Company Overview:

JTEKT India Limited established in 1984, manufacturers steering systems for the passenger car and utility vehicle market in India, catering to passenger cars, utility vehicles and light commercial vehicles. The Company gets its technology from JTEKT Corporation, Japan the largest producer of passenger vehicles’ steering systems in the world.

JTEKT India earlier called Sona Koya and was headed by Sanjay Kapoor. In 2017, JTEKT Corporation bought Sanjay Kapoor’s 25% stake in the company. JTEKT was already associated with the company for many years and was also providing technology support. JTEKT Corporation, the parent company of JTEKT India, is the world’s largest steering company. It operates in several areas such as steering systems, electric power steering (CEPS), machinery, and bearings. JTEKT Corporation have an annual revenue of around ₹1 lakh crore plus.

The company is part of the Toyota Group. Out of 1L Cr Revenue of Jtekt Corp, Jtekt India has approx. 2400 Cr revenue. Apart from Jtekt India, Jtekt corp also has 2 other unlisted entities in India: Jtekt Machinery and Jtekt Bearings. JTEKT India customer base includes major vehicle manufactures in India such as Maruti Suzuki, Toyota, Tata Motors, Mahindra & Mahindra, Isuzu Motors, Honda and Renault Nissan. Company is supplying to all major car manufacturers except Hyundai group because they are taking from Mando (Anand Group Company).

The Company has operations across India through its 7 Plants (1 plants in Gurgaon, 3 plants in Dharuhera, 1 plant in Chennai, & 2 in Bawal).

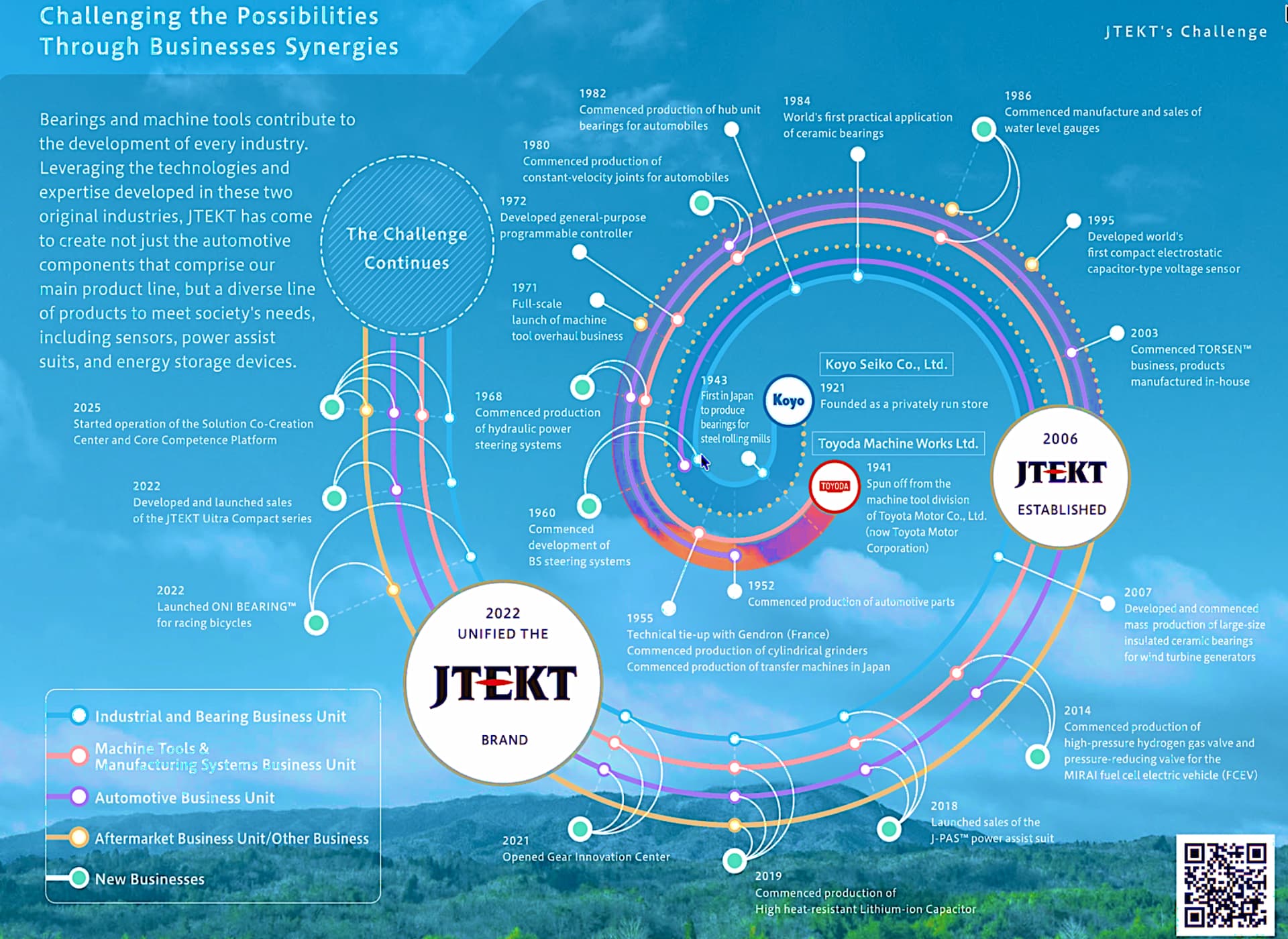

JTEKT GROUP

In 1921, Koyo Seiko started as a small bearing shop, and in 1941 Toyoda Machine Works spun off from Toyota to make machine tools. Together they began building Japan’s strength in bearings and machine tools, supplying parts for steel mills, factories, and later, automobiles. Over the next decades, they moved from simple bearings and steering systems to advanced automotive parts and precision machines.

