My observation is any price above 4000 yuan per ton, which is roughly 41k INR per ton, Indian steel mills are profitable

Below this, the mills struggle

4k yuan per ton was Q4 average prices

Right now we can see spot is at least 500 yuan more

So 10% more realization and mostly higher EDITDA at least 5% more margins (rough estimate given higher jaws)

So basically we can expect good results June quarter for all steel companies

In fact better than March quarter

Monnet thesis -

As is known Monnet was taken over by JSW and Aoin via NCLT process

Steel products are many types- broadly intermediaries and finished steel. Steel mills buy iron ore and coal and first convert to steel pellets first. Then they process pellets to finished products.

In case of monnet they have a 2.4 million ton plant

And all they were doing so fat is producing pellets

That’s low margin business

Pellets sell for 25000 Rs per ton approx. So margin is 1000 Rs per ton approx.

So 2.4 mtpa implies 240 Cr EBITDA per annum, if they do just pellets

I see they are 100% utilized producing pellets

Now from 2020 Jan quarter they started converting pellets to end products - billets and TMT bars

Realization is 45000 Rs per ton

Margin is 10000 Rs per ton

For Jan quarter they did 135kt of these end product’s

Implies 135 Cr EBITDA + pellet EBITDA of some 50 Cr

That’s why we are seeing 200 Cr EBITDA

Now last year they did very less of these end products

Next Year guidance has been released

They said they can do 630kt end products

That’s 650 Cr EBITDA p.a.

Plus some 200 Cr from selling rest as pellet

If we see capacity is 2.4mtpa

630kt is roughly 1/3rd only, Rest is pellets.

So for FY22 , if prices sustain, we can see 800 Cr EBITDA

Less interest and amortization of 500 Cr

That’s 300 Cr pre tax profit

And post tax some 250 Cr. . That implies forward PE of 8x roughly

Which is fair. .

What’s interesting is when they ramp up end product sales - 2.4mtpa at 10000 Rs, Implies 2400 Cr EBITDA

Assume margin dips to 5000 Rs. . (That’s super bear case)

EBITDA = 1200-2400 cr

That implies forward PE of 1x

But for long term… and assume prices hold and assume they don’t take more debt or expand etc

Risks to the above -

They are steadily ramping up - operational issues in ramping up will be very costly for minority investors

Price wise… this is a manipulated stock… Lower circuits and upper circuits imply rampant trading and speculation

Steel.prices should sustain these high levels.

On supply side

-. The issue is companies will.come up with expansion plans

-. Jsw steel said they are going to become 38mt pa very soon

That’s massive…

Opportunities-

For any new mill to be put up it takes 2-3 years

Even jsw steel takes time

So price looks safe for 1-2 years

Unless China takes a U turn and starts manufacturing steel at cheap prices like before

N they set up plants very quickly too

Will impact prices

Please offer your critical view of the above.

Disclosure: invested 33% of my overall portfolio. Average buy price is 38 Rs hence I am already sitting on a good profit. Please don’t buy just based on above. Please do your own analysis.

All the above figures are approximate numbers to derive a back of the envelope calculation only

Thanks Siva, will check with my friends in steel and confirm in a day or two. in the mean time. what i could make out is

china has stopped export subsidy of 13% and shut some of the most polluting units leading to 50 MT reduction in exports from 2015 levels. commensurate capacity yet to come up. which means pricing stability till supply exceeds demand. Corp Presentation_-pages-25.pdf (1.2 MB)

am attaching the aionjsw corp ppt which very well indicates the industry and monnets turnaround as well as future path.

Thanks for your replies Ashish, Monnet appears to be well poised to gain from a turnaround perspective. It will be good to understand the end users of Monnet and whether they are exporting now? Also top head has changed recently. It will be good to know about him too

I’ve very recently started researching the business. Which all competitors would be closest in terms of product portfolio from the listed space (or even unlisted)?

Hi Arpit, steel is a commodity business. All JSW Ispat produces is steel billets and tmt bars. Tata steel long is a comparable for tmt bars. For billets many players are there including JSPL. Idea about this company is turnaround and ramp up. Geographically they are placed in Raipur and Raigarh. Nor sure whether they are exporting and who the end consumers are… would be good to know for sure

really good work Shiva.

What about raw material integration?

As far as I understand it has coal mines but for iron ore the company depends on the the parent.

Hi Vikas, thanks a lot. If a company has captive mines margins are going to be higher. In case of Jindal Steel and Power, operating margin is as high as 45%. In case of JSW Ispat, I can see raw materials are linked so supply is assured. They do buy iron ore from JDW steel, margin would still be 20%+

