1 Like

This is how the company’s order book has evolved:

| Year | Total order book | New Order | Growth | Metro | Flyover Bridges Road | Civil and others |

|---|---|---|---|---|---|---|

| 2023 | 11,854 | 2,652 | -28% | 47% | 47% | 6% |

| 2022 | 11,936 | 3,685 | 63% | 61% | 31% | 8% |

| 2021 | 10,927 | 2,259 | -47% | 54% | 44% | |

| 2020 | 11,644 | 4,289 | -14% | 54% | 40% | 6% |

| 2019 | 10,372 | 4,970 | 191% | 60% | 30% | 10% |

2022-23

- LOA from lrcon International Ltd for a contract price of ₹ 1,068 crores (excluding GST) for Construction of 8 lane access-controlled Expressway from Bhoj to Morbe Section- SPUR of Vadodara Mumbai Expressway

- LOA from MCGM for a contract price of ₹ 510 crores (excluding GST), JKIL share in the project ₹ 306 crores for Design, Build and Commissioning of Priority Sewer Tunnel - Phase I

- LOA from MCGM for a contract price of ₹ 315 crores (excluding GST) for Reconstruction of Siddharth Municipal General Hospital at Siddharth Nagar, Goregaon (West), Mumbai

- LOA from BMRCL for Bangalore Metro-Phase - 2A & 2B for total contract price of ₹ 237 crores (excluding GST)

- LOA from MCGM for a contract price of ₹ 515 crores (excluding GST), JKIL share in the project ₹ 262 crores

- LOA for Dwarka Expressway-PKG-01 (COS) from NHAI for a contract price of ₹ 464 crores (excluding GST)

(completed projects which included Mumbai Metro Line 7, Mumbai Metro Line 2A, JNPT Flyovers & Road, chheda nagar flyover, SCLR flyover)

2021-22

- Mumbai Metro Line-2B MMRDA Rs. 1,168crs

- Mithi Package IV - Micro Tunnel MCGM Rs. 207crs

- Navi Mumbai Metro Line-1 CIDCO Rs.150 crs

- Cidco Coastal Road PKG02 CIDCO Rs.92crs

- Delhi Metro DC08 DMRC Rs 1,439 crs

- Pune Riverfront PMC Rs 605 crs

- Telli Galli Grade Separator MCGM Rs. 24

2020-21

- project by GMRC worth Rs. 942 crore for design, construction and completion of underground stations and tunnel for Surat Metro

- Rs. 1,052 crore for Sewri-Worli elevated connector by MMRDA

2019-20

- Dwarka expressway- package 2- Delhi- EPC Rs. 1540 cr NHAI

- Mumbai Metro Line-9 (extension of Line -7 from Dahisar to bhayandar and anderi to airport- MMRDA- Rs 1998 cr

- Mumbai Metro elevated 2 stations- MMRDA- Rs 324 cr

- Coastal road, AmraMarg to MHTL junction with airport link at Navi Mumbai- CIDCO- Rs 409 cr

2018-19

- Improvement of Chheda Nagar Junction, Ghatkopar (East) on EEH MMRDA Rs. 223cr

- Construction of Underground shafts for tunneling at Agricultural College and Swargate, Swargate Metro Station & Multi-modal Integration at Swargate Metro Station; and R & R facilities- Pune metro- Rs 222 crs

- Construction of South Delhi Municipal Corporation Head Quarter Near Pragati Maidan at I. P. estate Delhi on Design, engineering, Procurement and Construction (EPC) basis’- NBCC- 559 crs

- DMRC for Line 2A architectural finishing works of four stations – Don Bosco, Shimpoli, Mahavir Nagar and kamraj Nagar- Rs. 28 crs

- DMRC for Line 2A architectural finishing works of four stations – Charkop, Malad, Kasturi park, Bangur Nagar.Rs 28 crs

- UPRNN Ltd for the construction of Emergency Medicine, Clinical and Ward Area in the premises of SGPGI, Raibareli Road, Lucknow UPRNNL Rs. 176 crs

- Maharashtra Metro Rail Corporation Limited (Pune Metro Rail Project) for the Design and Construction of Elevated Viaduct of Pune Metro Rail Project MAHA METRO Rs. 388 cr

DMRC/MU/LINE6/BC/03: Part design and construction of viaduct and 5 elevated stations of metro Corridor (Line-6) of Mumbai Metro Rail Project DMRC Rs. 867 crs - Construction of Dwarka Expressway from Shiv Murti Intersection at Km. 20 of NH – 8 till Rail Under Bridge (RUB) near Dwarka Sector -21, from Km. 0.800 to Km. 5.300 Package – I in the State of Delhi on EPC Mode –Issuance of Letter of Award (LOA). NHAI DELHI Rs. 1349crs

