-

Jyoti CNC Automation Limited is one of India’s largest CNC machine tool manufacturers.

-

The Company’s range of products that includes CNC Turning Centres, Turn-Mill Centers, Vertical Machining Centers (VMC), Horizontal Machining Centers (HMC), and advanced 5-axis Machining Centers, along with solutions for Industry 4.0 and Artificial Intelligence (AI).

-

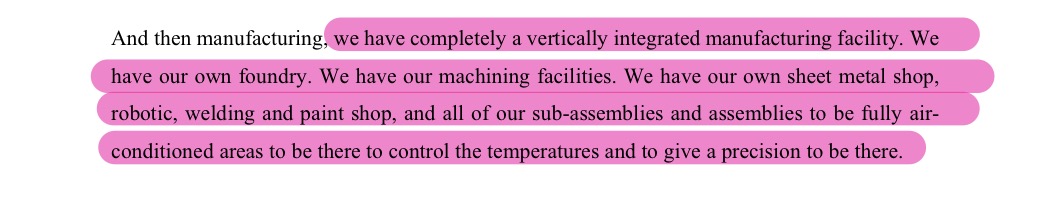

Vertically integrated company with in-house manufacturing of machine components such as spindles, tool-changers, pallet changers, rotary tables and universal heads in-house. The company has its own R&D Centers, Foundry, Machine Shop, and Sheet Metal Unit. Also has in-house design capabilities.

-

Focus on R&D with dedicated R&D facilities at Rajkot and Strasbourg.

-

diverse customer base. Some of the marquee customers include ISRO, Brahmos, Harsha Engineers, Bosch, Tata Advanced Systems etc.

-

Exports constitute ~ 40% of revenue.

-

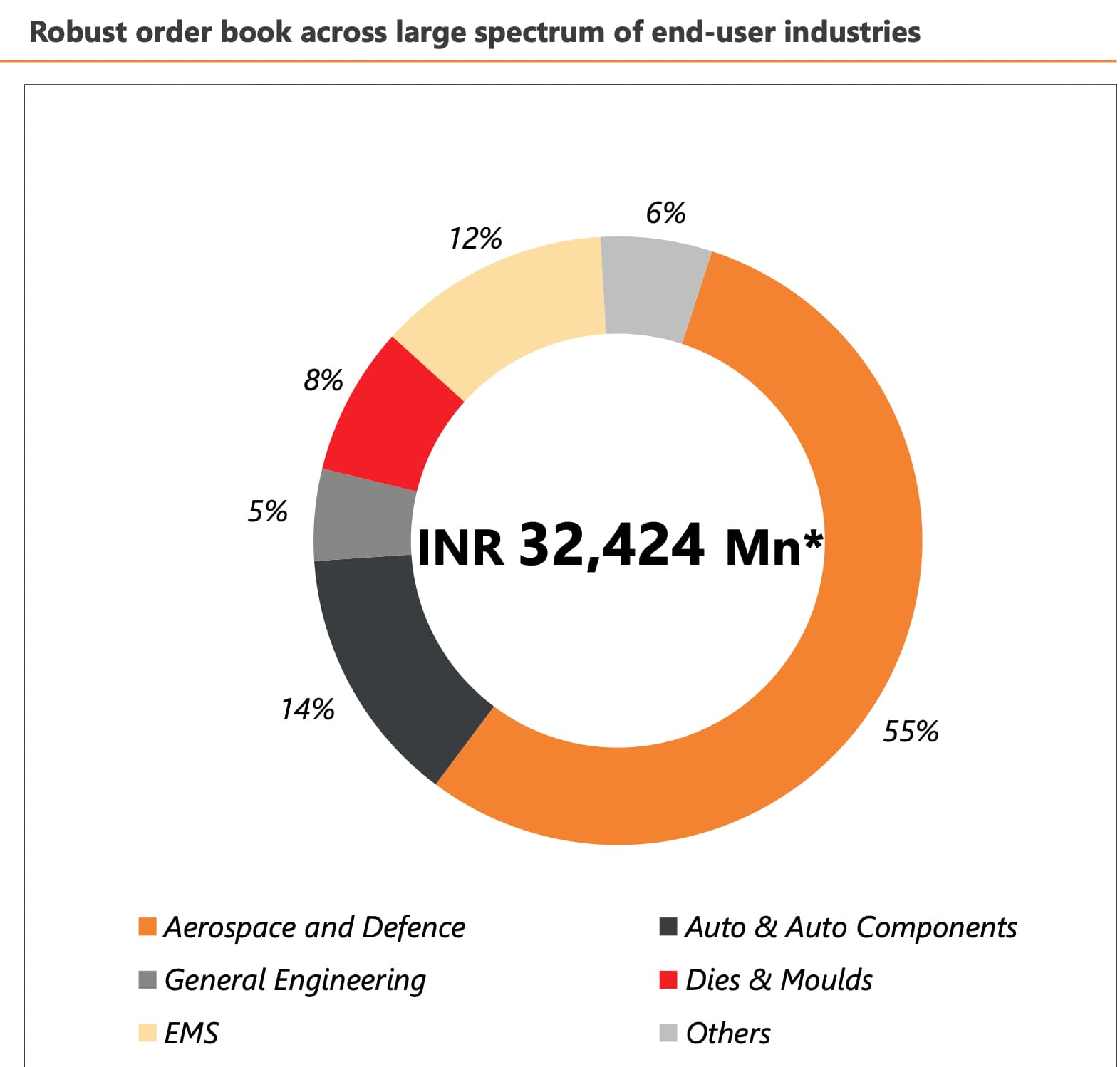

Catering to Aerospace, Defence, Auto, EMS, Dies and Moulds and General Manufacturing Industry

-

Orderbook as on 31 Dec 2023:

-

Vertically Integrated Company

Industry Size:

-

As per management, India consumed $3 billion worth of CNC machine last year (approximately 24,000 crore). of this 65% was imported while 35% was domestic over the next 5–7 years the consumption is expected to grow at 20%.