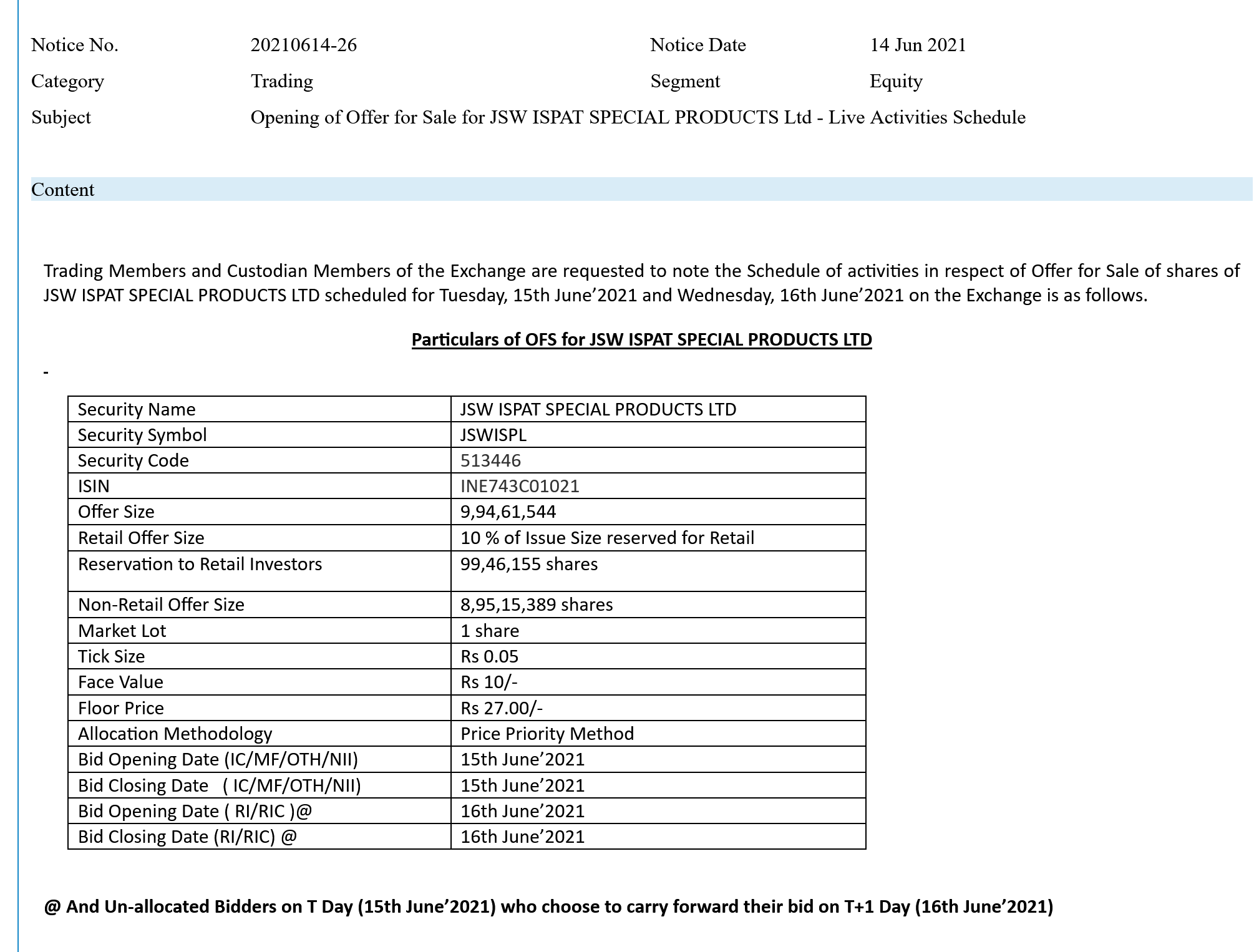

The Floor price declared is just the price fixed at the discretion of the seller(holding at least 10% of share capital) below which no bids can be placed and probably have fixed a low price(compared to the CMP) to garner higher interest from market participants.

The discovered price will likely be much higher.

The issue will be open for Retail(10% reservation) on the 16’th.

If anyone is interested in tracking the OFS (today non-retail window and tomorrow retail) below are the links. It is interesting to watch the build up - bid details and the indicative price as the day progresses.

Well can someone give more guidance on what bid price to be placed for this OFS - higher side or the lower band? In case one would want to ride the commodity cycle?

This OFS is based on Price Priority - there will be multiple clearing prices and the higher price you bid more likely you will get allotment. So you can apply at any price based on your risk appetite but allocation will be based on the demand. You can check the live bid status on NSE and BSE to see where bids are concentrated, and then make informed bids. You can refer below article for details:

Thank you so much. Based on the current bids the concentration today is happening at around base price however indicative price is showing around 28, this is non retail ofcourse.

Is my assumption and reading correct based on what I see on NSE website?

However this OFS is over subscribed already, does that means one needs to bid for the upper price band? Or around (read above) the concentrated bids?

You are right, you have to bid above the indicative price to get the allotment and the indicative price tend to swing largely towards the end of the session - that is when the institutions and HNIs bid (there is always a lag between the live price and the actual price so you have to take that into consideration while bidding). Don’t be surprised if the final price comes very close to today’s market price (around 54).

So the Clearing Price for non-retail is 35.05 which is 40% discount from the Current Market Price. I had placed my bid @ 40.05 and got executed. I could have done better but no regrets - it was a good learning experience for me. Hoping to exploit the arbitrage opportunity in the next few days as CMP is still way above my buy price. If not I will be a long term investor here

Disclosure: Not a SEBI registered advisor. Views are personal and not a buy/sell recommendation. Please do your own due diligence before investing.

In case one would want to ride the commodity cycle?

In case one would want to ride the commodity cycle?