Hi, do you mind sharing the calculations as well?

Just Dial Cal.xlsx (42.4 KB)

It is a simple straight-line projection. It could be improved by actually calculating the full P&L for all 20 quarters.

isn’t Web Search undergoing a fundamental shift due to AI?

Lots of Site traffic will be illusory now because its the AI agent visiting the sites and the impressions will no longer be the same. It feels like your thesis is not factoring in the possibility of any potential disruption.

The one thing is certain, the next five years are going to be radically different than the last five.

1 Like

You are right, @StonePitbull . That’s why I was looking at their mobile app traffic.

While 85% of their traffic is from mobile (web and app), we can assume (50% of that 85%) will be from the mobile app. This estimate is based on my working experience with apps like Ola, Redbus, MMT, and Unacademy. And this will grow as their brand search remains the same.

Brand search → App install → App retention ->. Increase in the app user base

And app traffic is more captive than web traffic and will be disrupted more slowly. Based on their annual report, their mobile(app+web) traffic as a percentage of overall traffic is increasing YoY for the last 5 years, and the cumulative app installs are growing. I considered this.

However, I am fully aligned with your thought that, in the next five years, things will be radically different from the last five. In five years, there may be a scenario where we have no apps, no browsers on our phones, and only one AI customized for each of us, which handles actions such as food ordering, ticket booking, local searching, and deciding where we should go. This is possible.

If this happens, JD, Swiggy, Zomato, MMT, etc. will become irrelevant.

I assume that even in this case, they will have enough cash(in the tune of the current Mcap) by then to give it back to the investor from JD. So the downside is somewhat protected.

4 Likes

justdials todays marketcap is less then 7000 cr..cash by end of this yr if they dont distribute dividend will be about 5900 cr, so basically we r getting justdial at 1100 cr market cap and there ebitda itself will be approx 350 cr for this yr..I dont understand why parent is not taking any descisive actions in favour of shareholders?

last concall they mentioned will be doing qtrly calls but didnt do, since many qtrs we r hearing abt dividend policy but still no action,

its a business where there is no credit to customers infact they collect full money in advance, zero baddebts, no need for big capex, no factory, no machines, no inventory issues, difficult to understand in todays world when new age tech companies making losses or minimal profits are trading at crazy valuations and here is a company with strong moat, available at single digit pe.

Investors, big institutions are just waiting for 1 positive trigger may it be dividend or buyback or some m&a.

disclosure : invested so my views may be biased

5 Likes

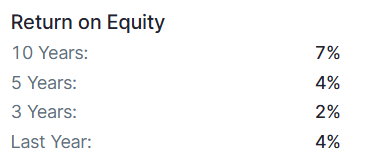

Why are they not distributing the cash to minority shareholders in terms of dividends or buybacks? They are acting like a holding company instead. Too much of a cash in the balance sheet becomes liability when there is no clear plan to use the cash or distribute to shareholders. Also, for a company with such less Capex and OPEX requirement, the returns are very poor. Below are the details from screener:

What could be the reason for such poor return rations? If the management is so oblivious of shareholders, the price is not going anywhere in the near future.

your roe calculation is not correct

for fy23 roe was about 4.5%

for fy24 roe 9.5%

for fy25 roe is 13.5%

so its continously increasing in past 3 yrs but nothing to cheer about its mainly due to other income.

2 Likes

this is the beauty of our stock market.

since long time i am very much optimistic about this comopany, they have everything!

they can enter in many new verticals parallel with their existing business model. Quick commerce losss makers commanding valuations equal to dmart, then why not Just dial?

may be because of ambanis interest… !? then why reliance bought this company?

Disc, sold 3 months ago.

We have carried out a detailed research study on Just Dial Limited covering its business model, platforms, financial performance, operational metrics, and future expansion plans. Sharing the analysis here on ValuePicker purely for healthy discussion and knowledge sharing with fellow members, and not as any investment advice or recommendation.

