Q2 call

What all is wrong- There seems to be all sort of headwinds possible, have happened/ happening for them.

- Pharma Sector is out of favor and have headwinds,

- Perceived RM cost impact from China and margins contraction

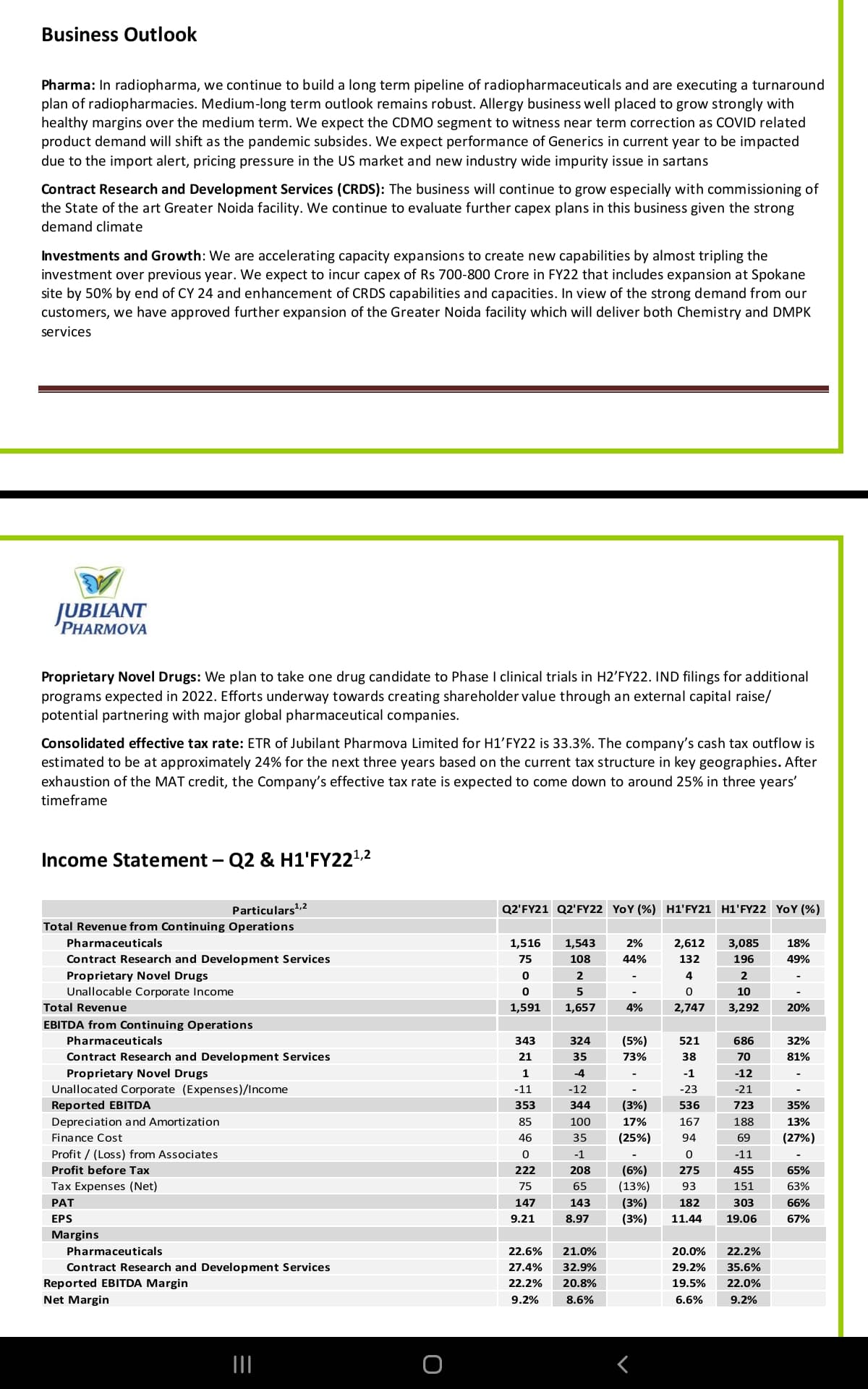

- Import alert on Roorkee plant, full remediation to take few qtrs, exempted products also not being produced yet

- Generics price erosion and some sartan products recall due to impurity

- EBDITA QoQ reduction

- Too complex of business ( too many moving parts or segments)

