Kalyani Steels results out →

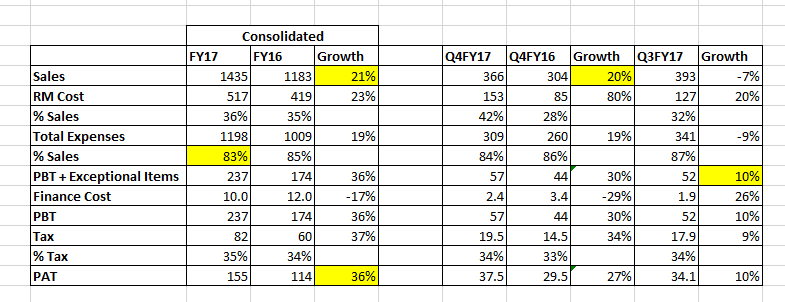

The top line growth is very good and RM cost for full year FY17 is similar to FY16.

Disc - No investments

Kalyani Steel

CMP: 413 MarketCap: 1808.11 crore

Kalyani Steels Limited is a part of the Kalyani Group. It is a leading manufacturer of forging and engineering quality carbon, and alloy steels using the blast furnace route. It caters to engineering, automotive, seamless tube, foundry and casting industries along with the primary aluminium industry. It is a quality supplier of steel to engine components like crankshaft, camshaft, connecting rods, axle beams, steering knuckles and bearings. In the energy sector, it caters to the players who manufacture seamless tube applications for high-pressure boilers, oil lines, casing and tubing, pipes for oil exploration. The Company is also a certified supplier to the Indian Defence and supplies steel for bombshells, and barrel applications for heavy vehicles.

Recent Financial Performance

- For Q4 FY 2017 Revenue grew at 20.43%, stood at 365.89 crores as against 303.79 crores in Q4 fy 2016.

- Net profit grew at 28%, which stood at 37.25 crores as against 29.09 crores.

Yearly numbers (in crores) Mar-15 Mar-16 TTM

Sales 1,227.01 1,180.47 1422.29

Expenses 1,059.52 945.19 1135.64

Operating Profit 167.49 235.28 286.65

OPM 13.65 19.93 20.31

Other Income 2.33 2.66 13.11

Interest 14.77 12.03 9.63

Depreciation 31.02 51.73 51.97

Profit before tax 124.01 174.19 238.17

Tax 40.71 60.61 82.24

Net Profit 83.31 113.58 155.92

EPS (unadj) 19.05 25.97

Quarterly Numbers in crores Mar-16 Jun-16 Sep-16 Dec-16 Mar-17

Sales 301.83 344.97 330.19 391.48 355.65

Expenses 239.77 257.88 257.23 325.52 295.01

Operating Profit 62.06 87.09 72.96 65.96 60.64

OPM 20.56 25.25 22.1 16.85 17.05

Other Income 1.97 0.9 0.65 1.33 10.23

Depreciation 17.04 13.64 13.24 13.28 11.81

Interest 3.42 3.02 2.36 1.88 2.37

Profit before tax 43.56 71.32 58.01 52.13 56.71

Tax 14.46 24.52 20.41 17.86 19.45

Net Profit 29.1 46.8 37.6 34.27 37.25

Manufacturing unit:

- KSL is a Pune-based company having steel mill at the strategic location of Hospet, Karnataka with hot metal capacity of 2,90,000 TPA.

- KSL has also a locational advantage as the southern region is a burgeoning automotive hub and Karnataka is rich in iron ore.

- KSL also benefits from adjacent Mangalore port for imports of other raw materials. End of MIP on steel products will lower operating costs: With minimum import price (MIP) a history now, KSL will benefit from cheaper imports in terms of iron ore which is its raw material. This will lead to improvement in profit margins for the company.

- An improvement of at least 500 bps in EBITDA margin is possible due to cheaper imports. However, one has to factor in the rising coking coal prices, which may offset the benefits accruing from lower iron ore prices.

Clients: - KSL benefits from its parentage in terms of access to steady clientele. Kalyani Group has joint ventures with Bharat Forge, Automotive Axles, Kalyani Hayes Lemmerz and Kalyani Carpenter Special Steels. KSL caters to all business requirements of these JVs through backward integration.