Just Dial Limited, a company founded in 1996, is India’s premium local search engine offering services on several platforms like website, mobile site, applications on Android and iOS, voice 88888-88888 and SMS. The company has transitioned from a basic local search provider over the years to a facilitator of transactions with the introduction of services like Search Plus, JD Omni for SMEs, JD Pay for online payment, and JD Social as a platform for sharing curated content. Its purpose is to deliver quick, free, credible, and complete information to users and facilitate discovery and transactions in products and services.

The business model at its core follows a scalable prepaid model wherein revenues are largely driven by advertisers operating paid campaigns. Advertisers choose between premium and non-premium packages differentiated by business category and geography. Advertisers can pay upfront or month-to-month, and add-on services like banners, custom sites, JD Pay integration, and review tools offer additional monetisation options. The organisation offers a compelling value proposition to MSMEs through facilitating strong online presence, cataloguing, offers and vouchers, and analytics, as well as serving national advertisers with multi-city campaigns.

Key Q1 FY26 operating metrics reflect the ongoing mobile trend. The platform saw 19.32 Cr unique visitors, a YoY growth of 6.6%. Mobile generated 86.9% of traffic with 16.79 Cr visitors, and desktop contributed 1.94 Cr and voice 0.59 Cr. Mobile downloads were at 4.07 Cr, showing increased engagement, as the voice channel continues to experience structural decline even while recovering quarterly. The firm’s database grew to 4.97 Cr listings with geocoded listings at 3.48 Cr improving on location-based precision. Paid campaigns totalled 617,340, and user reviews hit 15.37 Cr, reflecting strong community involvement.

From a financial perspective, Just Dial posted operating revenue of ₹297.9 Cr for Q1 FY26, a 6.2% YoY growth. Adjusted EBITDA stood at ₹86.5 Cr with a margin of 29.0%. Other income was a major contributor at ₹127.3 Cr on the back of treasury MTM gains, leading to net profit at ₹159.6 Cr, a 13% YoY growth. Though the profitability is sensitive to the fluctuations in treasury income, employee expenses constituted the majority of operating expenses at 60.4% of the revenue. The balance sheet is strong with ₹5,429.8 Cr of cash and investments and ₹534.6 Cr of deferred revenue.

The price chart shows mixed performance over different timeframes. The 1-year CAGR is -29.0%, reflecting a steep correction after the sharp rally seen in FY24. However, over the 3-year period, CAGR is +14.3%, and the 5-year CAGR is +16.8%, indicating that despite recent declines, long-term investors still gained healthy returns driven by earlier upswings.

The PE chart shows a sharp derating: from extremely high levels (~200 in 2022) it has steadily declined and now trades at low multiples, suggesting that valuations have corrected significantly and earnings have caught up with price.

In terms of governance, the firm boasts a sales force of 10,176, divided between tele-sales and feet-on-street. Its board comprises directors with Reliance Retail and Jio Platforms backgrounds, reflecting strategic cohesion with the Reliance ecosystem.

Just Dial plans to achieve mid-teen revenue growth in FY’26 with EBITDA margins over 25% through operating leverage. The key drivers are opening an online shopping portal, enhancing B2B realisations, dynamic pricing with a 7-8% blended hike, and increased ad spends (2.5-3% of revenue) to enhance traffic and leads. The firm has turned away from cold calling and towards qualified lead sales for 2.5-3x productivity and is incorporating AI for reviews, content generation, lead scoring, and auto-created videos. A formal dividend policy, likely distributing 100% of PAT, is pending soon, while integration with MyJio has been deprioritised.

Good to know what fellow members think about Just Dial’s growth strategy and valuation. Your insights on mobile focus, AI adoption, and transaction facilitation would be valuable.

-

Do you think Just Dial’s shift to transaction facilitation gives it a sustainable edge?

-

With mobile contributing 87% of traffic, how crucial is it for long-term growth?

-

Is the recent PE derating making Just Dial undervalued now?