- Coming out of a demerger ( chemical biz) and headed to some more restructuring ( CDMO unit)

- Covid impacted biz of US( radiopharma) yet to fully recover and continued cases of US covid cases still impacting

- Contarct manufacturing of Covid products reduction ( helped in capacity utilization and margins front in last 2 Q)

- Novel drug considered a drag as long upfront investments and binary outcomes

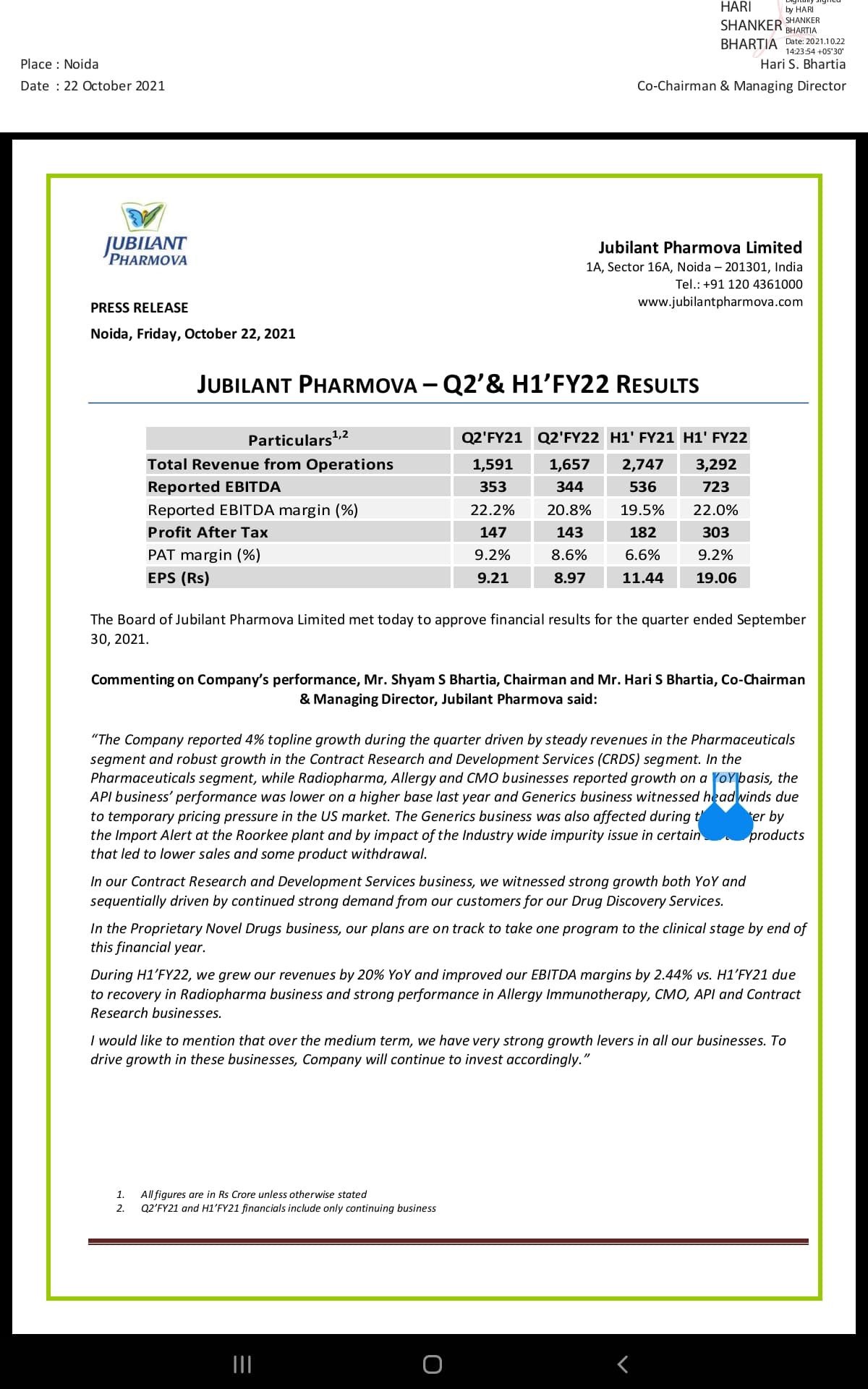

Valuation - less than 1.5X sales, 15 PE and 7X EBDITA on annualized basis, 20%+ EBDITA even at subdued performance.

