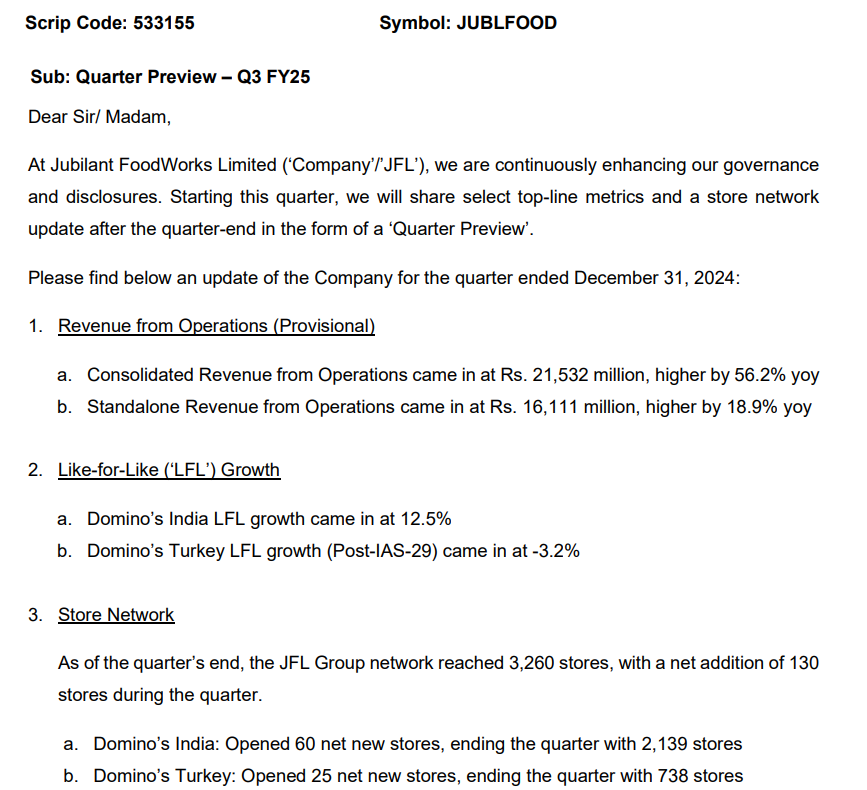

consortium of private-equity firms including Advent and General Atlantic, and Domino’s India Operator Jubilant Foodworks are among the entities in talks to buy Everstone’s entire stake in Restaurant Brands Asia, sources told CNBC-Awaaz.

.

People with knowledge of the matter also revealed that ever since Burger King has not been able to delivered on promised numbers, Everstone has had a hard time trying to turn things around. On the other hand, Jubilant Foodworks has shown significant interest because Restaurant Brands Asia will boost its current portfolio.

This is in light of various news appearing in the media regarding ‘Jubilant FoodWorks Limited (‘Company’) intent to acquire stake in Restaurant Brands Asia Ltd. (formerly Burger King India Ltd.) and consideration of the proposal by the Board of the Company’. In this regard, the Company strongly refutes any information appearing in the news about the Company. These are completely false and baseless and the Company is not involved in any such discussions or negotiations nor considering the aforesaid acquisition.

Sorry for bumping, but the issue that you have raised is a genuine problem for any franchisee investor. I am trying to build a case around different scenarios:

- If they cancel the franchisee, they disrupt their market share as there will be turmoil among suppliers, employees.

- How can they get other stores in same location(largest outside US) even if they do how will they create a delivery network.

- Company like Tata, Adani know that QSR is a low margin business where efficiencies play out over very long term like 10-15 years and it is easier to buy the franchisee player or develop a new category (like Vada Pav), like starbucks.

- All said and above they still have to get the local taste right, then pamper to the local government authorities(food control, trade licence etc.). In addition they take the liability if any untoward things happen(food poisoning etc.), which is a huge risk for an international company.

If I were the CEO then I would rather chase growth through new markets, new categories or new products rather than go through hell and then be accountable if anything in the line goes bad.

Thanks for the question as it made me think.

thanks, Because we have seen a similar problem with Mc Donald’s Franchises as well, also I read dominos international report and the timeline is 10 years on which they need to renew and it is only their prerogative if they want to renew I wanted to understand if this is a genuine concern or not, your answers somewhat helps.