By the 1980s and 1990s, their products were powering cars, plants, and new technologies like ceramic bearings and smart voltage sensors etc. In 2006, both companies united and form JTEKT, combining bearings, machine tools, and automotive components into a single, powerful group. From that point, JTEKT moved into more advanced technologies. It began making hydrogen valves for fuel-cell vehicles, heat-resistant lithium-ion capacitors, and power-assist suits that help people move more easily. The company also introduced smaller, more compact products and opened a Gear Innovation Center to develop new ideas faster. In 2022, all of JTEKT’s businesses were brought together under one brand. This made it easier for the company to offer everything from basic bearings to smart, modern solutions that support industries, transportation, and everyday life.

Product Overview

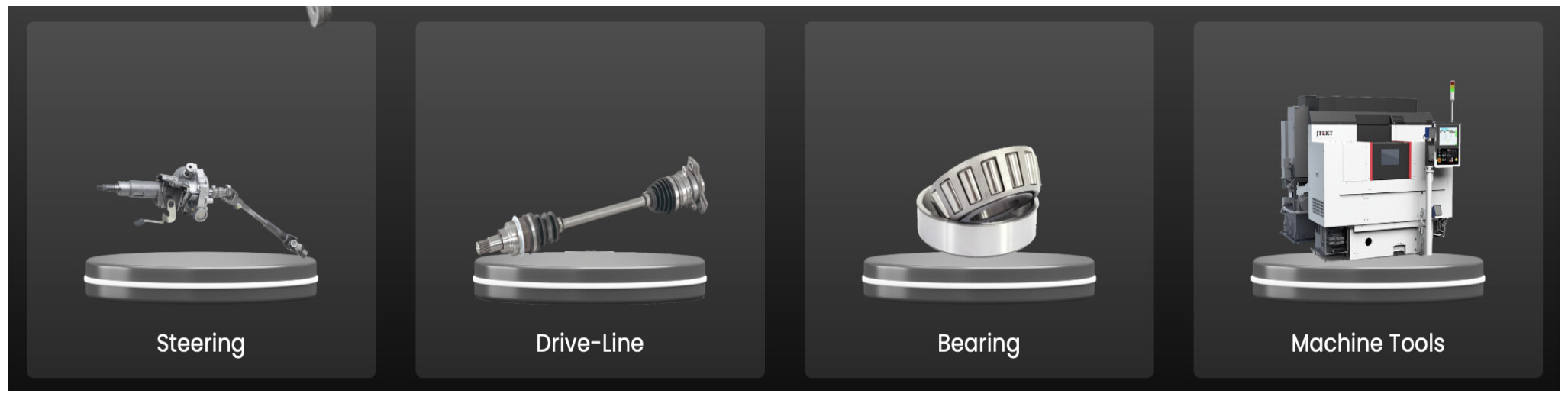

Company deals in 4 Categories of products which are as follows:

Steering Components

1. Steering Column:

The steering column is a shaft and housing assembly that transmits the driver’s rotational input from the steering wheel down to the steering gear or rack-and-pinion, which then turns the road wheels. It also typically includes bearings and joints so the shaft can rotate smoothly and handle slight angles between the wheel and the steering rack.

JTEKT India majorly manufacturing 3 types of products under Steering Column which are as follows:

-

C-EPS (Column Type Electric Power Steering)

Column Electric Power Steering (CEPS) is an advanced type of steering system that uses an electric motor to help the driver turn the steering wheel. The motor is fitted on the steering column and reduces the effort needed to steer the vehicle. This makes it lighter, easier to maintain, and more efficient. CEPS also uses less energy and can easily work with other electronic features in modern vehicles, such as driver-assistance systems. -

Manual Column

The steering column is an important part of a vehicle’s steering system. It connects the steering wheel to the steering gear and helps turn the wheels when the driver moves the steering wheel. It is made to be strong and safe. Many steering coloumn can be adjusted to make the steering wheel more comfortable to use. -

Inermediate Shaft

The intermediate shaft is a part of the steering system that connects the steering wheel to the steering gear or rack. It helps pass the turning motion from the steering wheel to the wheels of the car. The shaft usually has joints or flexible parts that let it move smoothly, even when the steering parts are not perfectly aligned. This helps reduce vibrations and ensures the steering feels smooth, stable, and safe.

2. Steering Gears:

Steering gears are the core mechanisms in vehicles that translate the rotation of the steering wheel into the movement of the wheels, allowing the driver to control the direction of the vehicle. These gears sit between the steering column and the steering linkage, converting the rotary motion from the steering wheel into lateral or linear motion that turns the wheels.