What is improving and can improve in near term

- Let’s look at consolidated biz view

-

Bigger and mixed bag segment - pharma and subsegments

-

High growth segment- CRDS( or CRAMS in making with in process restructuring)

-

Finally the businesses outlook

Full details here

Some broader pointer, Q2 call inferences and what is changing, what is being ignored by market, future growth triggers etc

-

Good Management pedigree- part of Bhartiya group ( Jubilant ingrevia, Jubilant food works being some of other listed companies - both have created decent wealth for investors)

-

KSM and solvent issue was acknowledged (44:00 in concall) but didn’t seem a structural issue, also relatively manageable one with pass on to customer

-

Import alert - exempted products ramp up started from first week of Oct after recertification completion - net of which it is low single digit impact on that plan revenue ( $35M is gross asset block), they are also working with third party manufacturers to supply banned products, also plant supplies can be used in RoW, on alert resolution plant to submit early CY 22 post which FDA visit to re inspect - net net negligible financial impact

-

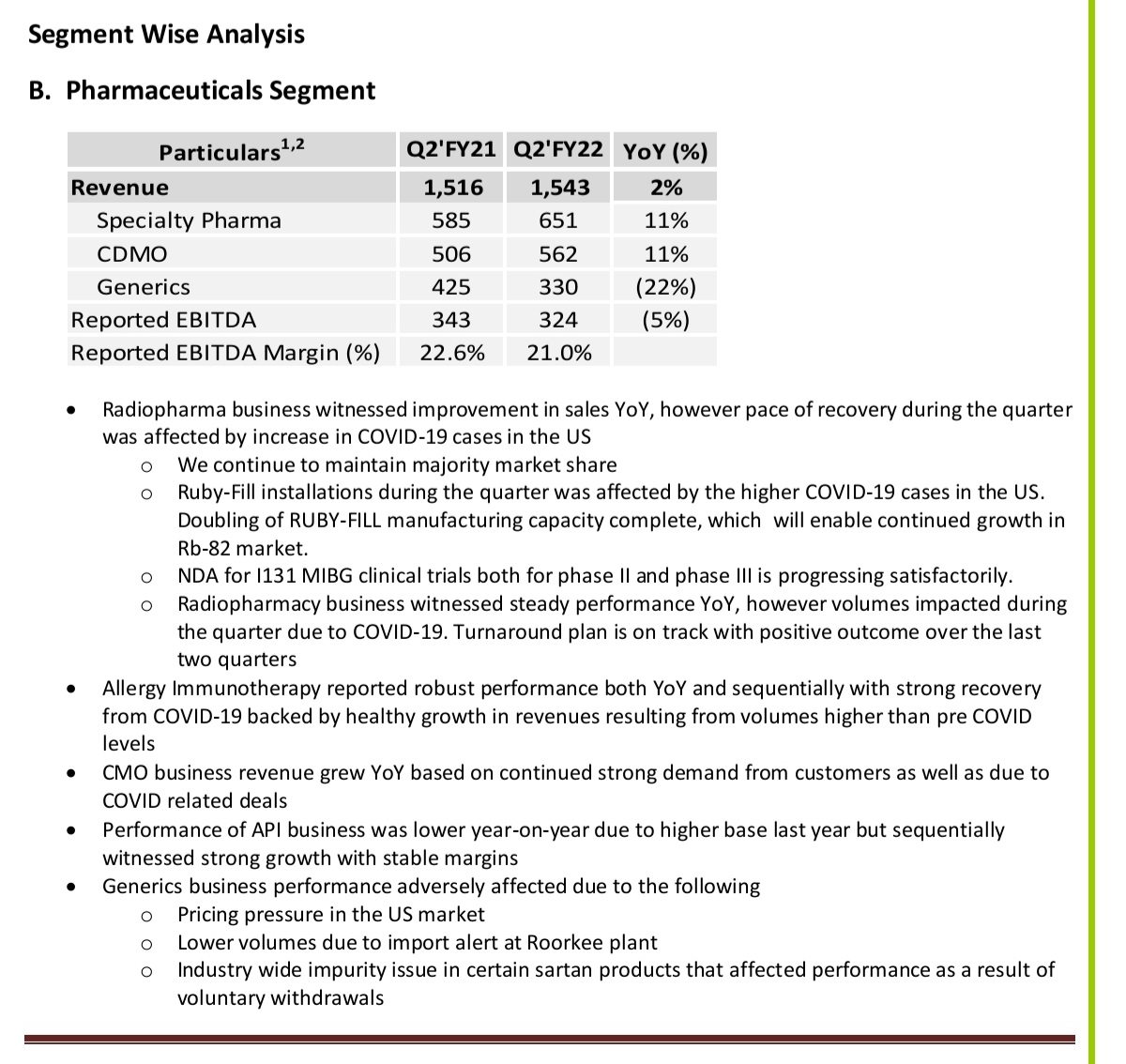

Generics underperformance ( 20% revenue) - per mgmt price pressure in US has cyclical pattern and currently at bottom of cycle, can see 1-2 Qtr subdued performance though API has picked up sequential, Q2 was higher base last year and that will normalize as well going ahead

-

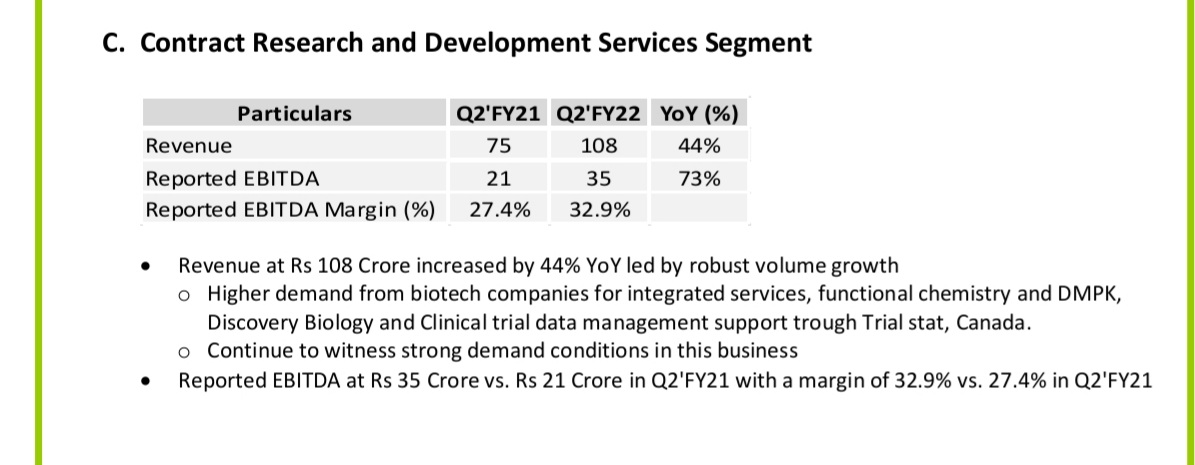