- Design and Construction of elevated road between Mulund Airoli Creek Bridge (Airoli End) and Thane Belapur Road. MMRDA Rs. 275 cr

- Construction of Elevated Viaduct from Vastral Gam to Apparel Park- up to Ramp Start in Reach-1 (East –West Corridor) GMRC Rs. 178 cr

- Construction of Ram Manahor Lohyia Rajya prashikshan evam prabandhan academy. UPRNNL Rs. 47 crs

- Part design and construction of viaduct and 3 elevated stations viz. IIT-Powai, KanjurMarg (W) and Vikrholi Metro Corridor (Line - 6) of Mumbai Metro Rail Project. DMRC Rs. 444 Cts

- For construction of world class skill Centre at village Jonapur, South Delhi Phase- I i.e. Academic block, hospitality block, workshop, hostel block, electric sub-station etc. PWD Rs. 178 crs

Disclosure: Not invested

8 Likes

J Kumar is a gem which is available at v cheap valuations.

Performed consistently over a decade despite all the negative news flow in the last 5-6 years. It is has withstood the trial by fire and has proven itself.

JKIL today stands at the cusp of massive earnings acceleration where as per my projections its PAT will grow 275cr last year to 700cr by FY27.

Management has a stated target of $1Bn revenue at >15% EBITDA without further increase in debt. And they are on track to achieve that.

Current Market cap is just 3200cr.

Prashant Jain (ex- HDFC Mutual Fund head has entered with a 1.42% stake in the last quarter (3P India equity fund)

Sunil Singhania & Porinju are already invested.

J Kumar Infra is right up there in terms of technological prowess for complex engineering projects and is often one of the only 2 or 3 players competing for complex infra projects…its usual competitor is L& T.

2 Likes

Last time I checked…there was too much dependance on Maharashtra region, is it still true?

Their scale & delivery has been good.

What are the triggers for the expected Earning Acceleration, could share your notes please?

My personal view:

I agree as I used to hold this stock earlier. However, there is a difference between being a good business and being a good investment.

They operate is a industry infamous for political connections. This company has also seen income tax raided couple of times.

I will buy it with huge margin of safety (its on my radar). Its currently trading a little over long term average PE. I would look for good correction to add.

I think the story is still the same.

1 Like

PE is definitely on higher side… some funds have entered and raised valuation… not sustainable given nature of business is volatile and politically affected. election is big risk.