-

Will AI in reviews and lead scoring significantly boost monetisation?

1 Like

They have also irregular in conducting conference call (since last few Qtr) as they don’t have any update on how to utilize cash. It is safe bet but market rewards future growth so one make more judicious call on valuation or business once they take call on cash.

Thanks!

1 Like

Hi All,

i have been following JD for a year. Below are a few notes of my thesis. It broadly matches what most forum members have been stating here.

Please feel free to share your feedback or pick holes on the thesis. Looking to learn. That is the primary reason for sharing it.

Overview:

- Core business is doing decently well & generating INR ~350 Cr of annual cashflow.

- Requires little to no re-investment. Negative working capital. There is no debt on books

- Management wants to grow the core business topline by 15% annually. I think it may be in 5% range

- The company has INR 5,569 Cr of cash on book. This cash on book generates around INR 380+ Cr of other income

Deep Discount:

- Market is giving a huge discount to the business due to the cash on book

- Current market Cap: INR 6,974

- Cash: INR 5,569 Cr

- Core business is being valued at ~1450 Cr

- Implied valuation of EV/EBITDA of 4x

- Competitor Indiamart is valued at 18x EV/EBITDA.

- At this 15x valuation, the core business of JD would be INR 5,250 Cr (implying an 75% discount)

Trigger for exit:

- This would be when the management decides how to utilize this cash

- They have indicated a dividend policy for the profit generated. At current profitability, it would imply a ~8.3% dividend yield.

- Should the dividend yield fall to 2.5% that would mean a capital appreciation of 3.3x

- Note: I have not considered tax implication of dividend in this calculation

Risks:

- The company delays it capital allocation/return policy. Cash will keep accruing till then

- Reliance decides to merge the company with Reliance Retail (no return of capital)

- Reliance acquired the business at INR 1022. Since the core business has improved from then, this could be a floor price to the merger. Will depend on the valuators report & merger ratio.

- The other source of comfort is that VSS Mani continues to have 10% stake. Unlikely that he may exit at poor valuation. The risk here could be a side deal.

- Reliance has historically known to be a shareholder friendly company. But one can never know.

- Company decides to reinvest the cash in other/adjacent businesses that do not perform well.

- Core business performs poorly

- Spike in bond yields (as we saw in recent quarter) or poor treasury management of the huge cash balance

Optionality:

- Justdial’s core business picks up & grows faster

- Their newer initiatives work well

For now it feels like a long waiting game. In 3 years, this stock will either give 3x (should dividend happen) or almost no return / bank FD like return (if no capital is returned).

I am okay with this risk/reward ratio.(Heads I win tails a lot but i do not lose much)

Now we wait.

Disclosure: Invested & biased

4 Likes

I think IndiaMART has significant cash and investment in its book. So you will need to adjust for that in the calculations above but broadly agree with most of the other points highlighted by you.

