Generally companies acquired by RIL have NOT done any wonders from return perspective. It has more to do with size of these is so insignificant wrt to RIL that they must be run like some tiny unit of RIL with lack of focus.

1 Like

Immediately after the takeover, covid happened. They have been working on new initiatives like mentioned above. They are aware that, the sector is very disruptive. So the cash is there for promotion of new initiatives or if any new inorganic opportunity comes up. Mgmt. is very conservative about how they use the cash. For now cash earns 7-7.5% kind of yield. They have been focused on bringing the core business back to pre-covid levels, that is showing results over last few qtrs.

VSS Mani, who comes from very humble background is still at the helm.

This old article, gives good account of the man.

As investors we need to keep an eye on how the puck is moving. For now, mkt has ignored the improving dynamics of last 5 qtrs.

Their qtrly revenue run rate inching closer to indiamart’s levels, but margins are nearly half and improving. But the valuation gap is too wide.

4 Likes

Mgmt interviews after the results.

Few Learnings regarding the revenue recognition and terms used by the company

- Realizable value : is a current estimation of the amount of the money the company should ideally be receiving from the existing customer (already made signups) in next one qtr/year. This value, they keep back testing with their historical data. So basically it’s an estimate and mostly given in a range than absolute value.

- Deferred revenue : Whatever money that comes in from customer is deferred revenue. A part of that gets recognized as actual revenue in coming quarters. So, if a customer paid, say 24,000/- for annual subscription, then the whole 24,000/- becomes part of deferred revenue. Each passing day, as the service is rendered the 24,000/365 becomes part of the operating revenue reported for the quarter numbers.

2 Likes

What are the strategies of management to ensure they stand out v/s other players? also strategy road map with reliance coming in is not very clear.

Q4 and FY23 Earning Summary

-

Operating revenue for qtr: 232.5 cr. up 5% QoQ and 39.5% YoY

-

Operating revenue for Year : 845 cr. up 30.6% YoY

-

Adjusted EBITDA for qtr: (excluding non cash ESOP expenses), 35.6 cr. (EBITDA margin 15.3%)

-

Adjusted EBITDA for Year: (excluding non cash ESOP expenses), 95.5 cr. (EBITDA margin 11.3%)

-

Employee expense increased 29.2% YoY led by 37% increase in headcount. rise of 3% only on Sequential basis.

-

Other income for qtr: stood at normalized 74.2 cr. (mainly from 4000 odd cr. cash in BS).

-

Other income for year: 141.9 cr. (there was MTM loss in Q2 due to rise in interest rate)

-

PAT for qtr. : 83.8 up 278% YoY and 11.3% QoQ

-

PAT for year: 162.9 cr.

-

Collection at 945 cr. vs revenue of 845 cr. the difference of 100 cr. seats current liability/deferred revenue in BS.

-

Deferred revenue : 438 cr.

Q4’Call Summary

-

Deferred revenue stood at 438.2 cr. growing 29.6% YoY and 8.9% QoQ

-

Tier 1 cities contribute about 61% to revenues and 41% to paid campaigns.

-

B2B side of the business (JDMart competing with indiamart) contributes 26% of the revenue. vs 20% 3 years back. In order to monetize this segment better , there is a dedicated 700-750 member team working on it. Mgm expects this to be the key growth driver from next 2-3 yrs perspective. Target customer is SME segment. Realization in this segment is 10-15% higher than normal Just Dial customer. Assessment is to take this 26% to 33-35% over next 2-3 years.

-

Margins : pre-Covid they were at 25% plus sustainable margins. exited FY23 at 15% margins (full year was 11.3%), Next year same time (Q4) mgmt expects to be at pre-Covid margin levels.

-

Tax rate: operating income attracts 25.2% tax rate. other income so far used to attract 12% to 13% tax rate, with the change in taxation norms, assuming they hold them for 3 years, they will be taxed at 20% with indexation, so effectively 12-13%

-

Next Year major expense heads estimates: Employee expenses could be 10-12% higher than current year. Ad expenses could be 35-40 cr. ( new initiatives may need more cash, will decide when time comes).

-

Landscape of target market : 65 million S&M businesses, and 10-15 million freelancers. so a total universe of 75-80 million. so even 1% of that population spends on digital advertising it comes to 8,00,000. The number we have as active campaigns at 5,38,000 is still miniscule and lot of headroom.

-

Growth : Realizable value for next year is 1000 cr. (20% revenue growth from current year based on current signups.). Plus the new recruitment which has happened over last few qtrs is expected to deliver better sales growth. Half the growth should materialize from addition of paid campaigns and half by realization.

-

Use of Cash: Mgmt is very evasive and non-committal on this. Might use for inorganic opportunity, might use for promotion of new initiative (but again rebuts this, saying we are not into mindless spending etc etc…). Says the sector is disruptive, we need to conserve resources for any eventualities.