Company is making 3 types of products under this segment:

-

R&P Gear (Rack & Pinion type)

The rack and pinion gear is an important part of a car’s steering system. It helps change the turning motion of the steering wheel into a back-and-forth motion that turns the car’s wheels. The system has two parts — a pinion gear, which is connected to the steering wheel, and a rack gear, which is linked to the steering arms. When you turn the steering wheel, the pinion gear turns and moves the rack, making the wheels turn in the same direction. This system gives smooth, quick, and accurate steering. -

RBS Gear (Recirculating Ball Screw type)

The recirculating ball steering system is a type of steering mechanism that helps make turning the wheels smooth and easy. It works by using many small ball bearings that move around inside a track. These ball bearings roll between a spiral-shaped part (called the worm screw) and a nut to reduce friction. When you turn the steering wheel, the worm screw rotates, and the ball bearings help turn this rotation into a straight, back-and-forth movement that turns the vehicle’s wheels. This system is strong, reliable, and ideal for heavy vehicles or those that need precise steering control. -

Hydraulic Rack and Pinion Gear

The hydraulic rack and pinion system helps make steering easier. It works like a normal rack and pinion gear but adds hydraulic (fluid) power to assist the driver. The system uses pistons filled with fluid that help move the steering rack, so the driver doesn’t have to use as much force. A pump connected to the engine supplies this fluid power, making steering smooth and easy, especially at low speeds or while parking.

Driveline Components

1. Drive Shaft:

A drive shaft is a strong metal rod in a vehicle that carries power from the engine and gearbox to the wheels so the car can move.

- Constant Velocity Joints

CV joint is designed to handle changes in angle and high torque so that the car accelerates smoothly and the ride feels stable and comfortable.

There are 2 types of CV Joints i.e. long stem CVJ and Short stem CVJ:

A long-stem CV joint is a type of car part that sends power from the gearbox to the wheels while allowing the shaft to bend at different angles without vibration, usually used in front-wheel-drive cars where more movement and flexibility are needed.

A short-stem CV joint does the same job of sending power smoothly to the wheels, but it is shorter and more compact, so it is preferred where there is less space, such as in many rear-wheel-drive or all-wheel-drive vehicles.

2. Ball Hub Unit:

A hub unit (wheel hub unit) is the integrated assembly that connects the wheel to the suspension/axle, supports the vehicle’s weight, and lets the wheel rotate smoothly on its bearings.There are 2 types of Ball hub unit i.e. Driven and Not Driven Hub unit. Driven hub unit is fitted to the drive shaft and also transmits engine torque to the wheel, so it both supports and drives the wheel (used on powered axles in FWD, RWD, AWD).

Non-driven hub unit is not connected to the powertrain; it only supports the wheel and lets it free-roll on non-powered axles.

Company is also into Bearing Manufacturing and Machines tools like CNC Machines as well but at very small level at present.

Segment Wise Revenue Bifurcation:

This trend shows Driveline revenue contribution decreased significantly in last 2 years but know reviving again, the revenue from driveline segment had not reduced but the revenue contribution from steering column increased significantly which ultimately lower Driveline share in % terms. But now, driveline again started increasing because of increase capacity and new orders kicking in for CVJ.

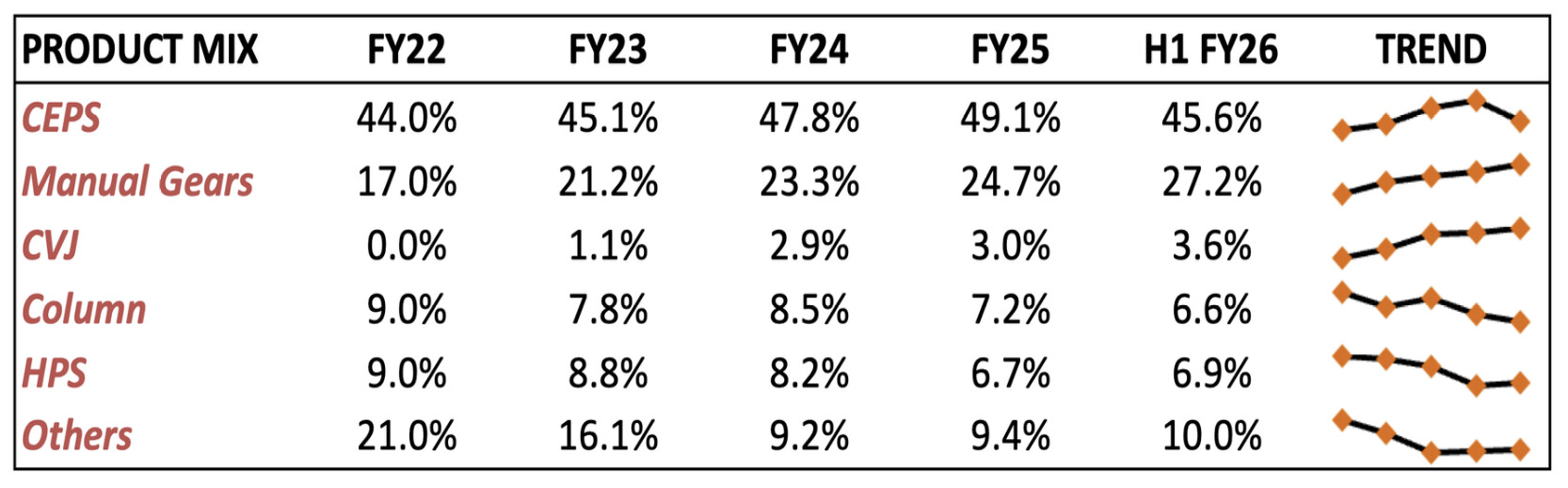

Product Wise Revenue Bifurcation:

Above trend shows CEPS is the highest contributor in revenue as a whole, because company has big manufacturing capacity of CEPS and this product average cost per vehicle is highest in all the product company is manufacturing. This trend also showing decline in CEPS contribution not because of decrease in the sales but increase in the sales of other products, as company is focusing on Driveline products which has better margins.