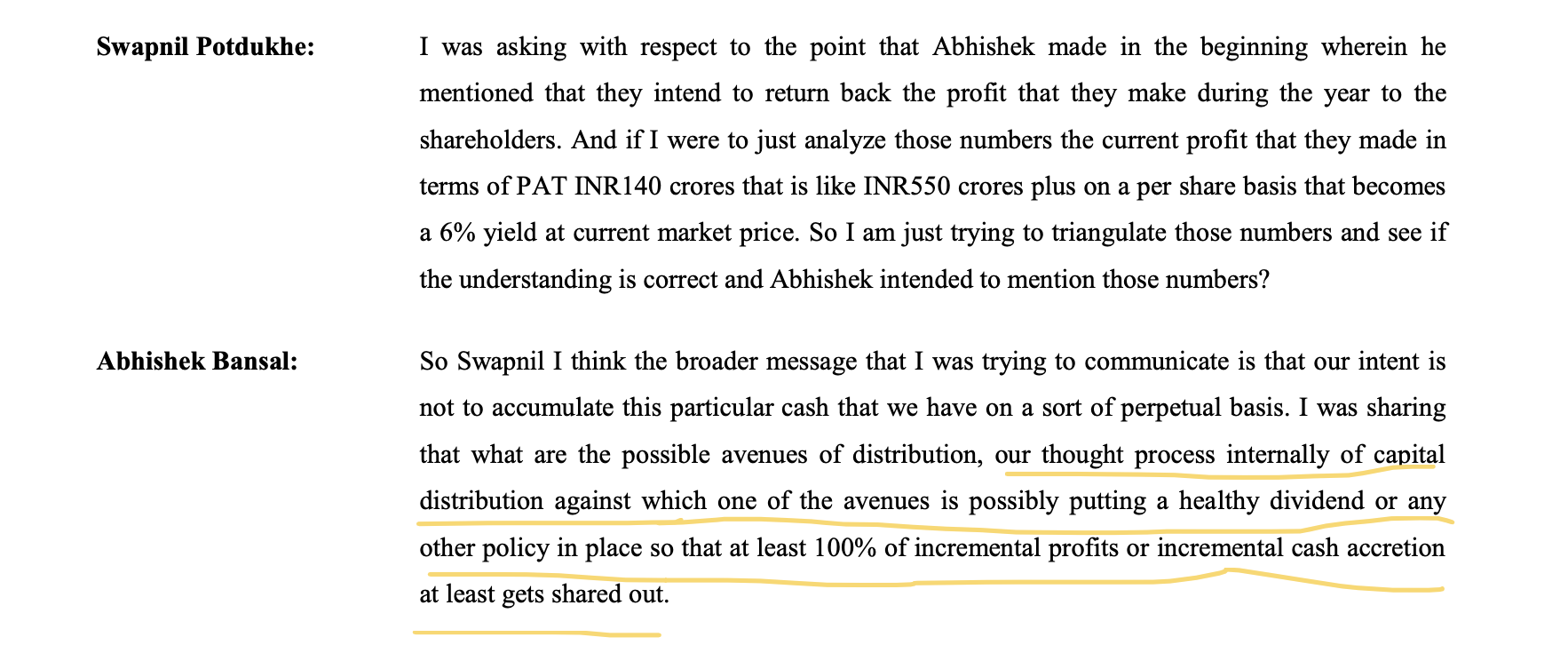

Could you kindly point me to the source of the dividend policy announcement? Any links would be greatly helpful. Thanks

Disclosure: No holding

On IndiaMart, i agree. The cash adjustment needs to be done for apple to apple comparison. My gut feel is that removing income from treasury/investments from EBITDA will increase the EV/EBITDA multiple for IndiaMart. This is because cash is generally already removed from EV.

Regarding the dividend policy, there is no formal announcement by the company. In the past the management has indicated that they will return atleast the full year profit (currently translates to ~8+% yield). Below is the screenshot of the transcript in July 2024.

source: page 10

It has been quite sometime this was indicated. The management has continuously said this will happen soon (including in the april 2025 concall). But it has not happened. This uncertainty is the reason for the underperformance of the stock.

On the other hand, this corporate action of dividend is completely under the control of the company/board and not affected by market/competition/tariffs etc. That what makes this situation interesting to me.

Thank you for sharing the source of the information. Considering this was from July last year there has been no action on the same until now.

Personally, I’m not very hopeful that the dividend policy will change. If you see how Reliance has been treating the minority share holders in other media/entertainment companies(Den networks, Hathway, etc) they have not been investor friendly. 0 dividend payout despite companies sitting on cash and having consistent yearly cash flows.

Also as you said, the decision is controlled by the board and not the management of these companies so the above shows the mindset of the promoters.

They can easily also delist the companies considering most of them are trading at big discounts to fair value but haven’t moved on that either, so I’m a little iffy that anything will change soon going by past history and looks like this is what market is pricing in currently across all these companies.

7 Likes