Kalpesh I like to request you to kindly have a look at sree royal seems hy strength hypo Ltd and share ur thoughts there is seperate thread for that u can kindly post it there or here

Both Sree Rayalseema Hypo & TGV Sraac Ltd are interesting companies, Will look at them as and when time permits.

2 Likes

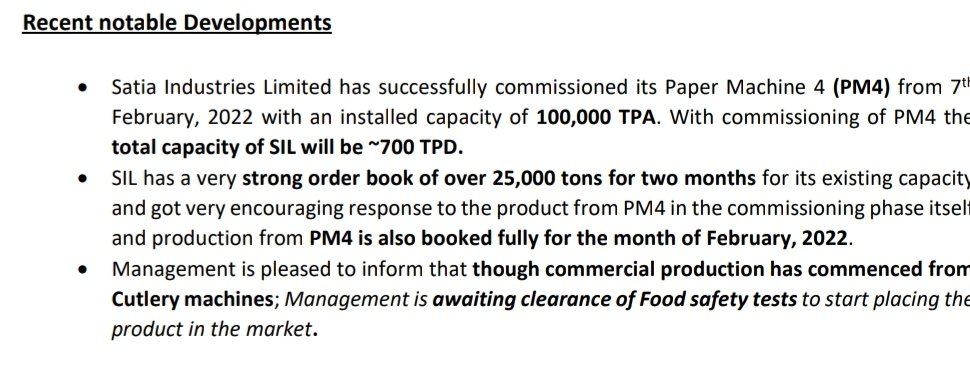

#SatiaIndustries

Interesting developments shared by co in release.

New PM4 machine already fully booked for Feb given the strong order book.

Cutlery commercial prod started, co awaiting clearance of food safety tests

Strong growth trajectory ahead

3 Likes

2 Likes

If you understand Hindi, then please go through Satia Industry Q3 earning call.

Mgmt has clearly explained the industry dynamics.