Geography Wise Revenue Bifurcation:

Revenue from exports was decreased significantly in last year and current year. In current year it was dropped because of US tariffs but company has very good number of orders from its group company (Jtekt Brazil) which will be pan out in next years. That will increase export contribution significantly and Company is also working with some US companies for export orders, once tariff situation become normal that also starting coming in.

INDUSTRY OVERVIEW

The company operates in the Indian auto components industry, which is currently worth about ₹5-6 Lakh Cr. This industry is expected to grow steadily over the next few years. The growth will mainly come from higher car and utility vehicle sales, rising exports, and more parts being used in each vehicle.

Within this industry, the automotive steering system market in India is growing even faster. It is expected to increase from around USD 4.7 billion in 2017 to about USD 10 billion by 2026, which means strong annual growth of around 9%. Most of this growth will come from direct sales to vehicle manufacturers (OEMs).

Steering and driveline parts are very important for vehicle safety and are difficult to manufacture. Because of this, only experienced and well-established companies can compete in this segment. Large Tier-1 suppliers such as JTEKT, Rane, ZF, and Mando are well placed to benefit from this growth.

JTEKT India is the largest maker of steering systems in India for passenger cars, SUVs and light commercial vehicles. It supplies key steering parts—such as steering gears, steering columns, and rack-and-pinion systems—to almost all major car manufacturers in India.

As the auto industry is moving from hydraulic systems to electric steering, JTEKT India is well placed to benefit from this shift. JTEKT India is backed by JTEKT Corporation of Japan, one of the world’s leading steering companies. This gives JTEKT India access to tested global designs, advanced technology, and know-how to make products locally, helping it stay ahead of Indian competitors.

Apart from steering systems, the JTEKT Group in India also works in driveline parts, bearings, and machine tools under its “ONE JTEKT” approach. JTEKT India manufactures important driveline components such as differentials, axle parts, rear axles, propeller shafts, and CV joints. These parts help vehicles run smoothly, quietly, efficiently, and last longer, especially in passenger and utility vehicles.

Impact of EV and technology advancement on the Industry:

Steering and driveline are directly affected by stricter safety norms, improved crash standards and increasing fitment of stability/ADAS features, which favour advanced EPS and high-precision mechanicals. EVs and hybrids still require steering, hubs, bearings and many driveline elements (with some redesign), so content-per-vehicle can stay stable or even increase for sophisticated EPS and CVJ solutions, rather than structurally disappearing.

At the same time, OEM pressure on cost, localisation of electronics, and compliance with Indian government schemes and tariff structures shape the industry’s margin profile and capex intensity.

Competitive Landscape and Industry Risks

Key competitors in the Indian steering industry are Rane (for steering gear and linkage), ZF, Mando, and some global Tier-1 suppliers that work through joint ventures. Competition mainly depends on technology, product quality, cost, and relationships with vehicle makers (OEMs).

The main risks for the industry are: car demand moves in cycles, raw material prices can change a lot, steering technology is changing fast (for example, steer-by-wire in the long term), steering systems use more and more electronics, and strong OEMs can push down supplier margins.

For JTEKT India, the key points to track are that it depends on a few big OEM customers and must keep investing in electronics for EPS and in localising parts made in India and must be working for future technology.

