I agree.

In my opinion, there are still levers for decent growth given the much lower blended ARPU (relative to India Mart) along with rising growth of B2B share (which has better retention and pricing power).

And offcourse, in case the management announces any capital allocation policy, it generally will be too late to enter at that time.

4 Likes

you are right ,in many terms its a fantastic stock.

but we small investors missing something,

zomato ,swiggy values 2.5 and 1 trn respectively. they can easily build 3rd company with same business model, by using its own cash. they can also think of like Blinkit or zepto. but what Mr.ambani is thinking we all dont know.

but “Bhav bhagvan che…” so withing 1 or2 yr it will reflect in the price. Till then i dont find any reason to worry for small stake holders.

Disc. Holding large portion of my PF.

3 Likes

1 Like

Just Dial’s current market cap is 8000cr and ex Cash / Investments is currently valued at just 3000cr.

Now, comparing this with IndiaMart which is in a very adjacent business similar to JD is valued at 13000cr and exc. cash has a valuation of 10K crore.

Last TTM op profit of JD is 320cr vs Indiamart at 390cr.

Could anyone throw light on why Indiamart is valued more than 3x of JD for just 20-25% higher op profits.

My understanding of both businesses is limited and maybe I’m missing something basic that explains such a wide valuation gap for both. Or market fears capital misallocation risk much more strongly for JD than for Indiamart.

2 Likes

In any business we should not simply net off investments from market cap, that can be deceptive. In this, company holds 5000 crores and say you are a investor who are looking to earn 15% return. Now if you value their investments as 5000 crores, then expectation should be company is ready to payout 5000 crores right away, but as you see there is no clear indication of what they gonna do. Say hypothetically, they give away this 5000 crores after a year, in that one year, this 5000 crores yields 6%, but for you this does not make sense. So you have to value this book by lower value like 4700 crores. if company plans to payout this after 2 years, then you have to think like this book is 4300 crores.

Right now we have zero clarity on what will they do with 5000 crores, so they may do a lousy deal to acquire a company or keep this cash forever without any proper plan. So apply some discount, say 25%. Now this cash is valued at 3750 crores and their operating business with yearly PAT of 200 crores valued at 3250 crores. With slow growth that JD is showing when compared to IndiaMart, this seems a fair valuation. Market is simply waiting for management’s action on paying dividend from free cash flow that it generates from operating business and that 5000 crores. When these two event occurs, market will rerate. But definitely JD should trade cheaper than IndiaMart because of the fundamentals

6 Likes

There are two ways to do it. One is to do it as a sum of parts.

- Core business giving cash flow discounted at hurdle rate.

- Investments giving cash flow discounted at hurdle rate (this will become smaller every year like you said). If one knows when it would be given back then one can account for it similar to dividend or not.

The other way I understand is the Enterprise Value method, where the impact of investments is point in time.

If I am buying this company then I am not really paying the stock price but a smaller amount, as I assume that I have the cash belonging to me.

I am guessing that, given their track record, of being non-commital of sharing cash with shareholders - using the first method may be more appropriate.

3 Likes

According to me Biggest issue currently with justdial is they stopped doing concalls this is 2nd qtr in a row when they have stopped speaking with investors…many questions which were asked in calls are being avoided

What about myjio integration, dividend distribution policy, any new initiatives on monetisation of cash?

What percentage of revenues coming from b2b side? Any possibility of cross selling initiatives with jio?

Current market cap is about 7600 cr less 5050 cr of cash so we are getting whole company at 2550 cr against an fy25 ebitda of about 330 cr…

dirt cheap none of the listed peers in online space available at such a throwaway price…its high time management should do something about this

Disc

Invested and planning to add more on dips

5 Likes

i found JD to be the most atractive value propotion in entire market … … due to presence of huge cash pile, existing business and presense of reliance group.

Reliance is known for larger than life future trend prediction,then planing ,and execution . so i am waiting for the picture to be clear.

But at the same time the dark part is "Its not so investor friendly , they do all Tac-tics and then give reasonable pile to the small stake holders:-) …

i want to understand is there any chances of getting sold to the Google or they became partner in any vertical, because RIL have tendency to partner with such huge players like they have done with Blackstone in Jio fin.

Disc. invested large portion of my PF.

4 Likes

I appreciate your conviction in investing large amount of your PF but please do some work in understanding the performance of companies acquired by Reliance.Dunzo after being acquired by Reliance did terribly and even despite reliance’s huge pockets,they were not able to steer them properly while others like Bigbasket acquired by Tata and Blinkit by Zomato has done well

4 Likes

My Personal Opinion - Don’t invest in JustDial thinking that the promoter is Reliance. Reliance is a kind of international behemoth whose main focus areas are Renewable energy, Green Hydrogen and many more mega projects. So it will be least bothered about a sub 10k mcap company - Just Dial.