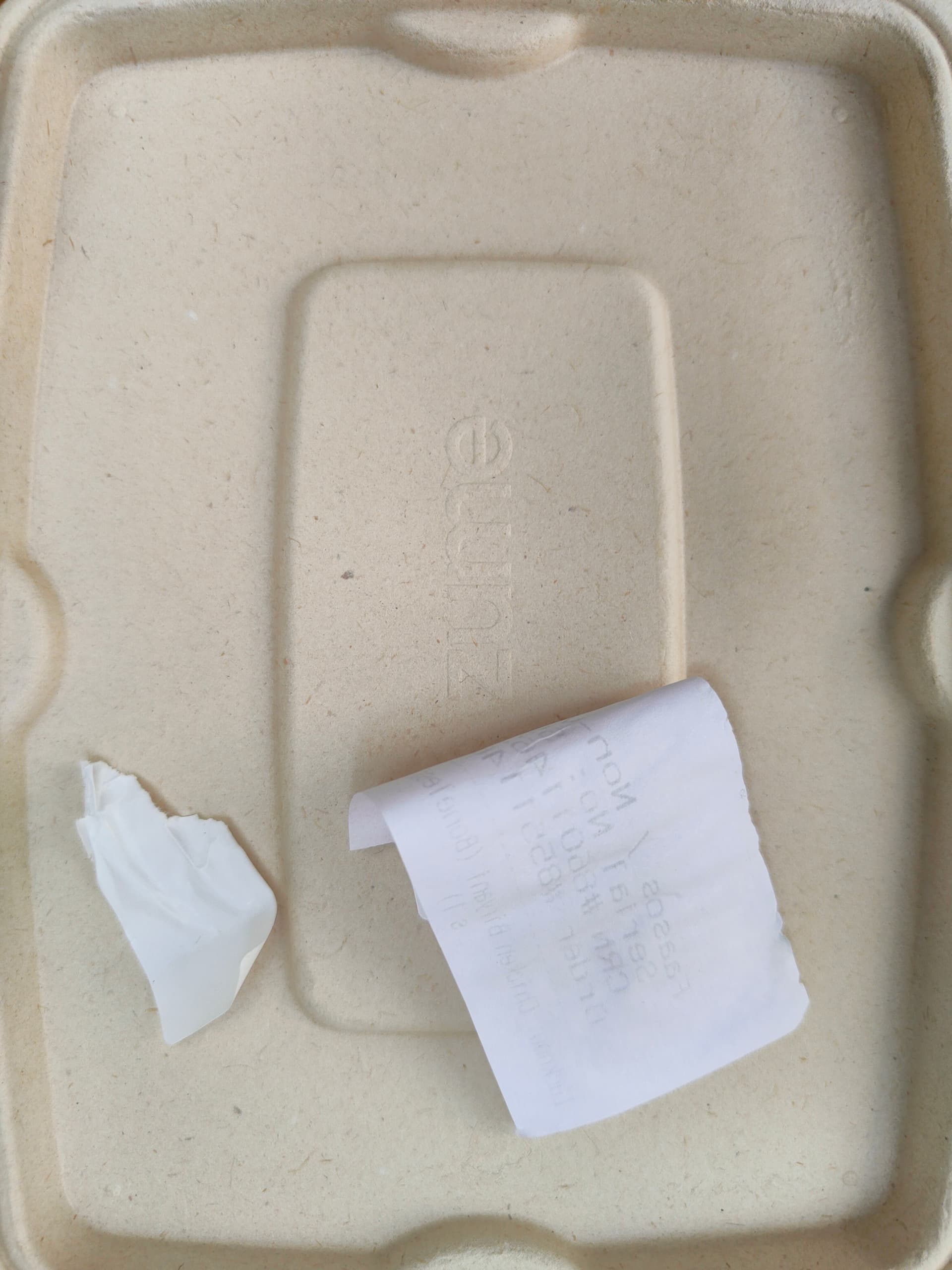

Ordered Food Online in Banglore . Came in a Zume Packed Box probably made by Satia Industries since it is the only Partner in India. It is a good Product and can easily replace Single used Plastics.

5 Likes

In the concall last week they said they don’t have all clearances yet to sell cutlery (FSSAI verdict was awaited on Feb 17th)…are you sure are exclusive suppliers to Zume in India? I ask because I see Zume products on Amazon with product reviews dating back to 2021.

I don’t have that information whether Satia is sole Provider for Zume or not but on their Website in India it is only showing Satia Industries. It maybe the case that the box they are selling now are imported and they have a local vendor satia also so, if satia starts manufacturing the price may go down since on Amazon it is expensive now.

2 Likes

What I think is Satia is sole manufacturer in India not sole vendor,

Zume will divert all future supplies through satia due to cost efficiency.

3 Likes

No, satia is not sole manufacturer or vendor for Zume in India.

They had mentioned it in 2-3 quarters back .

They also have Parason as Indian manufacturing partner. This product is available on Amazon India as well. Mentioned there that manufacturer is Zume India but country of origin is Thailand…confused…

Mr. Vaibhav Goel, Managing Director, APAC & EMEA, Zume Inc.

See they have many distributing partner, but manufacturing partner is only Satia in India at the moment,

Parason is Aurangabad based company, who manufacture paper & pulp machinery, not paper & pulp as product.

UBS estimates the global food delivery business is estimated to grow more than ten times, from USD 35Bn in 2018 and is projected to reach USD 365Bn by 2030. This has motivated Zume to create a first-of-its-kind, and plant-based compostable packaging that matches the performance of plastic, but comes at a lower cost

7 Likes

1 Like

Looks like Parason makes machinery for pulp for other manufacturers, not the actual product/pulp or paper.

Now a days seeing on twitter & Valuepickr that lot of investors are buying stocks solely based on capacity expansions by companies.

I feel this is not proper way to invest.

Investor should also seek below information -

- Is the company posses any advantage over peers? Doing things differently than peers?

- Is management capable to sell expanded capacity?(irrespective of macro conditions in future)

- Management taking decisions based on facts/data? or copying peers?

- Is management rationally allocating capital, energy(focus) and other resources in right direction?

- Investing by ignoring valuations?

- Using PAT to decide valuations? which is a wrong in my opinion

In my opinion investment decisions(Both buy & sell) should largely be dependent on rationality of management & valuations at that point of time.

all other factors are also important, but these two are above all.

Only thing important than these two is fine tuning investors own behavior to face market psychological forces in a right way.

Thanks!

10 Likes

Can you please elaborate on Point 6?

Thanks.

This all behaviour are part of stock market cycle untill capex will become a debt trap for some companies and death trap for some companies.

Although your observation will help investor to choose better company.

Thanks

1 Like

PAT is an accounting profit, it’s illusion.

read my previous posts -

1 Like

Hi @kalpesh4430 thank you so much for your views. I just wanted to ask your opinion on satia underperforming in recent paper rally compared to other players such as JK paper. Will the fact that satia uses waste paper as 25% of RM impact it’s margins a lot or will price increases be enough?

2 Likes

Hello @Investor1234,

I see two reasons for that,

- Their 40-50% revenue comes from state boards, which have existing contracts at previous prices, which will renew may be in 2-3 months, so effect can be seen in first qtr of FY 2023

- Imports are 25% of RM as on now, which will reduce in the future. effect can be seen may be 4-6 months later.

Satia is in completely different league than other big players, so can’t expect price to behave in same way.

5 Likes