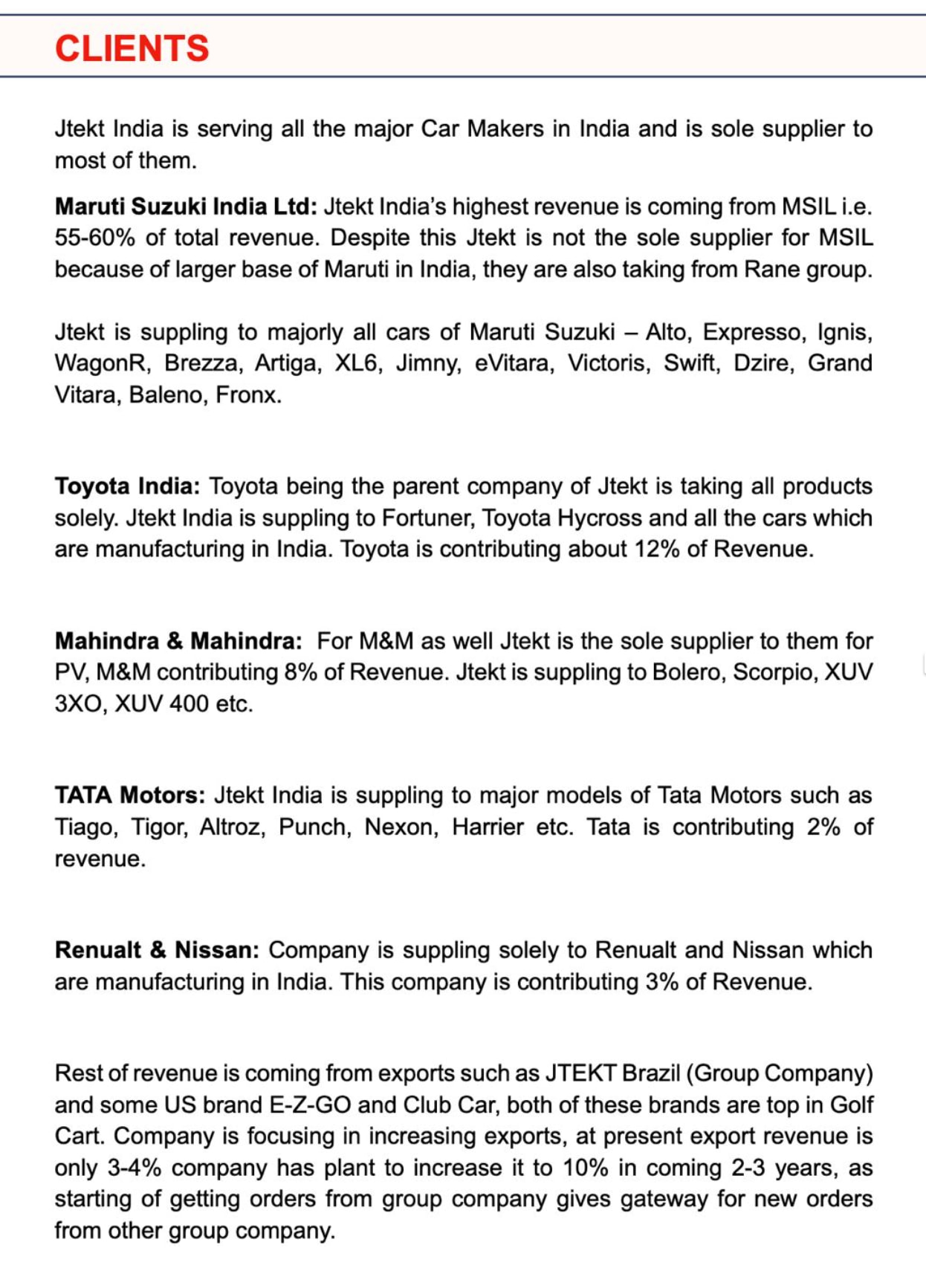

CLIENTS

Jtekt India is serving all the major Car Makers in India and is sole supplier to most of them.

Maruti Suzuki India Ltd: Jtekt India’s highest revenue is coming from MSIL i.e. 55-60% of total revenue. Despite this Jtekt is not the sole supplier for MSIL because of larger base of Maruti in India, they are also taking from Rane group. Jtekt is suppling to majorly all cars of Maruti Suzuki – Alto, Expresso, Ignis, WagonR, Brezza, Artiga, XL6, Jimny, eVitara, Victoris, Swift, Dzire, Grand Vitara, Baleno, Fronx.

Toyota India: Toyota being the parent company of Jtekt is taking all products solely. Jtekt India is suppling to Fortuner, Toyota Hycross and all the cars which are manufacturing in India. Toyota is contributing about 12% of Revenue.

Mahindra & Mahindra: For M&M as well Jtekt is the sole supplier to them for PV, M&M contributing 8% of Revenue. Jtekt is suppling to Bolero, Scorpio, XUV 3XO, XUV 400 etc.

TATA Motors: Jtekt India is suppling to major models of Tata Motors such as Tiago, Tigor, Altroz, Punch, Nexon, Harrier etc. Tata is contributing 2% of revenue.

Renualt & Nissan: Company is suppling solely to Renualt and Nissan which are manufacturing in India. This company is contributing 3% of Revenue.

Rest of revenue is coming from exports such as JTEKT Brazil (Group Company) and some US brand E-Z-GO and Club Car, both of these brands are top in Golf Cart. Company is focusing in increasing exports, at present export revenue is only 3-4% company has plant to increase it to 10% in coming 2-3 years, as starting of getting orders from group company gives gateway for new orders from other group company.

MANAGEMENT ANALYSIS

JTEKT India is run by a team that has a mix of international and local experience, showing both its Japanese Expertise and Indian presence. In 2025, there were some changes in the leadership, with new leaders, which has made the company stronger in planning and running its operations.

Key Management Personnel

-

Minoru Sugisawa:

Chairman & Managing Director, overseeing overall strategy and governance. His appointment in 2025 marks a dedicated focus on the company’s long-term direction and day-to-day operations. Minoru has over 30 years of experience in production administration and steering & drivelines technology. He joined JTEKT India on March 30, 2021, as Senior Vice President, overseeing production administration before progressing to his current leadership role. -

Rajiv Chanana:

Director & CFO, responsible for finance and strategic planning. Reappointed as Whole Time Director in June 2025, highlighting his critical role in financial management and growth initiatives. Chanana joined JTEKT India in 2009 as CFO and has since played a pivotal role in the company’s financial strategy, investment planning, and regulatory compliance. He is leading company since last 16 years, know all in and out about the company and regulation works etc. -

Yosuke Fujiwara:

Whole Time Director, supporting operational execution and management oversight. He is a Japanese national with over 25 years of experience in the automotive industry, having previously served as Managing Director of JTEKT Bearings India Private Limited.

JTEKT India’s management combines Japanese efficiency with an understanding of the Indian market. The board includes both international and local experts to ensure good governance and smart decisions. The recent leadership changes show a focus on stability, growth, financial discipline, and strong compliance.