2 Likes

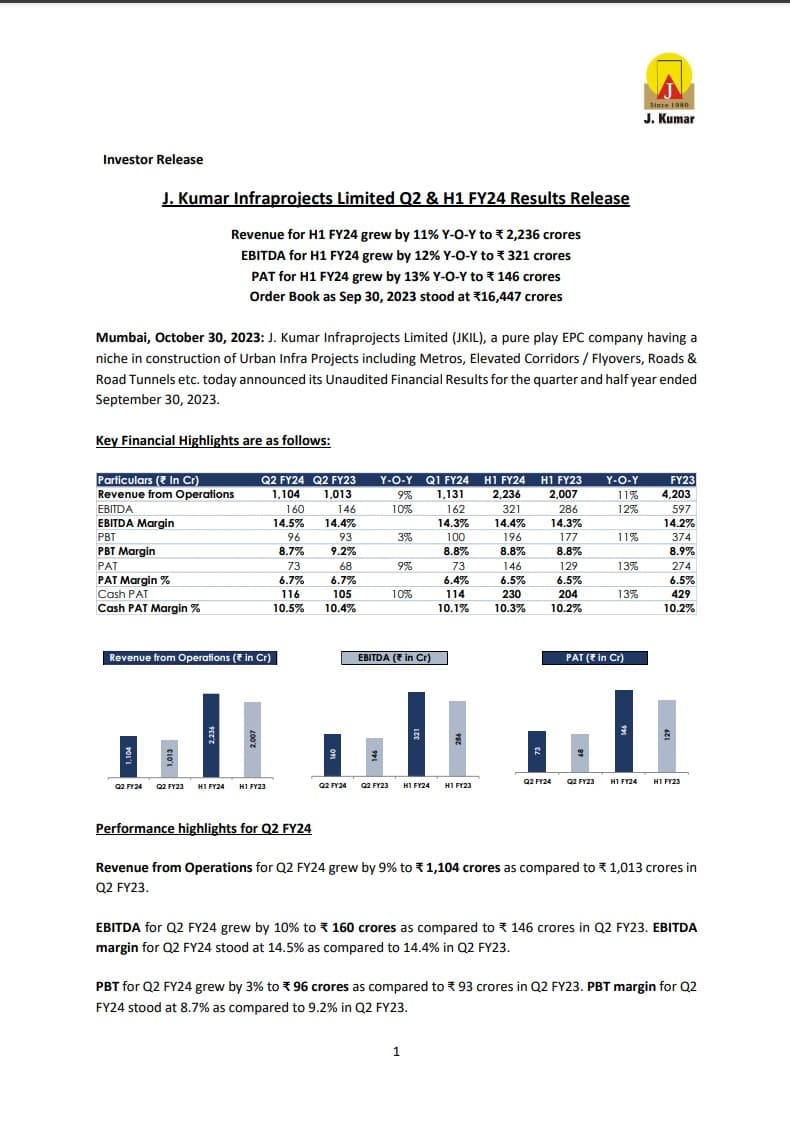

Quarterly Highlights (Q2 FY24):

- Revenue from operations increased by 9% to ₹1,104 crores

- EBITDA increased by 10% to ₹160 crores

- PBT increased by 3% to ₹96 crores

- PAT increased by 9% to ₹73 crores

Half-Year Highlights (H1 FY24):

- Revenue from operations grew by 11% to ₹2,236 crores

- EBITDA increased by 12% to ₹321 crores

- PBT grew by 11% to ₹196 crores

- PAT increased by 13% to ₹146 crores

Other Notable Points:

- Total order book as of September 30, 2023, was ₹16,447 crores.

- Orderbook includes various projects, such as Metro projects, Elevated Corridors/Flyovers, Roads & Road Tunnels projects, and others.

Key Business Updates:

