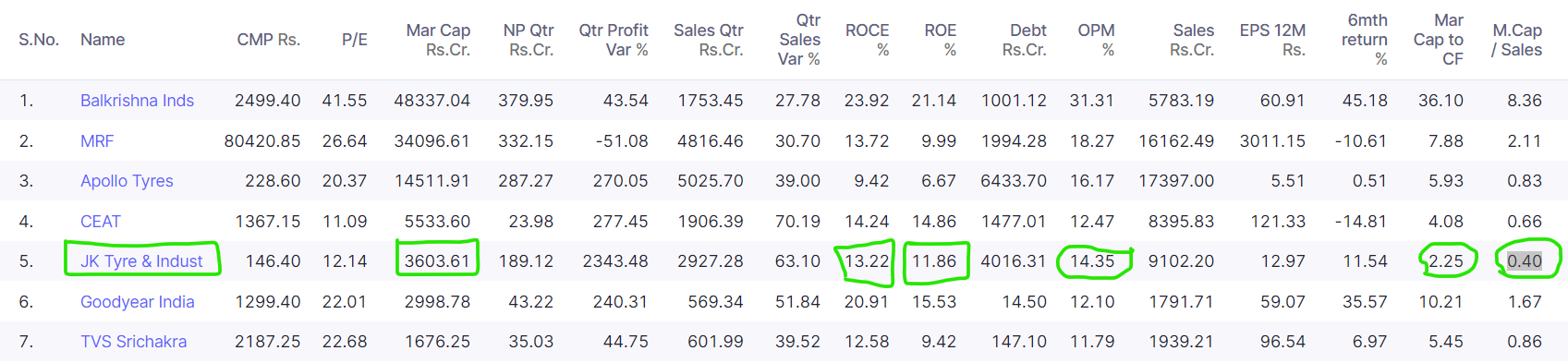

Why -

- JK Tyre is cheapest tyre stock on the multiple of cash flow for FY21. Market cap is at 2.25x cash flow.

- Company has repaid Rs. 929 Crores debt only in FY21 which is about 25% of the market cap.

- Company’s focus on ESG elements

Business -

The Company is engaged in the manufacture and marketing of automotive tyres, tubes and flaps. The

Company’s tyre products comprise Truck/Bus Radial & Bias, Passenger car radials, 2/3-wheeler tyres, LCV & SCV, Bias & Radial, Off-Highway Tyres (OTR and Farm) as well as speciality tyres for Racing, Military/Defence, Industrial and Farm applications.

JK Tyre’s manufacturing operations comprise 12 state-of-the-art manufacturing facilities. The Company

manufactures products out of nine modern plants in India (three plants in Mysuru, three plants in Laksar and one plant each in Banmore, Kankroli and Chennai) and three plants in Mexico

– an aggregate production capacity of ~32 million tyres per annum.(MRF at MRF @ 57 million tyres per annum with 80,000 market cap just to put things in perspectives)

Financial -

- Market Cap - Rs. 3,600 Cr.