BUSINESS INSIGHTS

- Company has total of 8 Manufacturing facilities at various locations in India (Gurugram, Dharuhera, Bawal in Haryana, Chennai in Tamil Nadu and expandind with new facility in Sanand, Gujarat)

Having a total capacity of:

Manual Steering Gears – 32 Lakh units annually

CEPS – 15 Lakh units annually

Constant Velocity Joints (CVJ) – 8 Lakh units annually

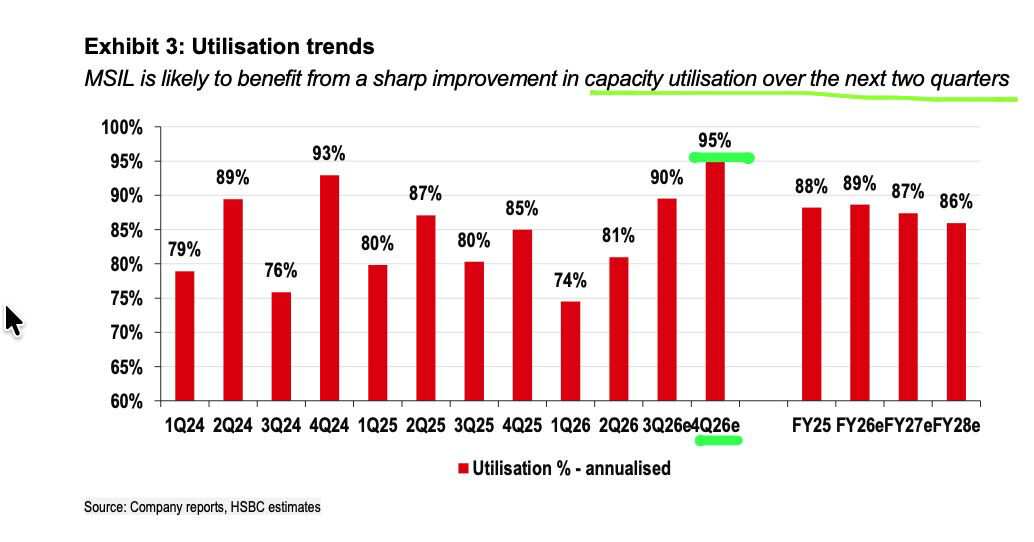

Company has doubled its capacity in current and last year as they have reached to 90% capacity utilisation levels last year.

-

Parent Company JTEKT Corp had announced ₹1800 Cr capex in INDIA, Jtekt India has already done ₹760 odd Cr of capex in last 3 years and also doing large greenfield project in Gujarat to serve fast growing western OEMs, this greenfield capex cost around ₹250-300 Cr. This greenfield capex will be completed by early 2028.

Company’s capex plan is majorly focusing on upcoming demand from Export oriented plan of Vechile manufacturers in India with rising EV penetration and company also working on more localisation and backward integration. -

Capex funding is incurred from internal accruals and recent right issue done by company. Right issue was of 249 Cr out of which 114 Cr will be used for Greenfield project and rest will be purchase of plants and machineries which helps in backward integration of forging parts of CVJ.

-

In right issue Jtekt Japan and Maruti Suzuki also participated.

-

All the capex which is going on have an asset turn of around 3-4x which means company can generate huge revenue from this on going capex.

-

Company is aiming for 10% of total revenue from exports over next few years. Recent Jtekt Brazil order will increase exports by 2% of totalrevenue and also unlock exports opportunities for other group companies.

• Impact of EV:

– Government has reduced import duty tariffs on EV components but increase duties on ICE, despite duties reduction on EV, company is 100% supplier of upcoming EV Vehicles of Maruti and Toyota.

– Maruti also is in board of Jtekt India and Toyota is the parent company of Jtekt gives the edge to the company.

– Maruti is going to implement EV infra structure all over the INDIA and planning to launch many new EVs in coming years, this will increase business opportunity for Jtekt as being the biggest supplier for the company.

– Company also started supply to TATA’s new EV CORAL which is small pick up truck.

-

Company is focusing to supply higher value products i.e. complex steering system components. Management also stated that in some models company is suppling both Manual Steering Gears and Electric Column which effectively doubling content per vehicle.

-

Average price of CEPS is ₹12000 and CVJ is ₹6000, bigger cars cost higher for these products and as per the growing trend in Indian markets sales of SUVs increases significantly leads to higher content per vehicle also helps in increasing revenue growth.

-

Company is also focusing on premium cars segment as it has better margins and higher value, CVJ is one of that product which is needed for higher end drivetrains. This reflects company is working on premiumisation as well.

-

Company is aiming for 10% of total revenue from exports over next few years. Recent Jtekt Brazil order will increase exports by 2% of total revenue and also unlock exports opportunities for other group companies.

-

Company is also working on future ADAS i.e Steer by wire technology which is majorly used in future by replacing mechanical steering link to digital.

-

In last 4-5 years, company has reduced manpower cost from 13.5% in FY20 to 10% currently. Despite that margin reduced in last 5 years due to certain factors, going forward margins will be improve.

-

Margins levels of all the product are more or less similar except CEPS and CVJ as they need higher tech advancements which leads to better margins in these products.

-

Company has worked on localisation in recent years, at present 10% of material consumed is coming from imports. Company is working to reduce that as well in coming years. This helps in margin improvement and easy accessibility.

-

Company is complete system provider (i.e supply all 3 products MS Gear, CVJ and CEPS) in eVitara Model of Maruti Suzuki whether exported or domestic sales.

-

Company is suppling CVJ to only 2 OEMs which is 5% market share, company is expecting to touch 7.5-10% market share in next 2 years.

KEY TRIGGERS

1. EV Expansion –

Being the supplier to Maruti and Toyota, these company started rolling out their EVs in the market and Jtekt India is the sole supplier at present, gives huge opportunity to grow in this space. Maruti once start rolling out may capture EV market very fast as being the market leader. At present, in first Maruti EV i.e. eVitara company is supplying complete steering system which means higher content per vehicle. Management Believes, they will supply to complete system in upcoming models as well.