SideNote: If the cancellation of the franchise was not a threat why they would have gone with other franchises[Popeyes, Dunkin] and with their own brands(hong kitchen) I think I have a valid concern.

Hello Sajal,

My reading of things is a little different.

The issue with Mc.D franchisee might not repeat in the case of Domino’s. Firstly they have grown very big. 2nd they are still investing well in the brand. Moreover Mc.D is an example of how messy it is in India to terminate a franchisee(court case, bad press). You might have gone through it but this article details on how difficult it was for Mc.D

All said Domino’s may still consider upsetting the apple cart.

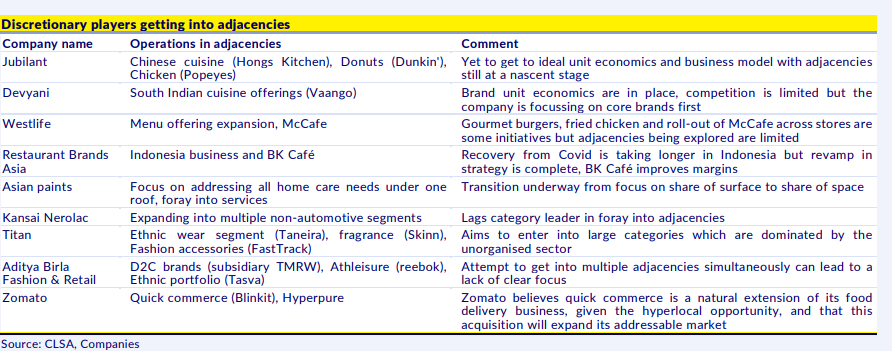

Regarding diversification of brands, from Jubilant’s perspective is to reduce the impact of unexpected rise in raw materials(milk products this year). A diversified set of brands may result in different rates of costs like chicken may not rise at same rate as milk products.

that’s my reading.

Can Anybody help me with the statewide count of dominos pizza stores in India? Thanks

Hey Couldn’t found latest one , but 2 years ago the scenario was this

I was trying to come up with the growth potential for dominos business have taken a lot of assumptions and leverage, please see and comment on what you think about it. and What assumptions I am missing and should be considered. thanks.

Certainly! Let’s break down the calculation based on the provided assumptions:

-

Calculation of Per Order Economics:

- Revenue in 2022: 1217.1 crore

- Total Store Count: 2650 (December 2022)

- Assuming 3 months per quarter and 30 days per month

- Per order cost: 400 (assumed and whatever I could find on net)

- Per day order per store: (((12171000000/2650)/3)/30)/400 = 128 orders per day (approximately)

-

Revenue Projection for 2035 (Best Case):

- Assuming the store count doubles by 2030 (from 2650 to 5300 stores)

- Assuming further increase to 7000 stores by 2035 (conservative figure)

- Assuming per-store sales will stay around today’s level (128 orders per day)

- Revenue per year in 2035: 128 * 800 * 7000 *365 = 26163cr

- This represents a 5x increase from the revenue in 2022.

-

Revenue Projection for 2035 (Worst Case):

- Assuming store count to serve approximately 2 billion people (including India, Bangladesh, Sri Lanka)

- Comparing with the number of stores in the USA (7000 stores)

- Assuming 5600 stores in India (conservative number)

- Assuming per order price stays constant to 550 (conservative)

- Revenue per year in 2035: 128 * 5600 * 400 * 365 = ~11000 cr (approximately 11000 crore)

- This represents a 2.3x increase from the revenue in 2022.

The growth trajectory was quite slow in India vs. China, which can be attributed to the

variance in the economic growth of these two countries. India is still quite an underpenetrated market with ~3 stores per million population vs. China’s 13 stores per

million (six stores in 2013). India can sustain ~10% store growth for global QSR giants

by 2030 (China clocked 10% CAGR in 2013-2022).

Antithesis:

More QSR players with better menus can hamper unit economics, and new stores opened are not able to perform up to today’s level [basically selling lesser than 128 pizzas per day]

The growth potential is not realized, and store expansion slows down. store count does not increases as expected.

Lot of hard work !!. But IMHO equity investment idea which require you to work out projections 12 year far is not the way to go.

This space was good maybe a decade earlier when there were few brands (dominos, Mc D and Pizza Hut mainly) and eating out culture was springing up.

But now the increase in eating outside food (sum of additional purchasing power, change in habit and increasing population) is surpassed by increasing number of options available to consumers… .resulting in mediocre growth.

