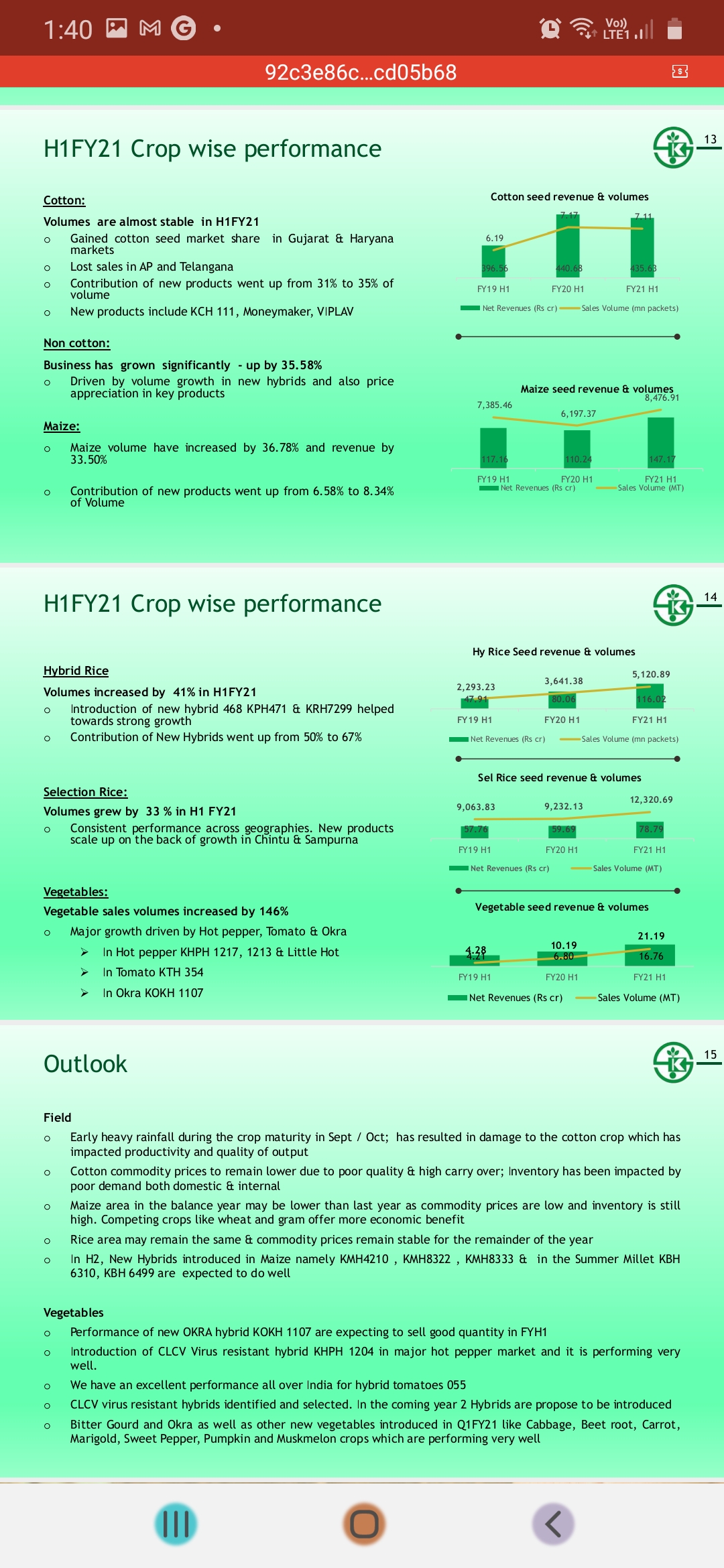

Few hiccups due the late showers in Oct/Nov, issues in Telangana And low pricing of maize and cotton but overall very happy with this especially since they are performing well with these factors against them and could be in for bumper quarters soon. The audit issue may never go away and may even be a non issue now but as long as their earnings keep being this positive then it’s only a matter of time before the market stands up and takes notice.

Other takeaways:

Cash In books 481 crores

Consolidated long term debt decreased from 380 crores to 130 crores

Ebitda Margins have improved substantially to 28 percent from 18 percent which is a godsend for their usual poor quarters(2,3,4) if sustainable

Inventory costs has risen(assuming this is due to the aforementioned issues regards rainfall in sept/Oct , pricing)

Receivables have increased. Hoping we get clarity on both along with the audit during concall(here’s hoping lol)

As a bonus we get rs. 4 in interim dividend. Management promised use of their cash in books for shareholders benefit since not much capex needed to maintain 10 topline and 20 percent PAT growth and This dividend is a good start.

Overall management hasn’t put a foot wrong regards guidance for this H1 and Kaveri looks set to continue growing at 20+ percent PAT with rice and maize as the growth drivers and vegetables finally contributing meaningfully. Add their cash in books and on EPS expansion alone kaveri looks good. Market won’t let these kind of earnings and growth go unnoticed without a re rating at some point either. It’s been a tough few months since June but hopefully patience prevails soon and it looks like there isn’t much downside left considering its currently trading at single digit PE.

Disc: Invested… At CMP(510) we are getting the past H1 results and information without paying a premium for it due to all the mitigating factors of the past few months(Prabhai sale especially) preventing this H1 from being priced in yet

Also, does anyone know if they conducted/are conducting a concall? If so please leave notes. Thanks