- KSL’s client list includes players from automotive, energy and aluminium smelting segments such as Eicher Motors, Hyundai, Force Motors, Tata Motors, Maruti Suzuki, Renault, Nissan,Mahindra, Volvo, Eaton, AMW, 7F India, BHEL, Jindal Saw, MSL, UST etc.

- KSL is also a supplier to the Indian defence segment and can benefit from the expansion in defence budget.

Key Growth Drivers

- India is the third largest producer of crude steel across the globe, and the growth in the Indian steel sector has been driven by the availability of raw materials such as iron ore and cost-effective labour. This should help Kalyani steels to increase their production and meet the growing global demand for crude steel.

- The Indian steel industry is upgraded with the latest technology with state-of-the-art steel mills. Such development will provide the Company the opportunity to capitalise on the new market requirements.

- Steel consumption in the country is expected to grow 5.3% y/y to 85.8 metric tonnes during FY 2017, led by a growth in the construction and capital goods sector.

- The Central Board of Excise and Customs (CBEC) has issued a notification announcing zero export duty on iron ore pellets, which will help the domestic industry become more competitive in the international market, and will further help in increasing the export orders.

- India is expected to become the world’s second largest producer of steel in the next 10 years, as its capacity is projected to increase to about 300 metric tonnes by 2025.This growth opportunity is offered by India’s comparatively low per capita steel consumption and the expected rise in consumption, due to increased infrastructure construction, thriving automobiles, and the railway sectors.

Technical:

Disc:

Invested

Does anybody know any details about 136 cr worth Non-Current Investments in 13,196,000 0% Fully Convertible Debentures of Rs.100/- each of DGM Realties Pvt Ltd?? What does the company derives from this Investment??

There is one another company called DGM Property Solutions. Are they both same companies??

Yes, this has been a negative. Seems like bad capital allocation. The investments seem to be in groups unlisted real estate business and the listed company hasn’t got any return on this investment

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=366e2f7f-f063-4cf8-b52a-e9acd5edcaef

Results out…

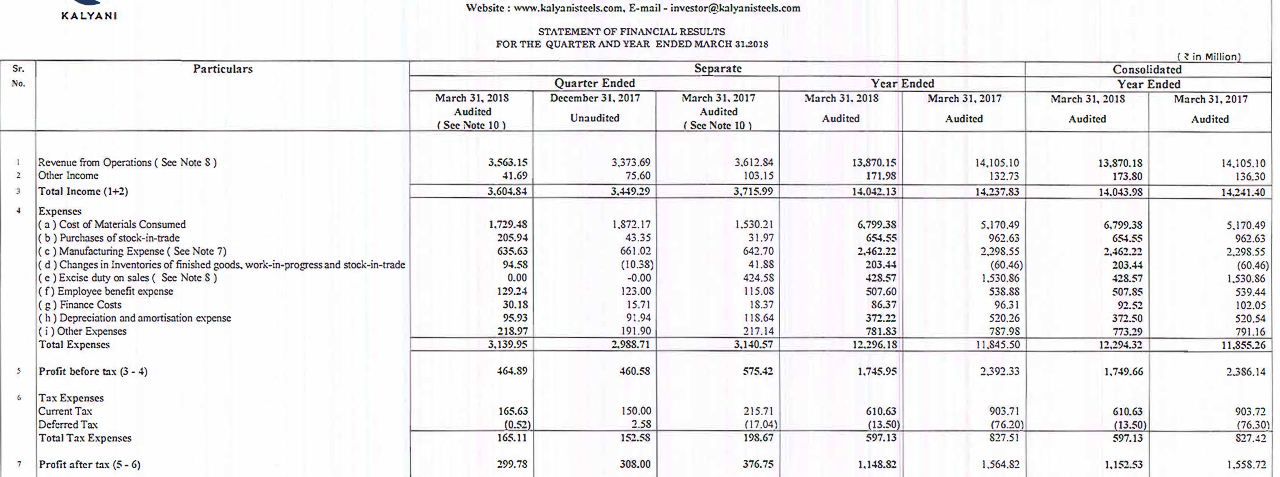

Kalyani Steel FY18 Annual Report Notes

- During the Financial Year ended 31st March, 2018, the Company achieved Revenue from Operation of