My take: Post Reliance take over and covid, this has been first year of company doing well operationally. It seems, for FY24, we can bake in a 1000-1100 cr. revenue at 20% EBITDA margins kind of scenario. So 200-220 cr. of EBITDA, ~30 cr. of Depreciation, 25% tax and 120-140 cr. kind of PAT figures from operation.

4000 cr. cash yields at 7.2% and 12% tax gives. 250 cr. of bump to PAT. No idea on how to value this. Best IMHO, is value it as cash, simple.

Mcap : 5681 cr.

Mcap ex of cash : 5681 cr. - Cash 4066 = 1615 cr.

company capable of earning 120-140 cr. PAT with solid BS, decent growth rate of 20+%, EBITDA margins of 25% and hardly any requirement for capex should trade at 30-40x trailing (??) i.e, 3600 to 5600 cr mcap ? Plus the 250 odd cr. added to PAT from cash. I hope so!!

Disc: invested after results.

8 Likes

With a growing share of revenue coming from JD Mart, does it make sense to see it as a growing competitor to IndiaMart? Which is trading at a much higher PE and market valuation?

The Q1 result looks like company is on the right track in its growth story, valuation seems fair as well.

However, from a look from its website UI it seems too diversified, trying to get a bite of everything from restaurants to travel bookings, where one would think of more specialised vendors first, like a Zomato or MMT. Seems like theyre throwing darts in the dark and trying to see what hits and what misses.

I feel this stock can have give great returns when you compare it to other internet companies which trade at much higher valuations than Justdial while not even necessarily being profitable.

Would appreciate any thoughts on this from more experienced investors.

Disc: invested in a tracking amount and increasing holding bit by bit

1 Like

Is anyone tracking this story?

1 Like

I guess only a few people have done their home work in this story including - @rajpanda

This is getting extremely interesting since April, 2023. Both the quarters of Fy24 so far have produced results in line with management guidance and expectation. Look at their PPT.

- Active Paid Campaigns

- Total Active Business listings

- Quarterly unique visitors (users)

- Penetration in tier 2+ cities

- Realizations per customer

All the above metrics have been consistently increasing in last 6-7 quarters after hitting the rock bottom in 2021. In fact in the latest quarter, all are above pre-covid levels.

On top of that the employee count is going to remain steady as per mgmt. going forward which will contribute to better margins and profitability. This is a very prudent approach taken by the mgmt to maximise profitability - just read their concall to understand their reasoning. Their advertising has become more efficient, prod. development expenses aren’t going increase further as they have already invested in development of JD Experts, Omni and Mart.

I see only 2 big threats in this story:

- Capital allocation: CFO himself is not clear what would be done with 4200cr of cash which is currently giving 7.2% yield. He is deferring those decisions to the board which consists mainly of Reliance folks. My guess is that the market is also quite suspicious of this and hence such valuations.

- Doubling down of investments from Google in this space. I can see Google is getting more aggressive in Indian markets in last few years - loans via Gpay, listings on Maps, partnerships with banks and credit cards companies, etc. As of now I don’t think they have a dedicated focus in this SME space, but could happen in future…

Other than these two, there is a little bit of concern from the promoter as someone already mentioned earlier in this thread that they would try to maximise their overall value instead of this subsidaries value - conflict of interest with Jio platforms. However, I think this is quite unlikely because otherwise they wouldn’t have infused capital at 1100 share price.

@rajpanda your take?

