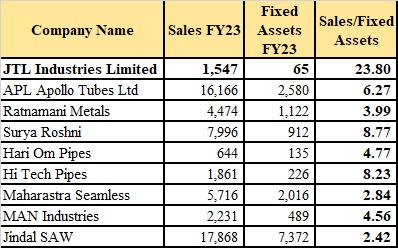

I was comparing fixed asset turnover across the structural steel pipe industry and i got a interesting data set

the JTL has the smallest asset base and the highest fixed asset turnover but given there revenue of 1547 crores the closest player Hi tech pipe has an asset base of 226 crores and even hari om pipe with sales of 644 crores has an asset base of 135 crores so how they are able to achieve fixed asset turnover of 24x while other players are able to generate only 4-8x of fixed asset turnover

if anybody has possible reason for it or have visited there plant and knows the answer pls reply as it would be of great help.

Yes the number is way to good to believe and is unreasonable because it’s not possible for a manufacturing company to achieve this level of asset turnover number.

As per there IR the thing which was said to me was that when the companies consolidated its assets at that time it was don’t at cost value rather than at fair value that’s why asset based is so small

As per Indian Accounting Standard 16 a company at its discretion can follow whether cost model or fair value model for subsequent measurement of the assets and once choosen the company has to adopt to that particular model indefinitely so that’s not the problem the problem is that it’s understandable that there land cost is very low but what about fresh capex that was done in recent years what about cost of machinery that was incurred? Because from 2021 to 2024 company has increased its capacity from 1 lakh ton to 6 lakhs ton that’s why

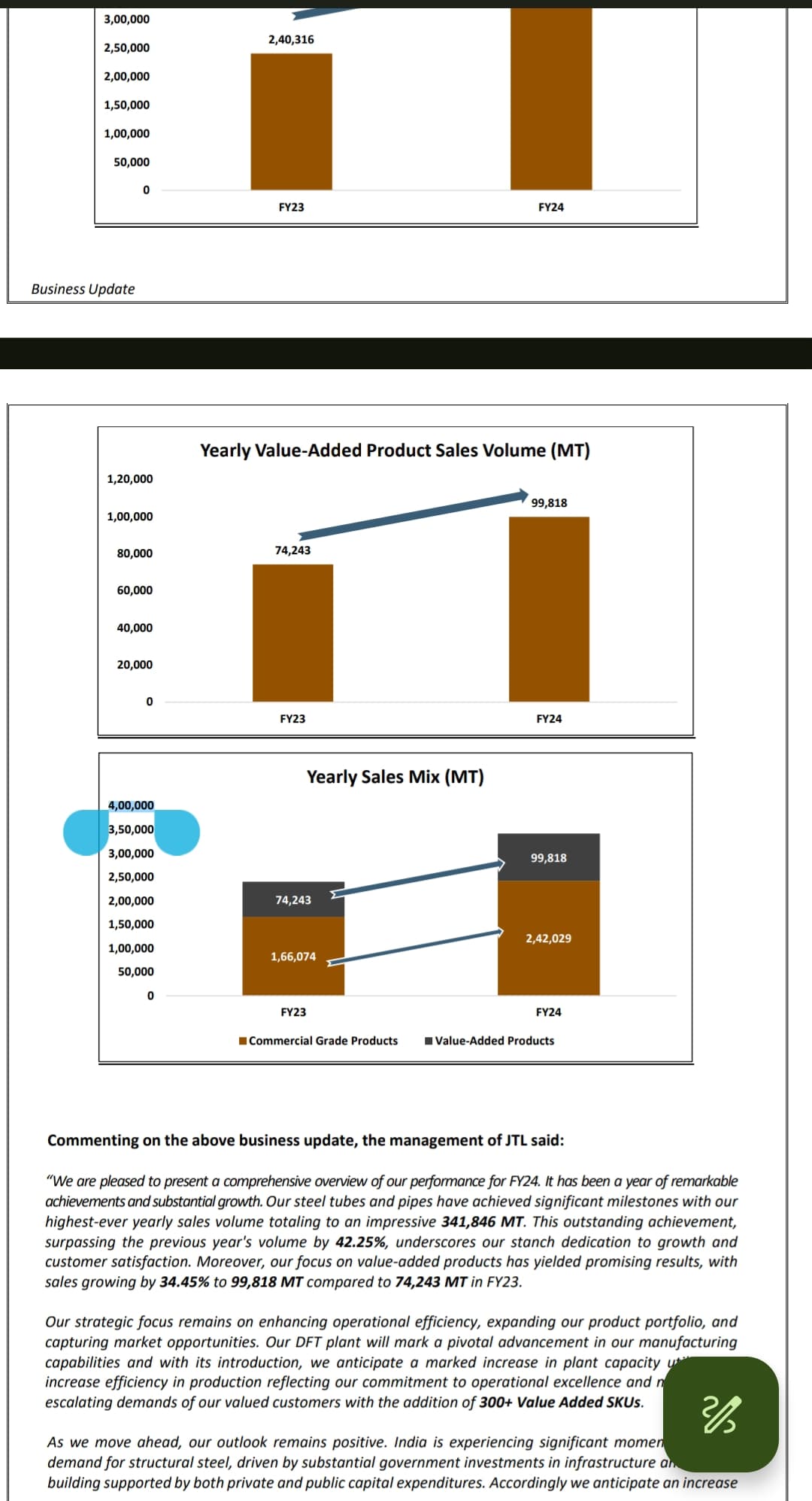

I had observed in the annual turnover report that Q4 growth is only 2 odd % on yoy basis. The numbers are reported on annual basis so this data is not presented.

I have arrived at this data by deducting the 9-month production from the 12-months production.

Thus can we expect a big jump in topline yoy for Q4?

There will be good jump in topline on annual basis like historically there sales per tonne has remained in line of 45k to 50k but this time i expect it to be in line of 50k to 60k per tonne so good jump in numbers esp revenue is expected but at the same time margin may take a bump due to on going capex and heightened metal prices.