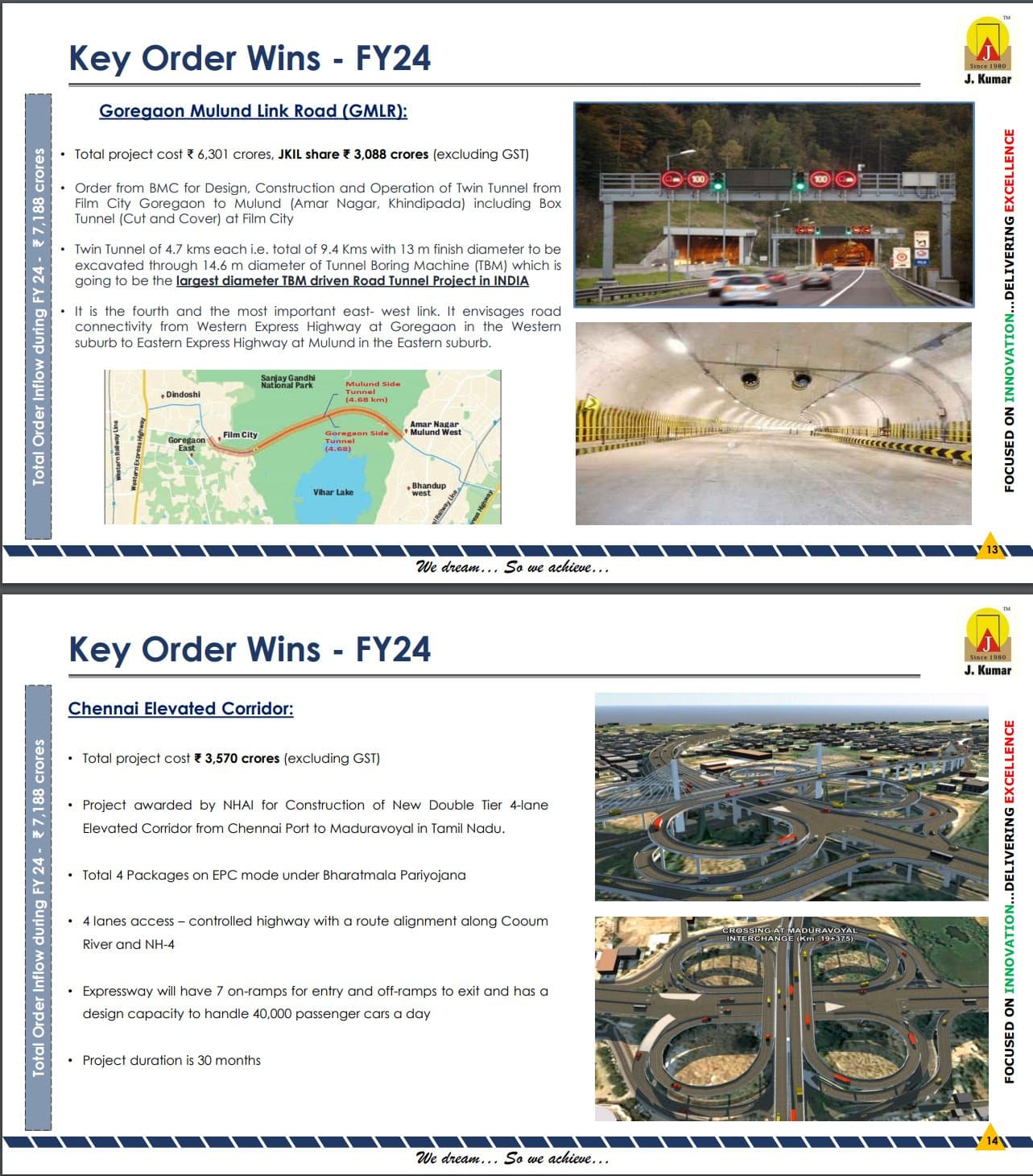

- JKIL was awarded the Goregaon Mulund Link Road project by BMC with a total project cost of ₹6,301 crores.

- They were also awarded the Chennai Elevated Corridor by NHAI with a total project cost of ₹3,570 crores.

4 Likes

Anyone tracking this 14 /15 pe play in urban infrstructure JKIL ? CLSA recentsly initiated coverage on it,

opp size seems good

CONCALL TRANSCRIT NOV 23 JKIL.pdf (1.1 MB)

As per my estimates, based on management guidance of Revenue and Margins, PAT will touch 700cr by FY27 from 275cr in FY23…

Despite all the negative news-flow over the years and sceptical perception which many have towards this company, it has continued to deliver solid, consistent numbers, with 15% YoY growth, over the last 12 yrs…thats why some of the best value investors and fund managers have sizeable stake in it. Porinju once called it the mini L&T 3 years back in one of the conference calls.

I feel current Mcap of ~4500cr should reach 10,500cr in couple of years (March 26) at which point the company will trade at 15 times forward (March 27) PAT of 700cr.

3 Likes

https://www.screener.in/company/JKIL/

Agree. Some marquee names like Sunil Singhania Abbakus , Prashant Jain ex HDFC MF 3P Capital, HDFC MF with big 9% stake , Mukul Agarwal invested in it.

Double engine govt focussed like laser on infrastructure projects specially urban infra projects.

CLSA report is quite detailed one.

1 Like

the company has had issues with corporate governance/ negative news in the past.

these big names usually exit fast leaving retail investors high and dry… HDFC has been invested for many years - risk of selling is there…

pl have a look at the chart - huge volatility…

1 Like

14 PE Good roce orders n opp size Jkil. can PE n Eps expand in 2024?

1 Like

Contigent liability of 2496cr, can anyone tell the reason?Still why big investors are attracted to this stock?

All infra companies are overvalued. they are taking too many projects and any delay will hit them hard. this is a repeat of what happened as few years back.

1 Like

Still a lot of value left in this stock. Expect a PAT of 700cr in FY-27 from ~330cr in FY24. Great earnings acceleration ahead.

1 Like

Infra companies are not like manufacturing companies - sales and profits can both increase and decrease by a huge %. hence the low PE. these companies at such high PEs are a risky bet…

1 Like

JKIL still remains one of the few deep value plays on the India story over the next 2 decades.

PAT will more than double in three years - from 330cr in FY24 to 700cr in FY27.

Conservatively, at 15x 1-yr forward earnings, the stock can easily trade at 10,500cr by FY26-end (Current Mcap 4600cr).

That is, more than double in less than 2 yrs.

Some of best value investors are holding this stock.

3 Likes

EPC companies usually have a forward PE of max 10. there are many variabilities - cost escalations, delays, litigation, etc. In case of J Kumar coporate governance also has been an issue on a number of occasions in the past.

3 Likes

1 more IT raid (check precedence) and all this optimism will be down the drain. Stock is trading at very high valuations because of general euphoria and excess liquidity in the market.

Please note they are working in a very competitive industry where orders are earned based on bidding, which directly impact the margin.

“India story” has been playing since 2 decades. Every analyst use the same 2 words. Then why are QSRs doing so bad? Even they are riding on “India story”.

Be cautious when your horizon is 2 decades. Its a long long long period.

Disc: Former shareholder, tracking for better entry opportunity to take trading position.

2 Likes

agree…

due to entry of few “reputed” investors has helped the stock shoot up… this is the story over and over again in the market. JKIL had shot up to 400 in Aug 2015 and then down to 100 levels in Jan 2020 (pre-covid). again it is time to correct… be careful.