As the total pie increases, more number of brands will spring and make it difficult to earn alpha returns in this space.

Disc. Invested in RBA and Devyani. Both on sell list.

Westlife guided 100% coverage around EOTF.

Heard the Q1 FY24 concall today, looking at the company after a long time since I exited more than a year ago.

Large part of the discussion in the call was on inflation, muted consumer demand and depressed margins. Popeyes is doing extremely well, says the company but no numbers were given. That is still some time away. Hong’s Kitchen seems to be struggling at the unit economics level, and hence no major expansion. Dunkin was not even mentioned, I think. DP Eurasia acquisition - company has taken a hit on account of the Ukraine War it seems. Though the war was unforeseen, I was never a fan of that investment, countries like Turkey and Russia are politically risky even otherwise.

Overall, no major upside triggers in Jubilant Foodworks right now - company seems to be just waiting for the overall environment to improve. A large Bangalore commissary is slated to open shortly.

My impression is that the company has already become quite large, and growth will only be incremental from here on. LFL / SSSG numbers are always in single digits, and growth due to store expansion will slow down too, since new store openings will add only a small percentage on such a large base (compared to the past). This means valuation has to correct from a growth stock to a stable cash cow stock. Non pizza revenues can be a new metric to track in future, once Popeye and others acquire a decent size. But right now, they seem to be too small to make a difference.

There is 4 quarters of EPS decline, resulting in a P/E of 118 which shows investors have not yet given up hope. The good thing is cash flows are strong, aided by negative working capital. Last three years, capex has been heavy. Capex will come down this year, which means company will accumulate even more cash. But their past capital allocation decisions do not inspire confidence. I have written about it before (click here). That is another problem.

(Disc: No positions)

It’s strange that this thread was inactive from past 4-5 months, don’t know the reason but I am assuming " No earning surprise" in the last 8-10 quarters, was maybe the reason.

Q1FY25 brings some hope in terms of growth, where all other QSR players are facing demand headwinds, the Jubilant Foodworks has shown some sign of growth, in this challenging environment. The 45%YoY and 23% QoQ growth in revenue along with stable 20% margins and LFL growth came of 3.0% driven by Delivery LFL growth of 12.1%, shows some sign of revival in the business operation.

Key Takeaway from the Q1FY25 Concall:

Financial Performance

- Consolidated Revenue came in at INR 1933 Crores, up by 44.8% YoY

- EBITDA margins stood at 19.8%, INR 380 Crores against INR 277 Crores in Q1FY24.

- PAT stood at INR 61 Crores, upward QoQ: +56.9% YoY: +110.3%.

- Gross Margin of 73% at consolidated level.

India Segment

- In India, the revenue at INR 14.4 billion was up by 9.9% YoY. EBITDA margins at 19.3%

- Domino’s growth came in at 8.5% led by record high orders, registering 16% growth YoY.

- Domino’s India LFL growth came in at 3.0% driven by Delivery LFL growth of 12.1%

- Domino’s Mature Store ADS for 1,644 stores at ~INR 80,000 was also the highest in last five quarters.

- Launched ‘best value’ that a QSR chain offers a Lunch Thalia four-course meal at INR 99.

- Launched the globally acclaimed Domino’s Cheese Volcano pizza range meant for cheese lovers.