7 Likes

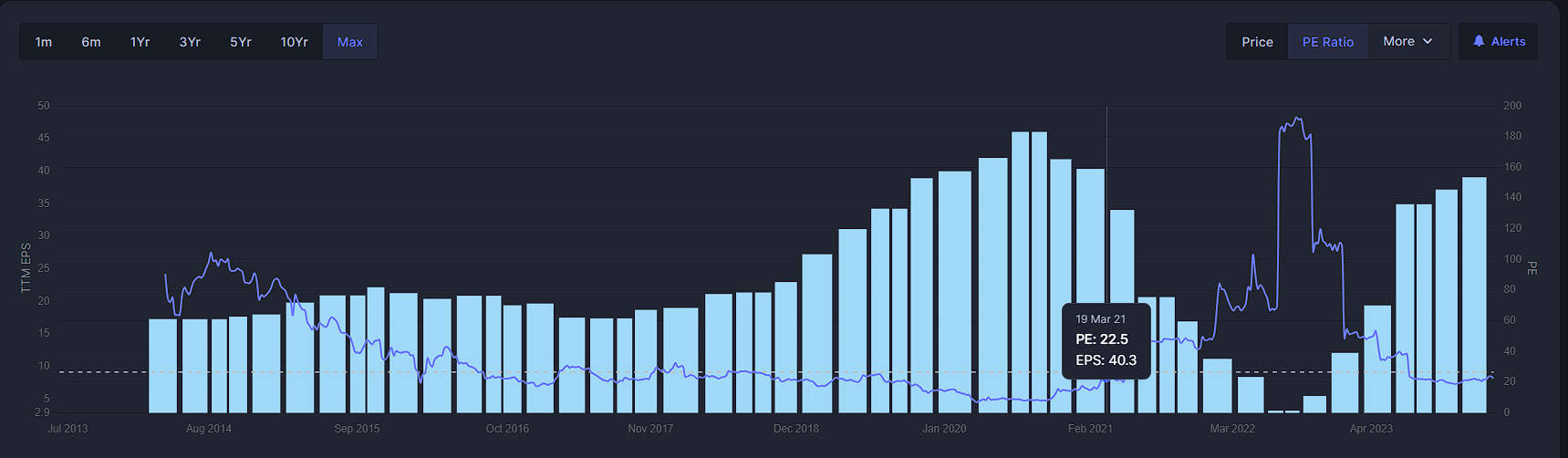

I want to know your views on the valuation of the business, as the historical PE suggest that the prices are favourable

Superb results again

1 Like

Here is the latest investor presentation by JustDial

https://www.bseindia.com/xml-data/corpfiling/AttachLive/aaf155c8-d501-413a-998b-36fbc96f3b1b.pdf

Hope you find it useful

dr.vikas

Isn’t it, sole reason for Profit increase is decrease in employee cost ?

I mean Q-Q & Y-Y they are reducing number of employees. Y-Y almost 10% reduction in staff. Even on previous concall people raise this issue & they answer that they are rationalizing staff. But they can’t reduce staff at same way after certain limit.

1 Like

- Deferred revenue growth of 16% suggest atleast 15% revenue growth in FY25 which implies 1.15 X 1043 crs = Rs1200crs.

- Management has guided for 26-27% margin in FY25 up from 21% in FY24 which implied EBITDA of Rs 318crs EBITDA up 47% YoY.

- Based on above company should do > Rs500crs PAT in FY25. Company is trading at < 18x FY25. Indiamart the closest competitor is trading at 40x

- So Just Dial looks like a great pick

Disclosure: Invested

4 Likes

Please find below the links for the recent con call.

Hope you find them useful

dr.vikas

There are a few positive points from my side.

1 - Management is by Reliance

2 - Huge cash on the books. But management is not in a ‘HURRY to piss it off.’

3 - It’s an Indian company. The Indian government will always give preference to Indian companies over foreign companies. Ex. Mapmyindia is more favoured by GOI over, say, Google Maps. The same thing may play out here. (I am just trying to connect the dots )

Invested and BIASED.

dr.vikas

anything has changed after March24 results?

Disc. Invested

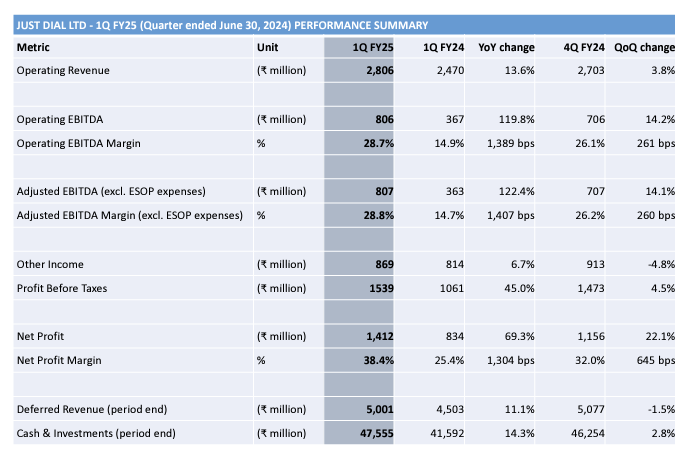

1Q-FY25 Revenue stood at ₹ 280.6 Crores, up 13.6% YoY

EBITDA stood at ₹ 80.6 Crores, up 119.8% YoY; EBITDA Margin at 28.7% (vs. 14.9% in 1Q-FY24)

Net Profit at ₹ 141.2 Crores, up 69.3% YoY

Traffic (Quarterly Unique Visitors) in 1Q-FY25 stood at 181.3 million users

Cash and Investments stood at ₹ 4,755.5 Crores as on June 30, 2024, up 14.3% YoY

Annualizing quarterly of Rs140crs, for the full year the company should do Rs560crs for the full year. AT Rs8803crs market cap the stock is at 15.7x FY25E P/E. Indiamart at > 45x P/E FY25E

Paid campaigns YoY growth 1.4% only, will monitor upcoming quarters…Likely 1200 (+or- 5%) cr revenue from operations and 290 cr (+or- 5%) op profit + 330 cr income from investment. 9-10% tax for fy 25…