Compnay Background:-

Jupiter started its first hospital in Thane in the Mumbai Metropolitan Region that is MMR in 2007, the second one was in Pune in 2017 and the third in Indore in late 2020. This is a 96 plus percent subsidiary. Thane and Pune hospitals are both around 375 beds each and were Greenfield projects, while the Indore Hospital was an acquisition that is planned for about 430 beds, but we are currently operating around 231. All our hospitals are full service independent hub hospitals, where we provide all services from childbirth and newborn care to cancer and organ transplantation services. As we speak, we are constructing a 500 bed hospital in Dombivli, which is also in MMR. The land is purchased, all permissions for construction received, the excavation is now complete and we have begun constructing upwards. The project is likely to be operational anywhere between 2 to 3 years from now. The construction is currently in full swing and working as per our scheduled time.

As the stated objective of the IPO, Company mentioned last time, Company have

repaid all our debt obligations and now got annualized finance savings of over Rs. 40 crores. In the previous quarter, Company also completed empanelment with the insurance companies in Indore, and consequently, Company occupancy has increased from 51.2% in the last quarter to 56.2% in Q3 FY24. The contract renegotiations with insurance companies at the Pune Hospital are also concluded and it has been one of the factors that has helped to increase the ARPOBs from ~49,000 in Q2 24 to 53,400 in Q3 FY24.

Personally I have been to their Thane hospital for my mom cardial test, Although charges were slighlty higher but the experinace I had was worth it. From Reception intraction to test. Mom was very well taken care of and my billing experiance was great.

Hospital was very clean and seems luxuries. Overall it was wow experiance for me. Since then i have been following this stock. I visited in Dec 2023.

Industrly Background:-

Jupiter life line hospital Q3 update:- Company has posted its highest profit this qtr, partly due to its repayment of debt. Company is walking the talk they said IPO funds will be used to repay its debt and they have done this. Company operate independently on

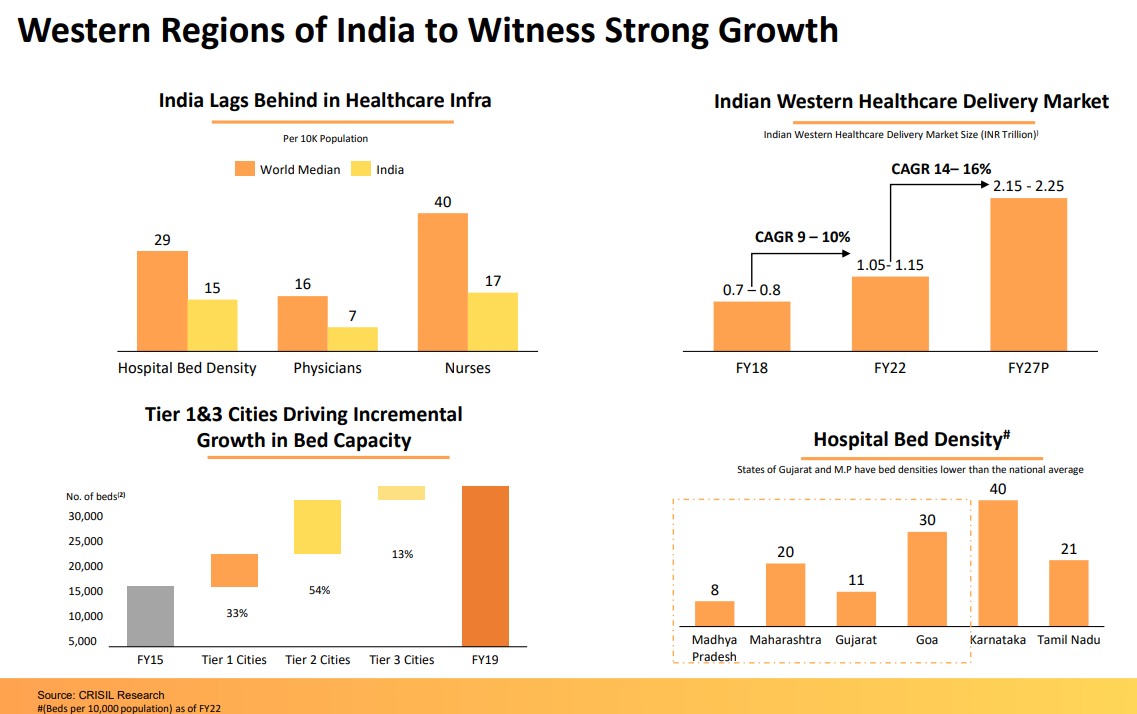

owned land.The proportion of the Indian population of 60 years or more is expected to rise to 12.5% by 2026 from nearly 8% in 2011

