Analysis by @suru27

Analysis by @suru27

Company’s current effective shareholding in HLPL is 37.68% and it is 35% on a fully diluted basis. The acquisition is finally done as communicated last October.

HLPL describes itself as

“Setup your own online food ordering system in 15 minutes!

Accept orders directly from customers instead of third-party aggregators and save hefty commissions on every order. Take control of your marketing, acquire customers for your brand and own their data!”

Seems like the company is innovating further to reduce dependence on middle aggregators.

Can this be another source of Income in future as they already service Dunzo.

Although I expect low margins here and this may simply be a means of improving service,reach and efficiency.

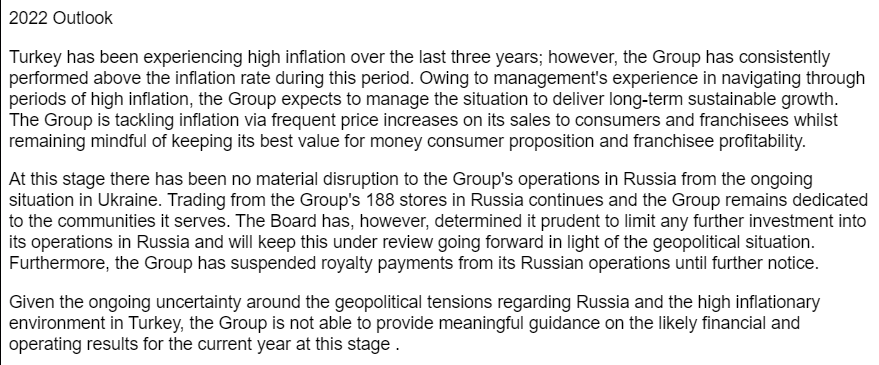

2022 Outlook by DP Eurasia:

Full link:

Recent presentation by ppfas on QSR restaurants

In my opinion next phase of growth will come from popeyes. Currently there are 4 store in banglore. I have never been to any popeyes store but youtube search of popeyes store by many youtubers shows its product is much more superior and delicious in comparison to KFC.Does any one knows what are the future plans for expansion of popeyes store in india by jubilant food work.?

Disclosure: In Wife portfolio at 2556 …views can be biased.

I have tasted in Bangalore Kormanagala. The taste is really very good. Comparing with KFC I find it like comparing coffee day with Star bucks. Popeyes is very rich and has high standards.

Sir what can be the reason for large exodus from fii in jubilant foodwork in your views?Imo recent announcement of departure of Prateek pota is not going to have any meaningful impact in long term growth story of company.

I think Jubilant Foodworks was priced to perfection by the time the management changes started. So, that was anyways ripe for exits from Institutional investors. The recent turbulence and short term hiccups were the trigger.

Jubilant Foodworks, sales and profit are up.

ccc7745b-ee87-4932-9236-3a9361df7f72 (1)-compressed.pdf (5.1 MB)

Disc: Invested so may be biased

Britannia, the country’s largest biscuits maker, is set to get its first standalone chief executive in Rajneet Kohli, who would move from being president and chief business officer at Domino’s Pizza, run by India’s largest food services company Jubilant FoodWorks.

Lately, I have noticed that I am ordering from dominos even though I would have planned to order something else. Their delivery usually happens in <20 mins in my area (Bangalore) and normal zomato/swiggy experience of other restaurants takes >40 mins.

Another thing is that I am willing to pay 10-15 rupees extra on dominos app after discounting normal delivery charges with my app pizza points for faster delivery than order from zomato and get the same generic delivery experience.

Jubilant Foodworks Netherlands B.V. (“JFN”), wholly owned subsidiary of the Company has increased its stake By 2.06 % Stake in DP Eurasia through various on-market purchases For GBP 1,664,874.

As on July 17, 2022, JFN is holding 6,50,60,801 ordinary shares in DPEU representing 44.75% of its issued share capital.

Is it diworsification? Is buying a tech company needed? Of course it is a saas tech for food delivery but…

I guess as Domino’s may delist themselves from Swiggy n Zomato they are trying to back-up option of their own.

It’s not “diworsification”. It’s a step towards further reducing delivery times ( I already cant understand how they deliver in < 20 mins). These steps are part of a bigger process where Dominos aims to improve both availability and delivery times. The more resilient and the lesser the impact of the points of failure your network is/has, the better will be customer satisfaction and wastage of inventory.

Management denied these reports in recent concall. They consider both of them as strong delivery channels. Although they continue to drive and experiment more with deliveries from house channel, I doubt the volumes from in house app will be even close to what they will be getting from these apps. Unfortunately, no analyst asked this in the call. Maybe worth trying to get numbers on these from investor relations.