My point is don’t get anchored to Reliance while looking at Just Dial. Study JD as a separate entity.

Not invested. Just tracking.

dr.vikas

6 Likes

Okay let me try to elaborate what attract me…in JD

- it’s profitable since it’s inception. Maybe only for a year it’s in loss…

- there stability to stay on cash while most of burning cash…

- and the most important one - last 8 quarter of continuous margin improvement. Very good prfit growth and a reasonable sales growth…

Look at the free cash flow generation… - what I am expecting is a completely new revenue streams will open in near future.

- while the cash pile and presence of Reliance will limit the backside…

So reasonable downside and unpredictable upside attracting me…

Disc . Invested

6 Likes

- Cashflow doesn’t really matter until there is any deployment of it either in business or to shareholders.

- Just Dial haven’t been able to increase their realizations (their B2B avg. realisations are at 20K) whilst Indiamart literally has packages ranging from low thousands to 8-10Lakh per annum

- I really don’t think they would be building any new revenue stream as they claim they are already working on JD Xperts and other platforms but there is no result (no contribution) from these platforms as they are just too late with their execution.

— Why JD Xperts did not work: Lets consider pest control as an example, they already have Pest Control ppl listed on their platform who are paying JDL for advertising/visibility and now if JDL starts JD Xperts it will cannibalize their sales. Which they are not ready to do so.

4 Likes

I don’t think JD experts failed…

What will be the way of contacting services like plumber electrician carpenter garage mechanic and many more…??

Definitely if not today then tomorrow you will have to use services like what JD is offering…

There is a huge entry barrier look at the pool they have created in last 20 years of their existence.

It’s much more than there 5500 crore cash…

2 Likes

I think you’re not getting the point. I never said there is no demand for JD Xperts. But it wont be pushed from company’s side as mgmt has conveyed that they don’t want to risk losing the revenue they are getting from advertising. It is very simple consider it as white labelling. For ex: they are already advertising pest control providers on JD platform and if they push JD Xperts (which basically puts their name on front) they are essentially white labeling (even though it’ll be outsourced from their bunch of pest control providers) but why would the people who are paying for advertising continue paying if they can get into JD xperts. And company doesn’t want to do this as sales cannibalization.

3 Likes

very nice and clear thoughts …

It will be very fruitful if you can share ur curent views/analysis on JD…like what u have think it would be, and what it exaclty become today… and at the same time why Mr.Ambani has jumped on it with another 2kcr infusion ,

Thanks

1 Like

The simple fact is that - Till the time management comes up with some concrete plan for use / distribution of the free cash flow it generates, this stock will languish around these levels.

