Hi friends, this is my first post on this forum. Invite your comments, feedback and suggestions to improve the quality of write up.

Disclosure : Hold 5% of my portfolio since past 3-4 yrs

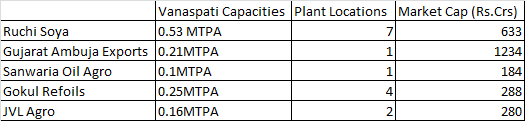

Business : JVL Agro Industries Ltd manufacturers Vanaspati (hydrogenated veg oils) and refined edible oils. The companyas flagship brand Jhoola is a market leader in UP and Bihar and overall, it has presence in 18 states and 2 union territories. Its manufacturing plants are located at Naupur & Varanasi (UP), Dehri-on-sone (Bihar), Alwar (RJ) and Haldia (WB). While its last year growth is nothing to talk about, what catches attention is the available cash per share.

From where further growth will come : The company intends to become a food products company from an edible oil company and has taken some steps in this direction :

1). The company plans to set up edible oil refineries in North East (70 MTPD) and Gujarat (1000 MTPD) and has identified locations / land parcels to be purchased

2). It plans to launch branded rice in 3rd quarter of 2014-15. The rice mill with capacity of 60000 Tonnes per annum is being established in Bihar

3). It is promoting an 80 acre Mega Food Park in Bihar - which it expects a will emerge as a hub for farmers, processors and downstream users coupled with adequate financing, warehousing and other support facilities

4). The present Operating margins are very low at 1.5 to 2.0% for last two years. The company plans to increase the same to 5% over next 3-4 years by following dual approach of : (i) Launching premium product categories and (ii) Leveraging Govt subsidy schemes by making investments in green field projects

5). It is already producing bakery products (bakery shortening agents)

Valuation : As per AR 13-14, the turnover has grown by 14.8% over previous year (5 yrs CAGR of 37%), and the net profit has grown just by 1.47% (5 yrs CAGR of 20%). While there is nothing special to talk about the present growth rates, the company appears to be a probable candidate for re-rating based on following :

1). As per AR 2013-14, it has got cash & bank balances of Rs.439.41 Crores (excluding inventories & receivables). This is Rs.26 cash per share. With CMP of Rs.20, the rest of the business is available for free.

2). For a 4800+ Crore FMCG company, the valuations appear cheap with PE of 5 and Mkt Capt to Sales of 0.07

3). The company is based in Varanasi which is a chosen constituency of Prime Minister Mr Narendra Modi. The city ranks high in the agenda of smart city projects. In fact, after this news, the stock has already rallied from 15-16 to present levels.

Concerns :

1). The company has signed MoU with UP Govt to invest 2200 Crores. Details are not available as to how the company plans to raise this money. (http://www.business-standard.com/article/pti-stories/investors-ink-mous-to-invest-rs-60-000-cr-in-u-p-114061201104_1.html)

2). The company has set up a cement unit at Rohtas, Bihar, which is a totally unrelated business