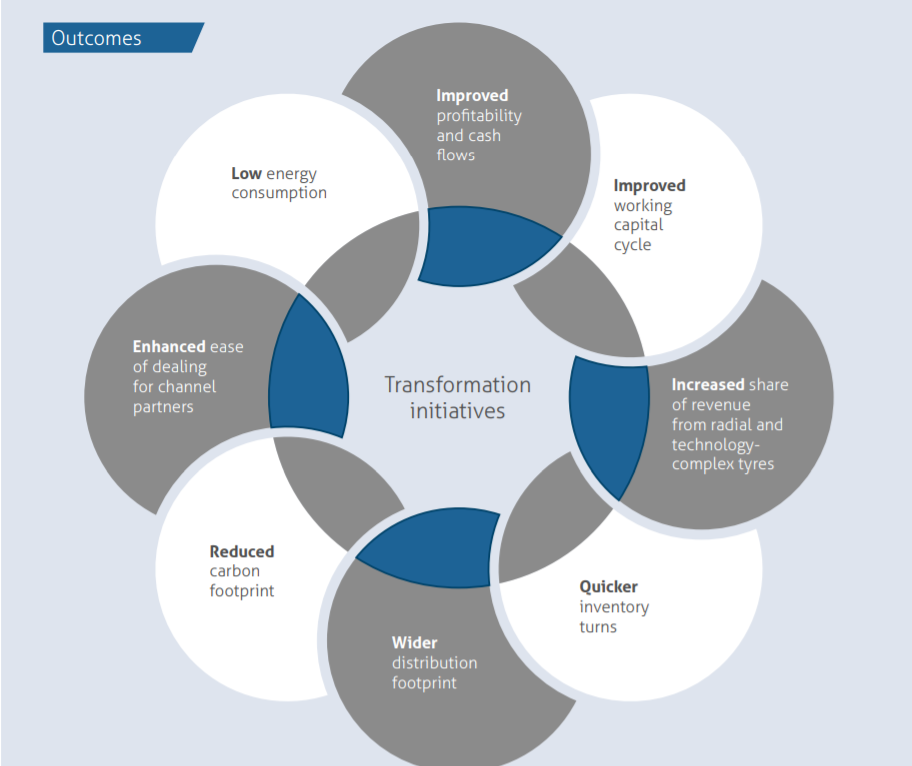

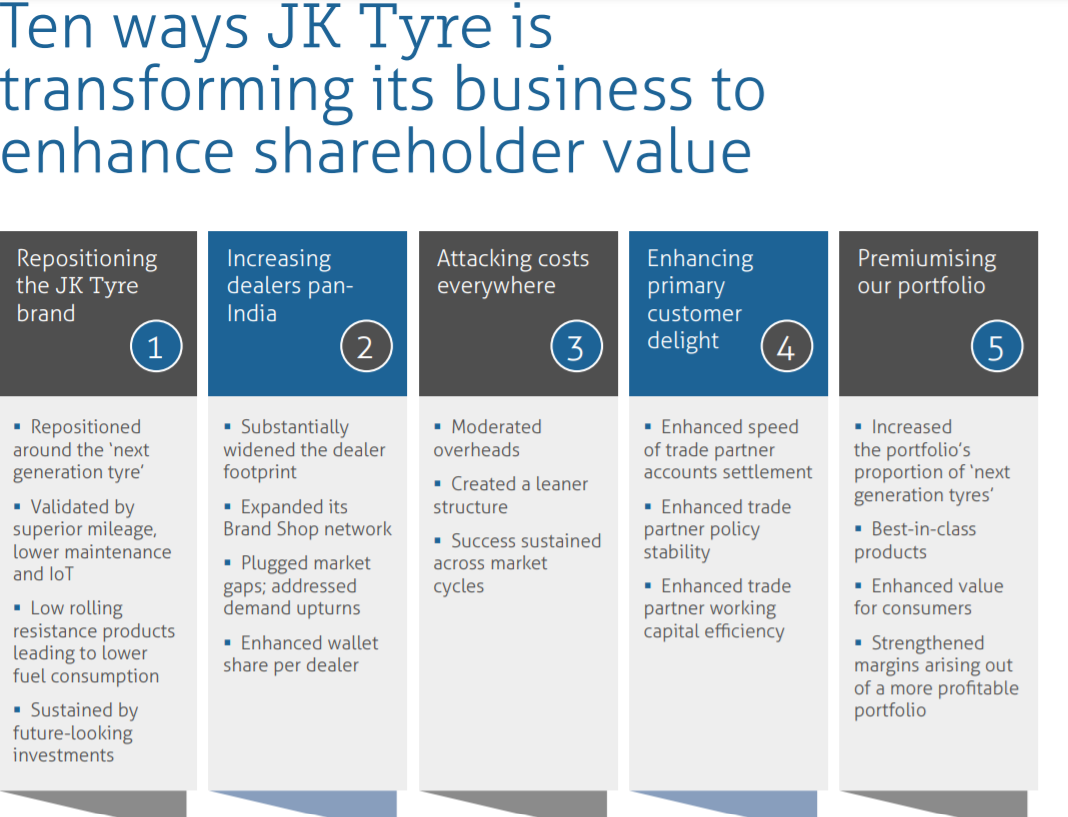

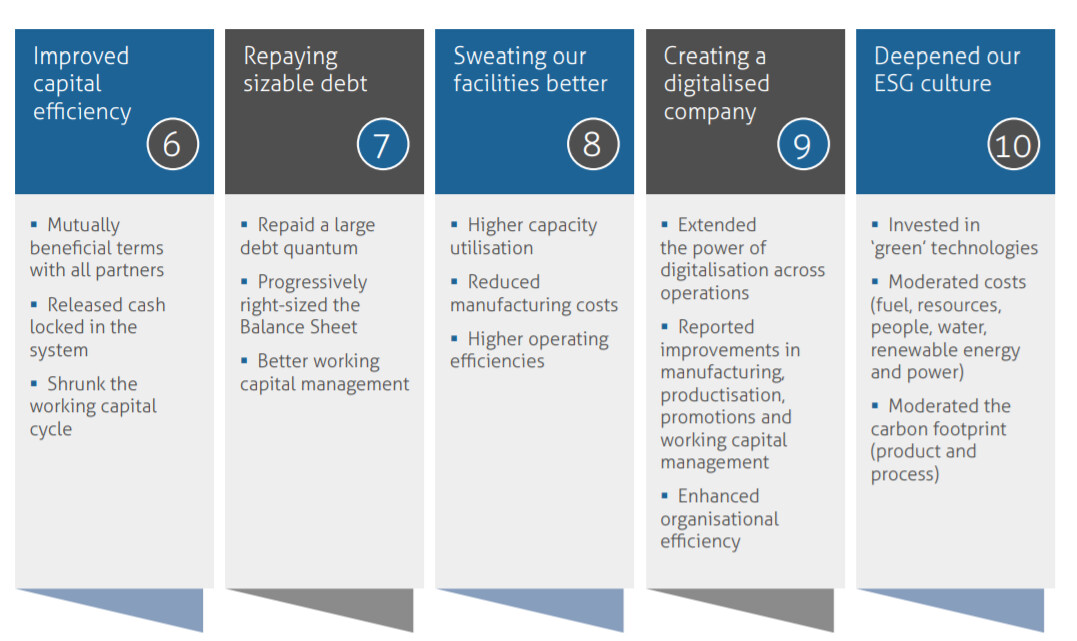

Outcome from transformation initiatives -

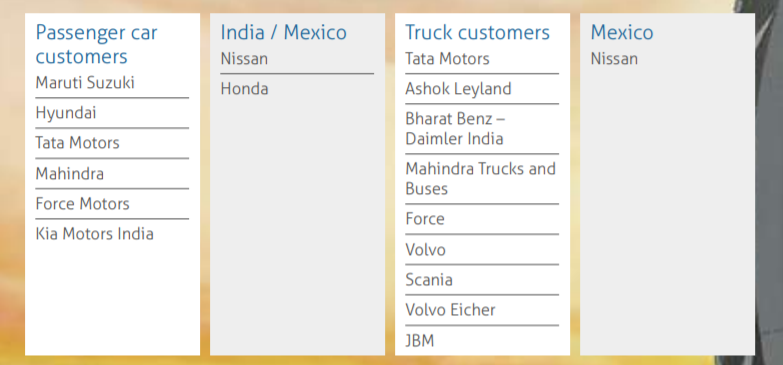

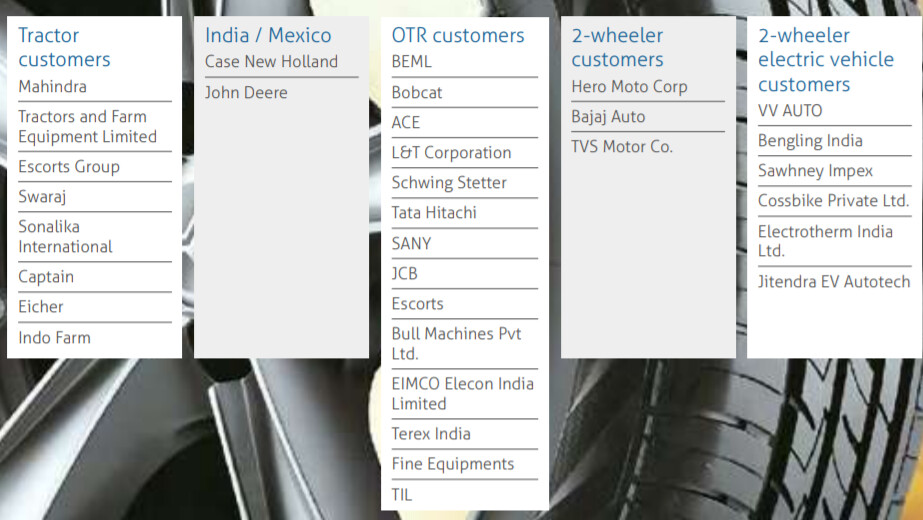

Customers

ESG Messages from AR2021

-

JK Tyres is the global benchmark for the lowest raw water use per kg of tyre produced. In fact, we are one of the lowest three in the world on energy consumption in the tyre industry.

-

The use of renewables in our power mix increased to 55% during FY 2020-21, increasing annually. These efforts helped us in reducing carbon emissions intensity by 53% in the past few years.

-

Moreover, JK Tyre is now certified to be as ‘Zero Waste to Landfill’ as well as ‘Single Use Plastic Free’

Business Performance - 2021

-

Robust cash accruals, coupled with close working capital management, led to a significant reduction in debt.

-

The capacity utilisation across all our plants exceeded 90% during the second half of the FY21.

-

Various measures were initiated to enhance capabilities in our manufacturing facilities, including