2. Export Opportunities –

Company is currently supplying to US golf cart OEMs because of tariff issue this segment suffers this year but this is short term problem which will get back in some time. Second is company received big order from group company Jtekt Brazil. Management belives once the first order rollout, further order opportunity will unlock and export can reach to 10% of total revenue in coming few years.

3. New Product Introduction and Backward Integration –

Company is planning to manufacture Jacket Assembly which is many component of CEPS in house, which help is backward integration and helps in increasing margin. Company also developing more new products, some of the smallers parts of existing product etc and exploring new opportunities like future ADAS (Steer by wire). This helps company not to stop at single point and keeps on getting new business.

4. Prime Customers Expansion plans –

Maruti Suzuki and Toyota recently announced huge capex to increase vehicle production capacity annually. These capex are majorly done for increase the export of cars from India to the world. Major expansion to be done in Gujarat or western side of India. Jtekt is also doing Greenfield expansion in Gujarat which is very near to Maruti New plant. This can be the growth trigger for Jtekt India as the key supplier of these vehicle manufacturers.

5. Capex Realisation –

Jtekt India as done around ₹800 Cr of capex in recent years and about ₹300 Cr is already announced for next 2 years. This gives company a better space to catter more business and all these capex was done after full utilisation of last capacity. Asset Turn is over 4x as per past performance and management is also assuming the same given that if we consider 3x aswell there will be big revenue potential in the company for coming years supported by exports and EV rollouts.

6. GST Cut and Increasing Disposable Income –

Indian government cut taxation significantly on Vehicles and also giving benefits in Income tax which further increase disposable income of people of India all these factors increases the demand of PV and leads to more demand for company as well.

KEY RISK / CHALLENGES

1. Customer Concentration –

Around 95% of revenues come from passenger vehicle OEMs. This high concentration exposes the company to downturns or order cuts from a few large clients. Maruti contribution 55% of revenue, any disruption in orders may lead to significant impact on company performance.

2. Increasing Competition in steering systems market –

There is a stiff competition from other steering system manufacturers, which resulted in loss of business for a few key models in the past. Nevertheless, the company maintains a strong relation with various OEMs and has been able to gain business for recent product launches of various OEMs.

3. Significant capex plans over the medium term to constrain improvement in return indicators –

Company has material capex plans over the next two fiscals towards capacity expansion and new plant addition. The funding mix for the capex plans and its impact on the credit profile would be monitored.

4. Disruption in Supply Chain –

If there will be any issues with supply chain like unavailablity of key components may leads to delay in deliveries. For this company is focusing on increasing localisation.

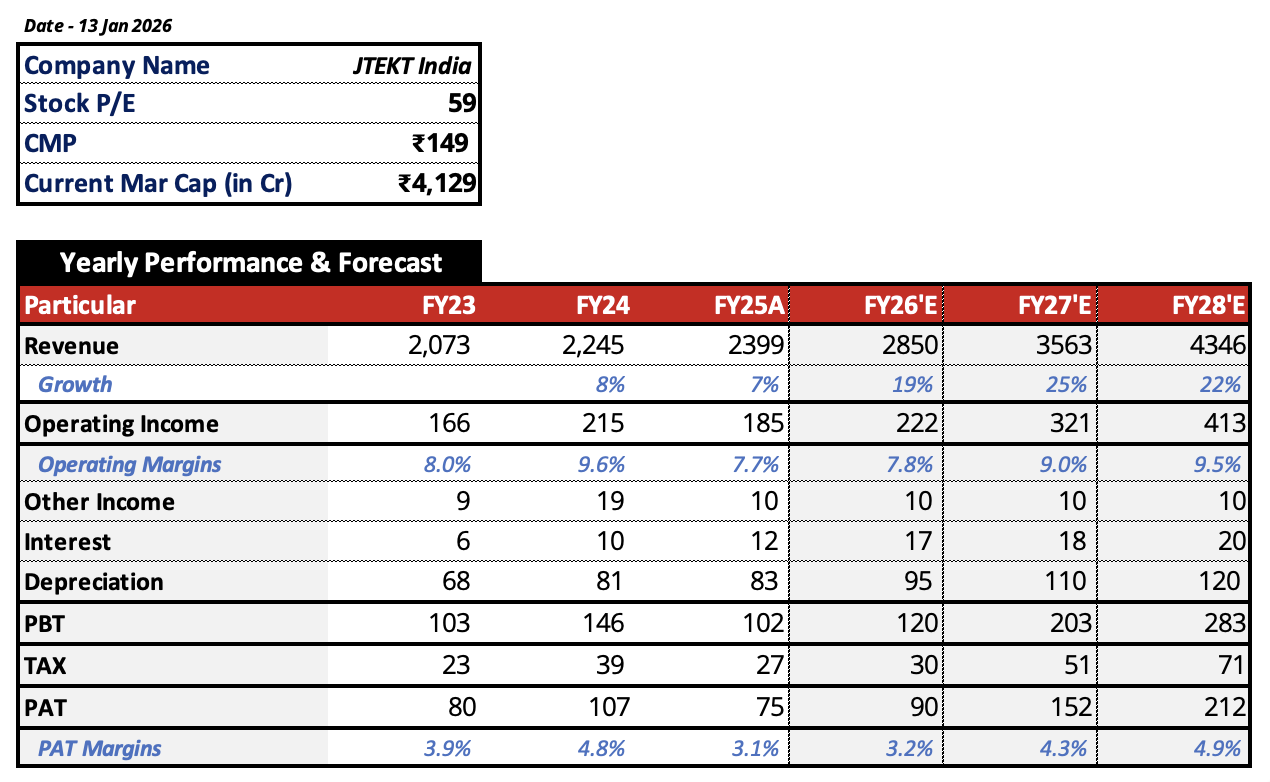

Financial Overview

Assumptions Behind Forecast:

REVENUE -

- FY26: GST Rate cut is the biggest boost and leads to increase in demand of their prime customers, capacity increased in H2 will drive volumes.