13,870.15 Million against14,105.10 Million in the previous year. The Profits before Tax is1,745.95 Million, against2,392.33 Million in the previous year. - Cost of key raw materials such as Iron Ore, Coke, Electrodes, Refractories etc. has increased substantially, however there was a delay in accepting such increased costs by our customers, which resulted in comparatively lower profits. Secondly in view of the reduction in margins for sale of Pig Iron, the Company sold 4,095 tonnes of Pig Iron as compared to 26,686 tonnes in the previous year. Gross margins declined from 51% in FY17 to 43% in FY18 in the period when other players in the industry expanded their margins.

- Revenue from Operations is Rs. 13870 mn, it includes Manufacturing Revenue of

13,000 Million, Trading Revenue of675 Million, and other Operating Revenue of ` 195 Million. - Manufacturing Revenue consists of sale of Rolled Products, As Cast Blooms and Rounds and Pig Iron. The Company sold 234,989 tonnes of Rolled Products aggregating

12,215 Million, 14,533 tonnes of As Cast Blooms and Rounds aggregating679 Million, 4,095 tonnes of Pig IronÊ aggregating106 Million. The Manufacturing Turnover includes exports of 5,568 tonnes of Steel aggregating584 Million. - The Company has chalked out clear road map for Approvals and New Product Development with major OEMs in Domestic and International spaces. The Company has continued focus on niche segments such as critical components in Automotive and Engineering, where the product range is less susceptible to global market fluctuations.

- Forex earned Rs. 58 cr. and Forex used Rs. 398 cr.

- Reduced borrowings from Rs. 238 cr to 168 cr. Most of the cash earned in the past 3 years have been used to reduce debt and increase financial investments. Company has financial investments and Cash of Rs. 151 cr, that makes the company almost debt free.

- Cash equivalents of Rs. 151 cr and investment in realty firm of Rs. 153 cr, thats total of Rs. 304 cr out of total asset size of Rs. 1278 cr. A very high 24% of assets is earning very low return.

Some Steel Industry Trends mentioned in the AR

- As per World Steel Association, crude steel production in India increased by 6.2% in 2017 as compared to 2016, from 95.5 mntn to 101.4 mntn.

- It is interesting to note that in 2017 India clocked the 3rd highest growth in crude steel production among major steel producing countries after Turkey (13.1%) and Brazil (9.9%).

- On the steel consumption side, India’s finished steel consumption increased by 4.4% from 83.5 Million Tonnes in 2016 to 87.2 Million Tonnes in 2017.

- Going forward, India’s finished steel consumption is expected to grow to 92 Million Tonnes in 2018 and 97.5 Million Tonnes in 2019 showing 5.5% and 6.0% growth in 2018 and 2019 respectively. However, even stronger steel demand growth may be seen when private investment cycle kicks in.

- Increasing Iron Ore prices : NMDC increased the floor prices of Iron Ore Lumps* & Fines* by 31% and 23% respectively between April, 2017 and March, 2018. Such steep increase in Iron ore price has severely affected Karnataka steel industry.

- Between April, 2017 and March, 2018, the CFR India LAM Coke prices have increased by around 12%, which directly affected steel companies not having captive coke ovens. Further, in November, 2016, the Department of Commerce had imposed an anti-dumping duty on Low Ash Metallurgical Coke at 25.2 USD/T and 16.29 USD/T for imports from China and Australia respectively. Such anti-dumping duty coupled with rising global Coke & Coking coal prices has severely affected Indian steel Industry.

- It is pertinent to note that even though there were various talks of China cutting its steel capacity, in reality, the Chinese crude steel production has increased by 5.7% in CY 2017.

Steel sector has been hit hard lately due to the China Virus issue.

But more of concern is the fact that they were to announce dividend on 27th February. company has not announced anything as of today( no updates at all). Why has SEBI or stock exchanges not asked for clarification?

