So I hold this company in my portfolio, and was also writing a report on it. No better way to start my first post on this forum I guess. I saw a post on it when it was demerging its paints business, but nothing more on the remaining business in the listed company, so here goes.

Kamdhenu Limited is a Delhi NCR based manufacturer of long steel products and construction material. They have been in this business for more than 30 years now. They manufacture Thermo-Mechanically-Treated (TMT) Bars, Structural Steel products (like Angles, Channels, Beams, Flats, Round/Square/Rectangle Pipes) and Color-coated sheets. These are typical products that go into construction. Majority of the business for the company comes from TMT bars only. Company is promoted by brothers Satish and Sunil Kumar Agarwal - with promoter group holding about 49% stake in it.

Now why i like the business (Disc. I am invested in this co.) is because the promoters managed to create a branded, franchisee business out of a pure play commodity business. Since 2004, they have been onboarding independent TMT bar manufacturers as Franchisee Partners, who then manufacture goods under “Kamdhenu” brand name and sell using Kamdhenu’s dealer network. For all this, Kamdhenu in turns receives a royalty based on tonnage of material sold.

Franchisees are happy as they get better capacity utilization and more demand by leverage Kamdhenu brand name and dealer network. Co. also claims that they get a better realization by selling under their brand name. Kamdhenu Limited is happy because it gets to keep the Royalty income, which is pure fee income, with no associated investment in capex/working capital!

Look at the growing royalty income as %age of sales:

| Particulars – INR Crs | FY19 | FY20 | FY21 | FY22 | FY23 | FY24 | FY25 | CAGR |

|---|---|---|---|---|---|---|---|---|

| Royalty Income | 86 | 97 | 88 | 93 | 114 | 129 | 139 | 8.3% |

| Royatly income/Total Steel business revenue | 9.0% | 13.2% | 20.7% | 15.4% | 15.6% | 17.8% | 18.6% |

Overall, the co. claims ~3.5mn MTPA qty of TMT bars sold through this method by the 80+ franchisee partners under Kamdhenu brand name. Co. has a share of ~20% in the small residential TMT bar market (as per co.)

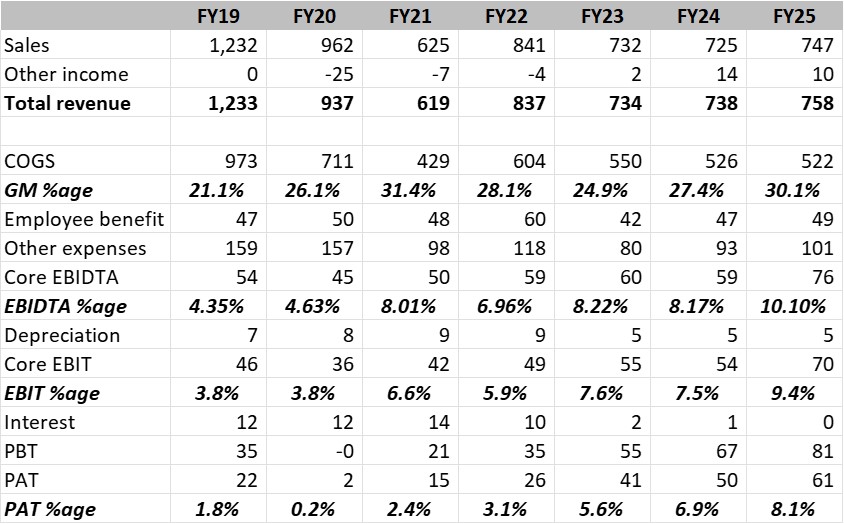

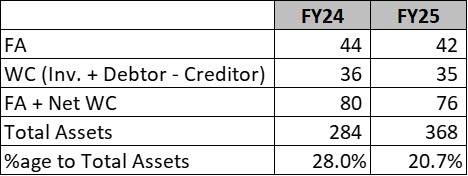

The effect of this unique business model is that the business is capex light, WC light, high ROE and has been throwing out cash.

A few caveats though. Management recently went in for equity issuance (through convertible warrants) to raise ~97 crs (of this, 45 crs already raised upto FY25). Now the company is already sitting on a cash+investment pile of ~206 crs as of FY25 (i.e. ~161 crs pre-fund raise), so it didnt really need to dilute at this stage. More so, when its business doesnt require any major investments. So this is kind of a puzzler for me ![]() . In the past co. had tried entering into other businesses related to construction (including the Paints business, which got demerged into Kamdhenu Ventures) so i hope they are not planning anything new again. But let’s see.

. In the past co. had tried entering into other businesses related to construction (including the Paints business, which got demerged into Kamdhenu Ventures) so i hope they are not planning anything new again. But let’s see.

Also, there had been some aggressive accounting tactics in 2020 leading to Qualified Opinion by auditors (basically booked income from insurance claim of 42 crs pending approval from insurance co., and reported lower expense on ESOPs of ~8 crs - thereby inflated 2020 profit by 50 crs).

Despite the same, there have been no overt leakage of cash, or loans/advances to fund any other related party businesses. And i like the business model, which is a slow and steady compounder as you can see from growth in Royalty income.

Would love to hear any thoughts from other members, and if someone else has studied this business.