CRDS is dark horse with massive growth YOY of 44% on revenue and 73% EBDITA, high margins of 33% , H1 numbers also impressive , New CEO joined them, Noida expanded capacity came online and further Capex on same announced - as this biz becomes sizable, narrative will evolve

-

Net debt down from 1700 cr+ in Mar 21 to approx 1000 cr in Sept 21(100 odd cr incrementalin working capital but to normalize in next Qtrs), interest cost and rate( below 5%) both down

-

Tax rates were high in H1 at 34% , to come down at 25% over next 3 years - profit figure to look better boosting EPS

-

We have seen value creation out of Jubilant Ingrevia demerger - it’s too early but new CRDS post restructuring will build a high growth and margin asset base.

-

Novel drug can be seen as drag but can also be a high risk high reward optionality- Last concall Mr Bhartiya did indicate ability to monetize if needed, and working on investments to come in for funding ( reminds of Suven life type situation)

-

Specialty pharma will have CDMO carved out thus CRDS and CDMO will start to look good growth and margins biz - together a sizable chunk

-

speciity pharma - Radiopharma and Allegry seem to be on recovery and are based in US geo, multiple Capex coming online here as well in next 2 yrs( radiopharmacy biz breakeven expected by end of this year). This adds to complexity in terms of not being typical India pharma/API game - per numbers does deliver 20%+ margins and double digit growth in mixed bag performance, to improve per mgmt on margins trajectory and Capex already done coming online.

-

700 cr+ Capex in near future Guidance.

Tracking position