- FY27: Bulk capex of 800 Cr will be fully operational, capacity starts ramping up, Export orders delivery will start, Assets turnover of 4x as stated by management starts playing out.

- FY28: Capacity utilisation starts picking up, major greenfield capex in Gujarat also commences commercial production, Export market establise with newer opportunity, EV launches by prime customer will boost demand significantly as content per vehicle in new EVs is much higher.

EBITDA/OPERATING INCOME -

- FY26: H1 margins were 6.3% due to high employee cost and lower fixed cost absorption, good demand in H2 will improves margin by playing operating leverage, Management also stated administration cost will peak out no further increase in that. This whole will stable whole year margins.

- FY27: Employee cost expansion stops, export revenue has higher margins and company also doing backward integration both this thing improves margins to good level.

- FY28: Export business stabilises at higher rate, capacity utilisation at higher rates improves operating margins. Management also focusing on localisation which will peak in FY28 leads to better margins. Contribution of higher margin products will increase by FY28 as well.

BALANCE SHEET IMPACT -

- Gujarat Plant: Massive Capex (₹300 Cr odd) for the Gujarat facility (completion expected early FY28). Depreciation will majorly peak hear as there will not be much bigger capex at that time

- Debt: Borrowings will likely peak in FY28 to fund this, increasing finance costs slightly, but strong cash accruals make comfortable for the company to manage finance costs.

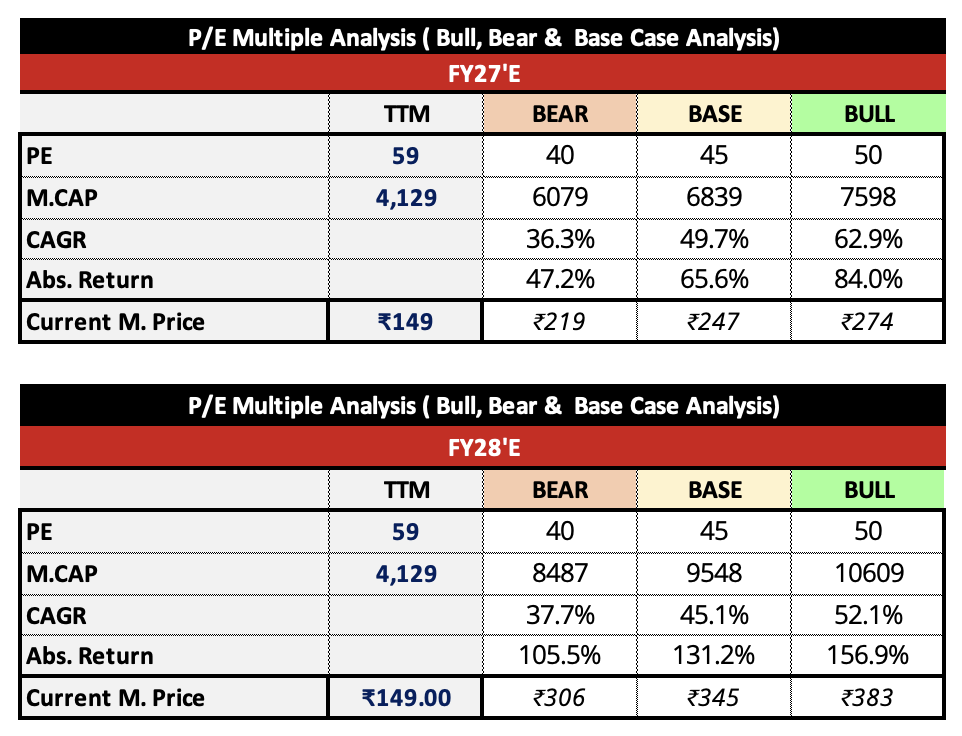

WHY SHOULD WE CONSIDER THIS?

In Auto Ancillaries there are some key things to monitor for future growth and good momentum which are as follow:

- EV Agnostic

- Export Oriented

- Multiple OEMs

- Working toward Premiumisation

- R&D Heavy

If we see Jtekt India is optimally suited to all the above matrices, company is EV agnostic, looking for export opportunities, having multiple OEMs, working towards Premiumisation for drivetrain components and also doing R&D for future technologies.

Additionally, some supporting elements also playing out in the present time such as GST Cut and Increasing EV penetration which further boost the growth for the company. And if we see long term factors which may also helps the business is taxation reliefs by government leads to higher disposable income leads to more demand in the economy.

Secondly, India has only 30 cars per 1000 people where as developed economy has 500-600 cars per 1000 people, there is a huge gap available. Ultimately these things support company’s growth in background and play major role in it.

Disclaimer: Invested, Above forecasts are based on assumptions and do thorough research before investing.