IOT for complete traceability. -

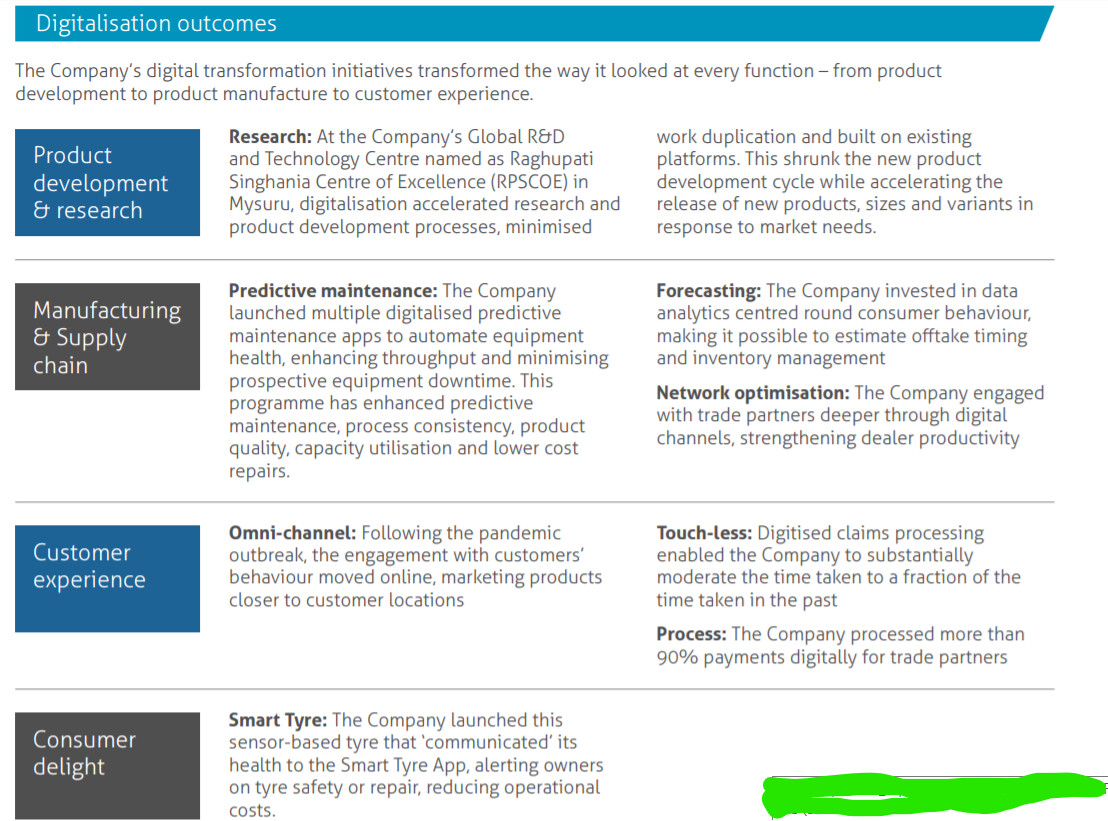

Digitalised customer solutions played an important role in sustaining and improving customer service levels despite the restricted operations. The digital claims process, based on AI and Machine Learning,implemented in the year under review addressed 95% of the warranty claims, majorly in nontruck tyre categories. We were able to achieve a benchmark turnaround time for claims settlement to as low as 30 minutes

-

Our marketing communication was also transformed by leveraging various social media platforms,

leading to industry-best levels of viewership -

Enhanced employee engagement yielded fruitful results and JK Tyre was recognised as a ‘Great Place to Work.’

Transformation Strategy

Digitalization Focus

Outlook on Digitalization

The Company’s mid-to-long term digitisation plan is to become digital-first, deepening digitalisation through robotic process automation, advanced analytics, machine learning and leveraging artificial intelligence. The Company intends to implement or recalibrate processes that maximise human and digital capabilities leading to positive outcomes in terms of revenue growth, optimised costs and superior customer experience.

Aggressive Debt Reduction

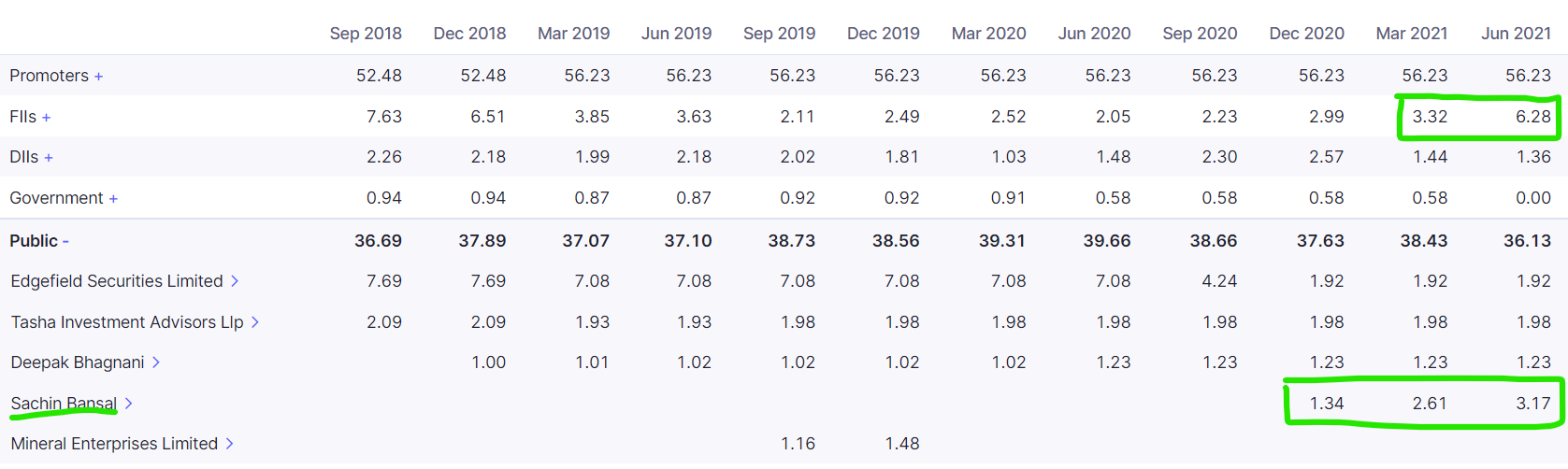

Noticeable Share Holders

Key Business Risks

- Uncertain economic Scenario:

- Impact of Pandemic on Business:

- Raw Material Availability

- Technology Risk

- Supply Risk / Capacity Risk

References - 2021-AR & Screener

Disc - Invested at 2% of the portfolio