- The company eyes that the proportion of imports will decrease in the next 5-7 years that is import substitution is likely to happen. Secondly, the market itself is growing at 20%.

-

85% of the total market is metal cutting and 15% metal forming. Jyoti CNC status metal cutting

-

Overall market the entry level is domesticated 80–85% is domestic while in high end machines 90% is imports. the company is focusing on this high end of the market, where competition is mainly from Germany and Japan.

-

The Company operates in a niche growing sector. But a good business is not always a good investment if the valuation is not in favor.

Crude Valuation:

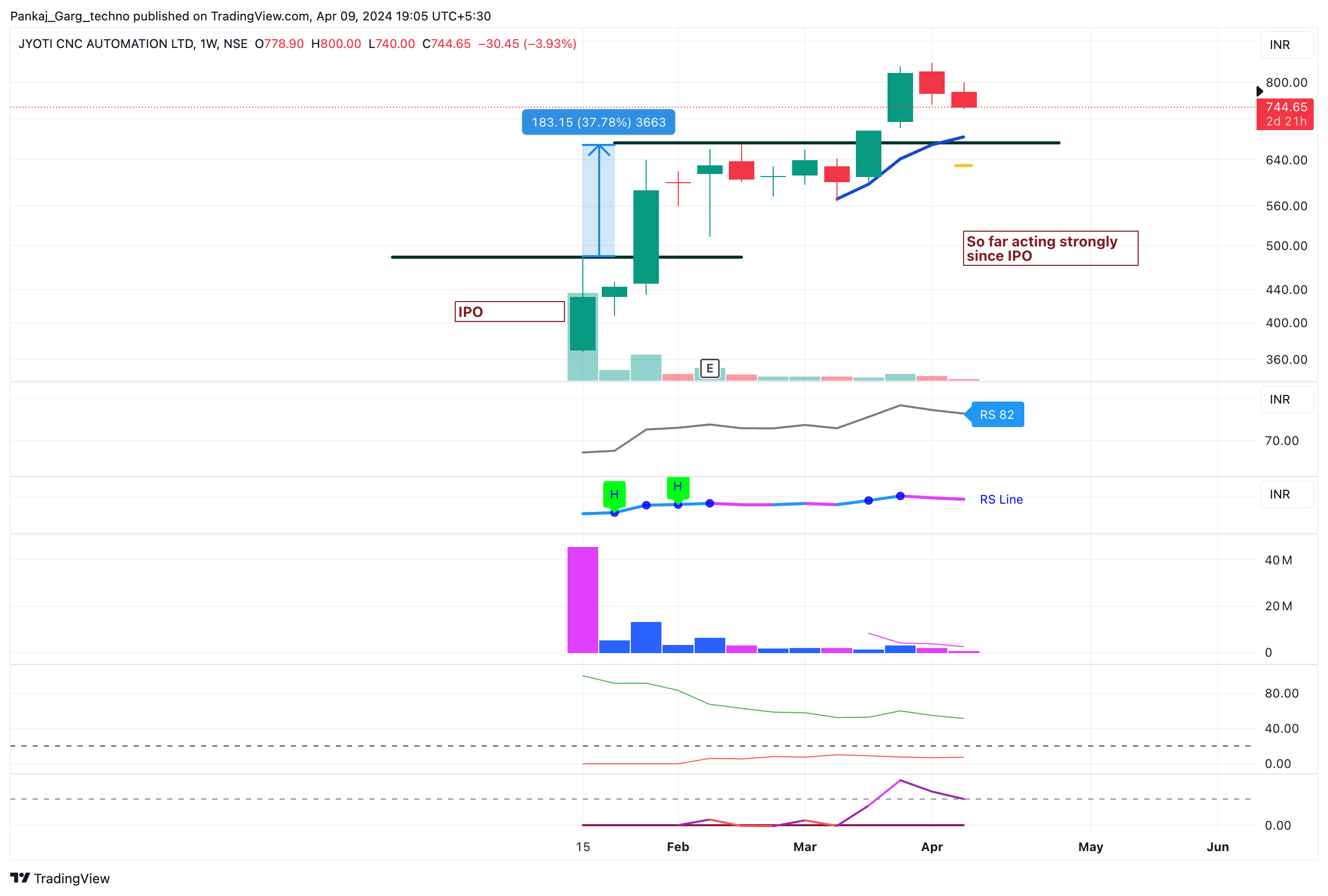

Last Quarter EPS of 2.44. If we assume this is the run rate then full year eps comes out to be approx 10 i.e. on PE basis it is valued at 75X i.e. a lot of growth is already priced in.

The main risk in my opinion is the execution risk i.e. whether their products will find traction among manufacturers pitched against tried and tested suppliers from Japan and Germany.

I think this is a good stock to discuss on this forum

Disclosure: Tracking position