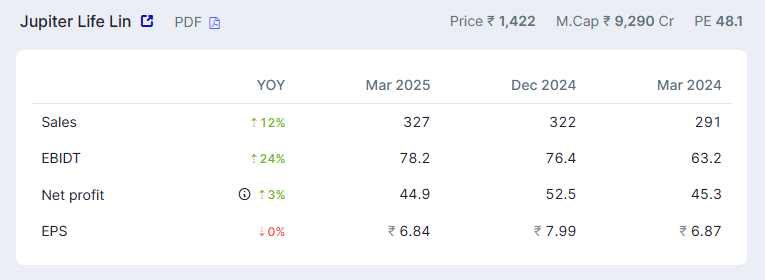

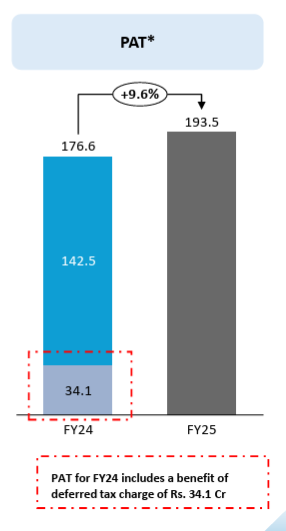

FY24 Nine Months period update : -Fo**r the nine months period, the total income has been Rs. 782.1 crore, 19.8% growth. The EBITDA for nine months is Rs. 178.9 crores, that is a 17.6% increase Y-o-Y. And the EBITDA margin is 22.9%. The PAT for nine months is Rs 131.3 crores. The average occupancy for these 9 months has been 63.2% compared to 60.6% in the previous year same period. ARPOB for 9 months FY24 is Rs 53,585 and the ALOS is 3.92 for these 9 months.

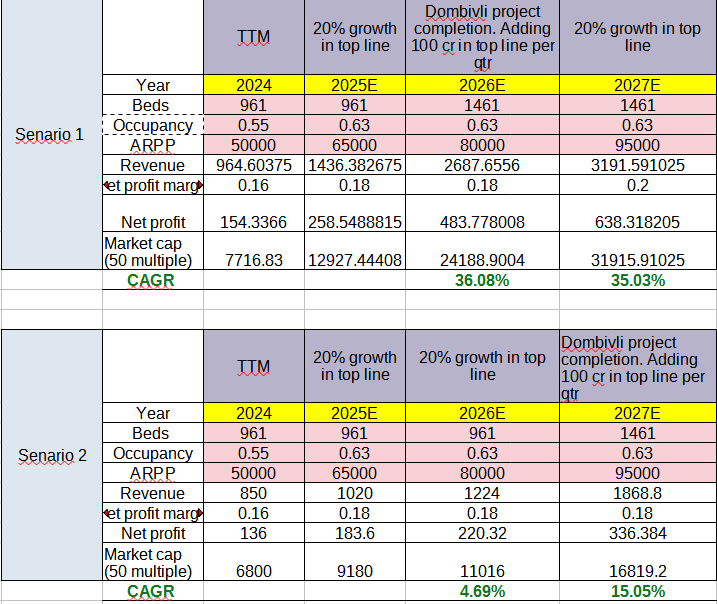

Capex Update:- Company is doing a capex in Dombivali east for 500 beds. Kalyan dombivali region comes under smart city plan of central goverment. Project is very near to Lodha palava city and proposed metro line. Many residensial real estate plans are about to be completed.

Above image shows 2 senarios

Senario 1 - Project completed in FY 2026. Considering 20% growth annualy on existing hospitals and adding 100cr qtrly revenue in top line. (100cr calculation as below 500 beds - 50% occupency - 50000ARR) . With net profit % at 18% 2026 profit would be 483cr and 2027 638cr while taking 50 multiples I have come to a target market cap.

Senario 2 - Project compeltion in FY 2027. Considering 20% growth annualy on existing hospitals and adding 100cr qtrly revenue in top line in FY 2027. with Annual profit of 336cr and multiple of 50 market cap would be 17000cr

Risk and threats

- Delay in dombivali project compelation

- Growth of less than 20% in top line

- Reduction in Net profit %

- Company borrow heavely from External market which reduces its NP

With above very optimist senario and after seeing this above CAGR return compnay seems fairly valued at this price.

Please provide your feedback any feedback will help. Just let me know if you have liked it or dont liked it. where did I went wrong what i have not embeded in this calculation.

Is this right way to analysis company or should I change the way?