Turkey Segment

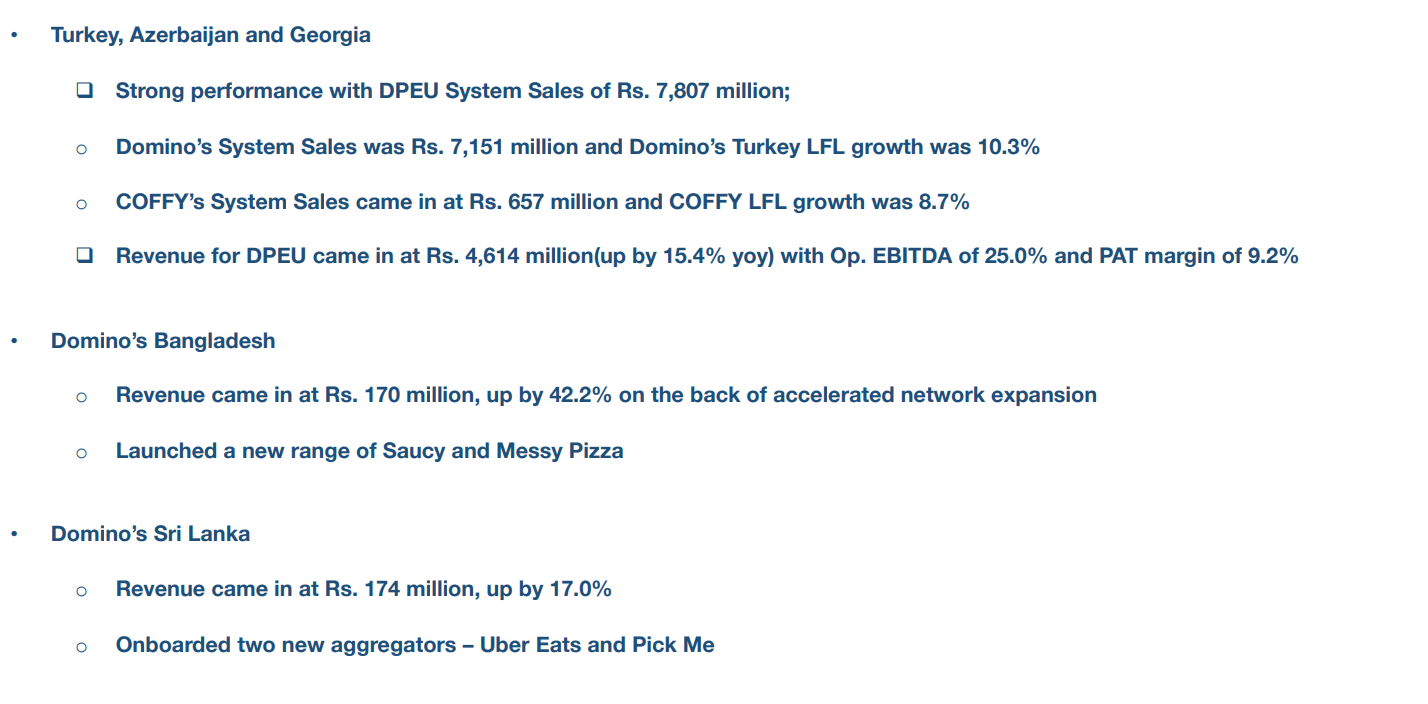

- Domino’s Turkey system sales came in at INR 7 billion and LFL was 10.3%. COFFY system sales came in at INR 656 million and LFL was 8.7%.

DP Eurasia

- The Revenue from DPEU came in at INR 4.6 billion, higher by 15.4% YoY at current currency rate. EBITDA margin came in at 25%

- PAT margin was strong and accretive to Indian business, at 9.2%.