dr.vikas

1 Like

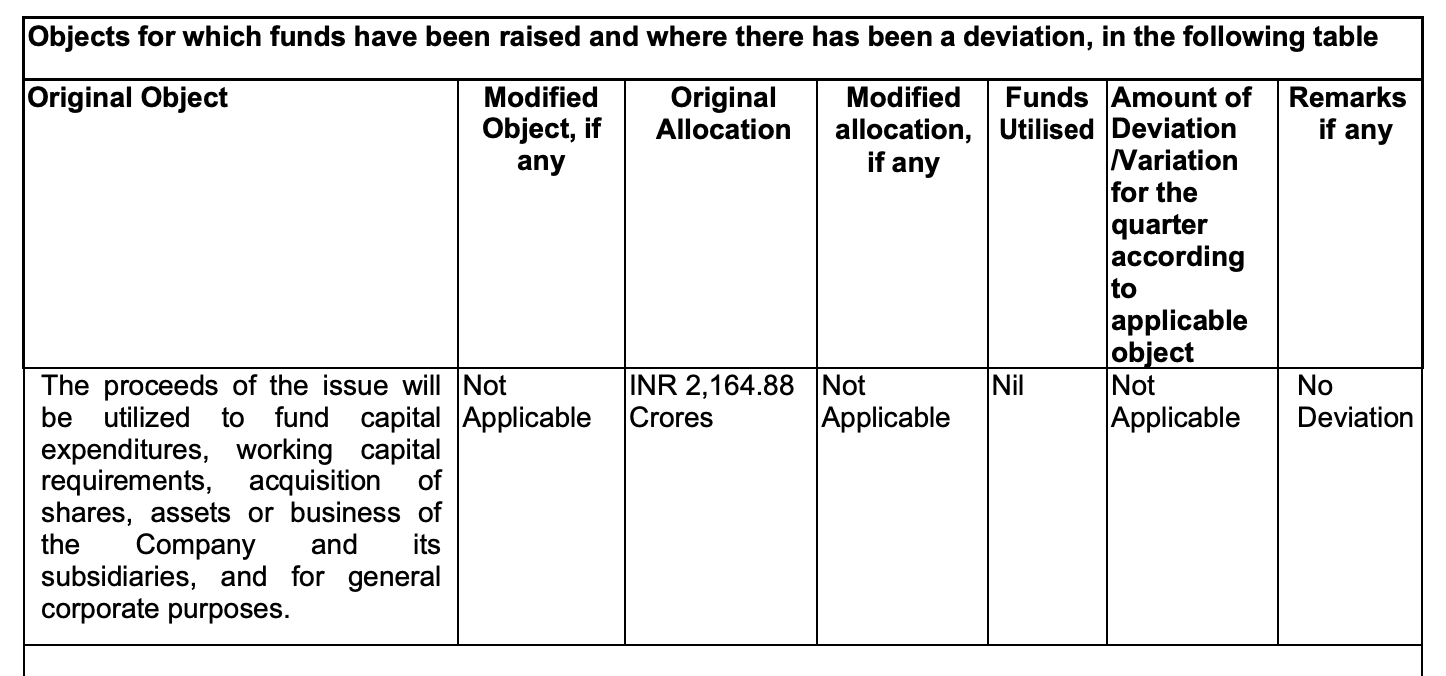

Hi All, I just had a cursory look at JD & the situation looked interesting.

There is a core business that is doing decently well & generating INR 250 Cr of cashflow. Added to this there is another INR 5000 Cr of cash on the BS.

The market looks to be discounting the company because of the high cash & there is little guidance on how it will deploy the cash.

My first assumption that a significant portion of this cash could be returned in the form of Special Dividend or buyback. But then I realised that INR ~2156 Cr is from the preferrential issue. As per the below filing of the company, this money can only be used for the following purposes

- Capex

- Working capital

- Acquisition of shares, assets or business of the company

- General Corporate Purpose

1, 2 & 4 dont make much sense since it is an asset light business (no capex) and has negative net-working capital.

The above rules out Dividend for this portion of the money. That only leaves acquisition of company shares, i.e, buyback (which has its own restrictions)? Again why pump in money into a company just to undertake a buyback? It does not make sense to me.

The alternatives i can think of is to use the money in the business or invest in other business lines? Or merge JD with another company (say Jio platforms)? I could be horribly wrong.

Also, does regulations allow them change the end-use of the cash?

My hunch is that the management’s hands are slightly tied on this portion of cash.

Is my understanding right?

Screenshot -

6 Likes

Could anyone throw light on why Indiamart is valued more than 3x of JD for just 20-25% higher op profits.

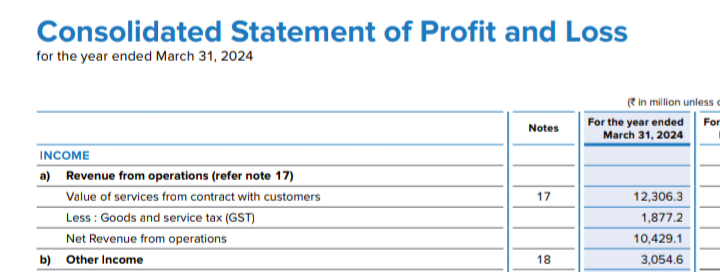

I guess JD only appears to be undervalued due to the bloated numbers in their financial reports.

For example, screener.in website shows that the company earned Other Income of 305 cr. in FY 2024 but I could not find clear details about this income in the published financial report.

Also I could not find details about Other liability items of INR 739 cr. in the same period.

Please share, if you know any details about these two numbers.

1 Like

Other income of 305 cr is right there in both quarterly statement and annual report. Screener combine lot of liabilities and show it as one other liabilities in their website. It is also matching if you combine all liabilities except lease liabilities

3 Likes

Hi @Admantium

There is a provision in the companies act using which you can change the end use of the cash raised via a preferential issue. Read Section 27(1) below

Section 27(1) states: "A company shall not, at any time, vary the terms of a contract referred to in the prospectus or objects for which the prospectus was issued, except subject to the approval of, or authority given by the company in general meeting by way of special resolution "

So basically you need to get a special resolution passed for this. And the below rule Section 114(2) says that 75% of the shareholders should approve it.

Section 114(2): Ordinary and Special Resolutions. This section defines a Special Resolution. It requires that the votes cast in favour of the resolution (whether by show of hands, electronically, or poll) by members are not less than three times the number of votes cast against the resolution. This translates to the 75% majority.

So if both Reliance and VSS Mani agree on something they can change the end use of the cash. Hope this helps.

3 Likes