Why can this happen?

Hi,

The dividend declaration was to be through “circular resolution”. The board members will be sent the resolution through email and their approval will be taken. it takes couple of days to receive approval/disapproval from each board member. You should get announcement of result by next week.

There is no board meeting for a single agenda item, it saves company’s time and resources…

Company is the best in specialised steel sector . .

The announcement clearly mentioned board meeting intimation. Hence the questions.

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=ebb0ba77-a3f2-4c63-a948-17d6b9f75128

Extremely good results from Kalyani steels on both QoQ and YoY fronts. With Buoyancy in Auto sector, tractor/farm equipment and Infrastructure sector the good show should continue in future also. North America’s Class 8 trucks bumper demand should keep the demand high from forging companies. 4637833e-4bd6-44e0-89f7-aefd6c04fc54.pdf (2.4 MB)

Kalyani Steel’s backward integration capex of 210crs (coke oven with waste heat recovery plant) is next critical milestone. Commissioning in Sept 2022. Presume a 3 year payback is possible like kirloskar ferrous so incremental ebitda of 70crs. 260crs current ebitda is higher than long term median but might sustain in current conditions. So 330crs ebitda Fy24. 1700crs mcap and 400crs cash. Upside possible but need more growth capex for big upside.

As per the latest interview:

Management is looking for big Capex.

Requesting the esteemed members to please elaborate on the impact this investment may have on the KSL.

-

Will need to add rolling equipment. To produce 3.5 Lakh Tonnes of green steel. Will be investing 5000-6000 crores.

-

Will be 1 million tons overall capacity of steel by FY27.

-

50% of capacity supplied to bharat forge which is looking to expand revenues.

-

Note: Company converts steel to semi-finished and finished forging and machining components used in Auto comp, oil and Gas and Industrial manufacturing.

-

So this will be backward integration for them.

-

EC will take one year. Funding plans EC is received.

-

But the important factor is setting up of Titanium metal plant in Odisha for defence and aerospace industries.

-

Total Revenue to be approx 7500 crores on incremental capex of 11750 crores with 20% editda margins by FY28.

Disc: -1% of PF. Looking to add if CMP drops below 700.

Hi,

As we all know KSL has acquired Kamineini’s plant for Rs. ~450 cr which has capacity of 350,000 MT.

On Kamineine’s website it is mentioned that they manufacture Billets:

If my understanding is correct, Steel Billets have realization of ~Rs. 40-45,000/ MT, right or am I wrong?

KSL’s current realization are almost Rs. 75-77,000/MT

| (All Rs. In cr) | FY22 | FY23 | FY24 |

|---|---|---|---|

| Total Revenue (Rs. cr) | 1,706 | 1,899 | 1,959 |

| Total Volume | 2,28,578 | 2,45,364 | 2,47,500 |

| CU% | 91.4% | 98.1% | 99% |

| Blended realization (Rs/MT) | 74,635 | 77,395 | 79,152 |

| RM Cost (Rs. cr) | 967.3 | 1185.0 | 1120.8 |

| RM Cost per tonne (Rs/MT) | 42,317 | 48,294 | 45,285 |

| Gross Profit per tonne (RS/MT) | 32,319 | 29,101 | 33,867 |

| EBITDA (Rs. cr) | 338.6 | 245.7 | 371.0 |

| EBITDA per tonne | 14,812 | 10,012 | 14,988 |

I have 3 questions from this:

- Will KSL sell commodity Billets from Kamineini’s plant or Carbon/Alloy it after processing?

- What could be the realization and EBITDA/MT of Kamineni’s products?

- Is Kaminein’s entire capacity available for production or actual utlization would be lower because the plant is old?

Would be great if anyone tracking thye Co. closely could enlighten on this. Thanks

So they are redoing the entire plant. Their intention is to produce HR Coils and preferably be a green steel plant.

The company is bought mainly to get the linkages, land and also available permits. They are not going to sell billets.

Listen to the videos I have posted above. Gives an accurate summary of management thought process.

Thanks for the info. Do you believe that plant will become operational anytime soon? The management has been pretty vague on this.