Other Countries

Store Composition

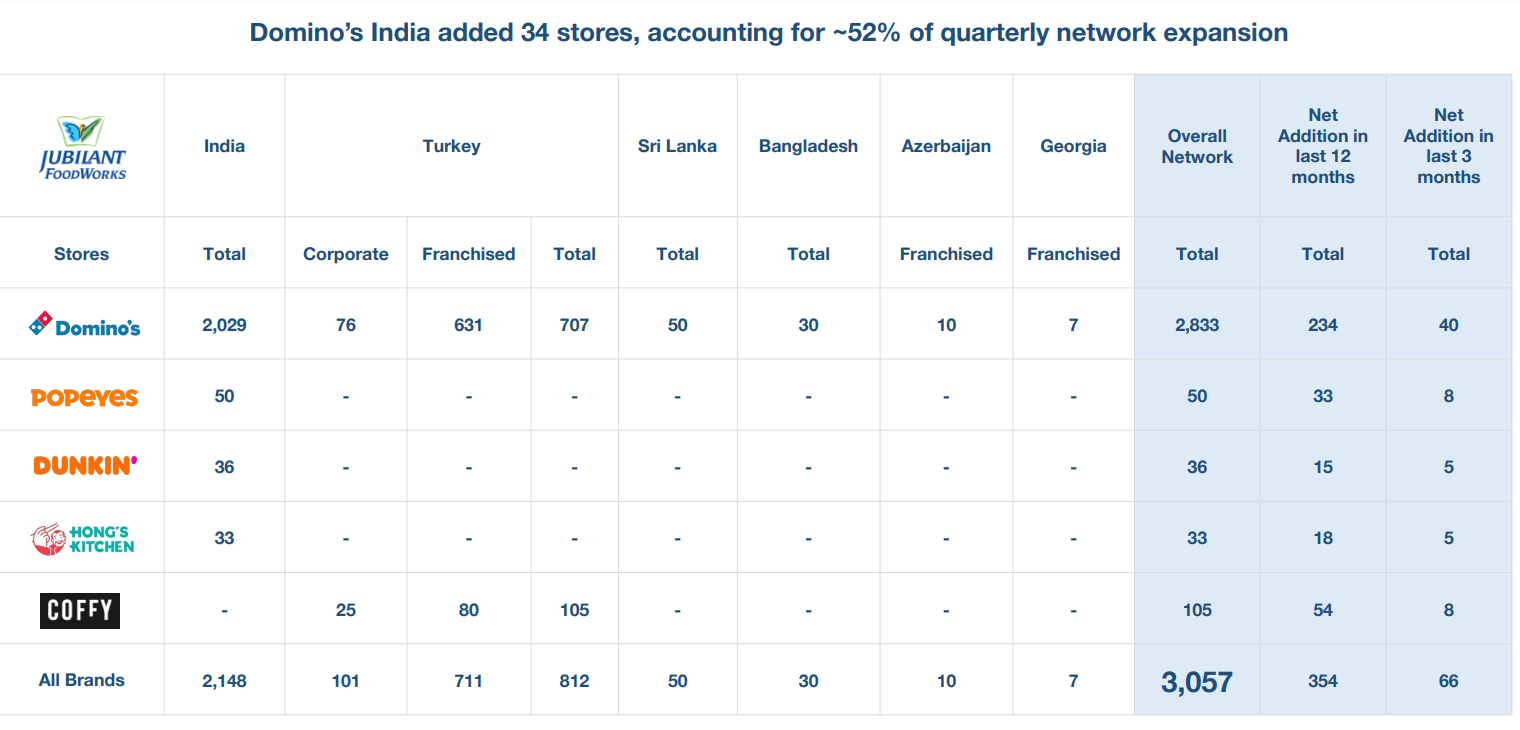

- Reached the milestone of 3000 stores across 5 brands and 6 countries. India’s contribution to Domino’s network at 10%.

- Crossed 100 COFFY stores in Turkey and 50 Popeyes stores in India.

Operational Performance

- The company acquired new customers at highest-ever rate, beating the industry trend.

- No price increase in the straight last 8 quarters also waived off the delivery fees.

- Across the world , delivery as a mix is growing. So there is also a consumer trend that Jubilant is also riding on. Delivery channel now contributes 69% in Q1FY25.

- Delivery channel revenue increased by 15.7% driven by Delivery LFL growth of 12.1% YoY, while Dine-in channel revenue declined by 5.7% YoY.

- Any store refurbish at least would see 10% to 12% growth in dine-in.

- Monthly active users has moved from 10.3 million to 12 million, which is almost 2 million customers we have added.

- Cheesy reward customers are now contributing 50% of business.

- In DP Eurasia (Turkey, Azerbaijan and Georgia), H2 is higher than H1.

- In Popeyes, the management has brought down the store size to fit it into the Indian kitchens.

- Domino’s India volume growth is about 16%, which is mainly on account of reduced threshold fees for delivery which is now only INR 150.

- Majority of the debt in DP Eurasia book is short term in nature.

- Management on any material change in the trend:

“Despite rains, despite heat, whatever the weather conditions we are seeing an uptick in delivery, and that’s what we are banking on.” - Bangladesh business turned profitable at the operating level. On the ongoing political unrest, management assures that staff is safe and company has not incurred any material loss.

- The company is looking to increase the ticket size by offering greater cheese and more indulgence to consumers.

- In Popeyes, the management is focusing on the chicken eating markets, that’s why more stores are in South India.

- In Popeyes, the company has high street locations to do deliveries. delivery share is lower and dine-in is higher at the moment.

- Dunkin is even more on track to kind of achieving high store-level profitability.

Shared my thoughts on recent developments happening in QSR Space

I think POPeyes has huge scope for growth

If they get the coca cola bottling deal, will it impact jubilant food? Bhartias lead race for Coke bottler Hindustan Coca-Cola Beverages, ink exclusivity pact to buy up to 40% stake for $1.4 billion - The Economic Times

what is groups thought on so many local restaurants serving pizza? like crazy cheesy in pune, la pino and many more …how they will impact JFL ?