The hikes in the price of paper products and the recovery in demand could help the company maintain industry-beating margins forward.

As per industry sources, paper prices have started to decline. Do you have any concrete information that paper prices are still going up?

PAper prices are indeed declining. First went the Kraft paper. Then the White back and Grey Back. FBB is still holding on, but it seems it will follow suit sooner or later. Import have started coming in as the freight rates are down.

In April :

1 Like

Sir, the article and development is from April 2022 and I believe the impact of it is already in the market. Despite this the Q1 & Q2 results of most of the paper companies have been very good.

However, the CFO of JK paper did mention in a recent interview that there is some pricing pressure in newsprint & packaging board while the writing paper is still trading strong.

Regards,

Yogansh Jeswani

Disclosure: Invested

1 Like

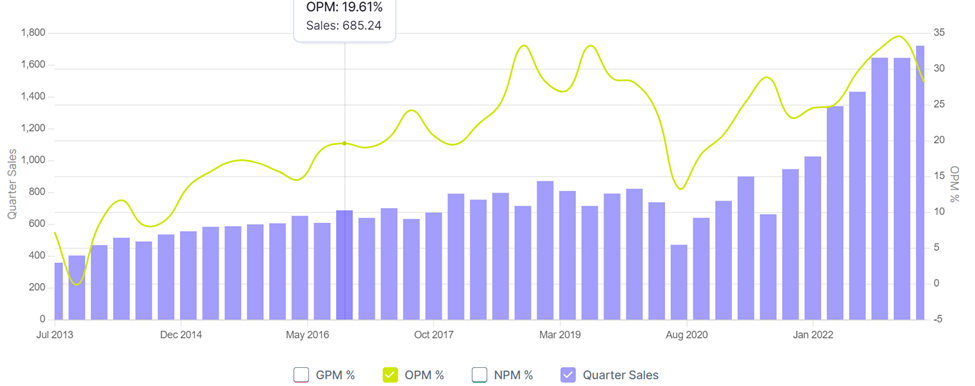

Of recently markets have been discounting good results posted by many commodity companies. Paper industry was no exception. And as @anjeshv4 has said commodity stocks prices peak before peak earnings. If you look at OPM for JK Paper they were @ 33% which is close to peak margins posted in 2019. In addition to the high margins, most of the capacity is optimally utilized as well. So we may be close to peak revenue as well as margins. So can the current margins and revenue be sustained?

Major Indian integrated paper companies benefitted from the very high pulp prices. JK Paper buying almost all the wood that it require from its own adjoining plantations through contract farming. At a time when most commodity companies are hit severely due to raw material costs, Indian integrated players are at a sweet spot due to their farming operations. Utilization levels of JK paper was always very high close to 100 % even in bad cycles. It was the usually the landed cost of imported paper that played the spoilsport for Indian Paper companies. With high freight rates and high pulp prices the landed price of imported paper is stay high atleast in the short period. China banning import of waste paper had a severe impact on paper pulp prices, which doesn’t seem to be going down any sooner.

Infact pulp prices are continuously going up.

Eventhough all its capacities are optimally utilized now, the corrugated paper capacity may come up in a couple of quarters. There is a CWIP of 115 crores in balance sheet as of Sept 22.

So even if prices for different paper are getting soft as per news, I dont see prices going down sharply due to the high pulp prices. So margins may stay high.

Also company had an EBITDA of 500 crores, and Market cap/ EBITDA of 3.6 on an annualised basis. The company’s high debt of 2900 crores may have been an overhang on the stock price. With much improved cash flow and repayment in debt could lead to better market cap eventhough enterprise value remains the same.

Discl: No investments. exited way too early

9 Likes

I’m curious to know what is happening in EU paper industry as power costs have gone over the roof, what could be it’s direct & indirect impact on Indian paper industry?

OPM margins were down to 28 % from 34 % on a QoQ basis. Share prices have dropped from a peak of Rs .447/- on August 22 to 366 as of yesterday ie, 17.05.23. So far it is perfectly following the usual cyclical understanding that price peaks before the peak margins and signaling the end of a cycle.

The landed cost of imported paper is usually the largest dampener to the paper industry in India. As discussed, there are two things that affect the cost of imported paper. 1) Pulp price. 2) Cost of transport or shipping costs 3) Import duty.

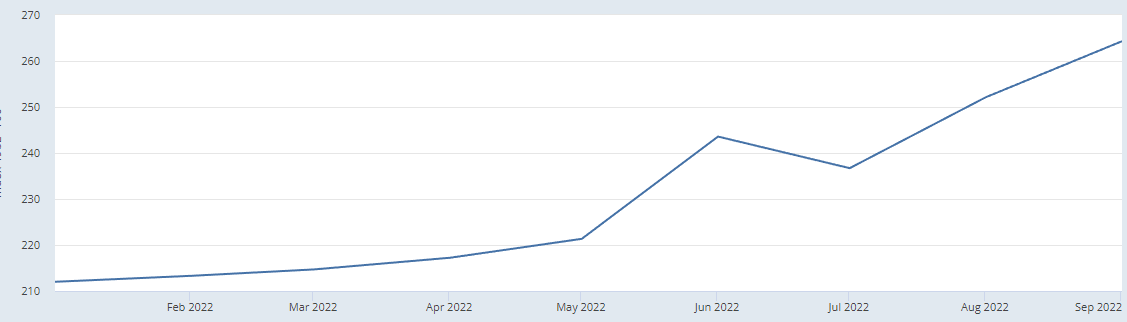

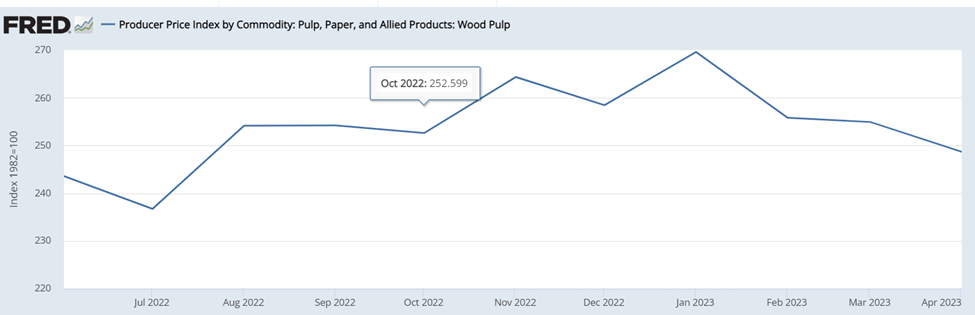

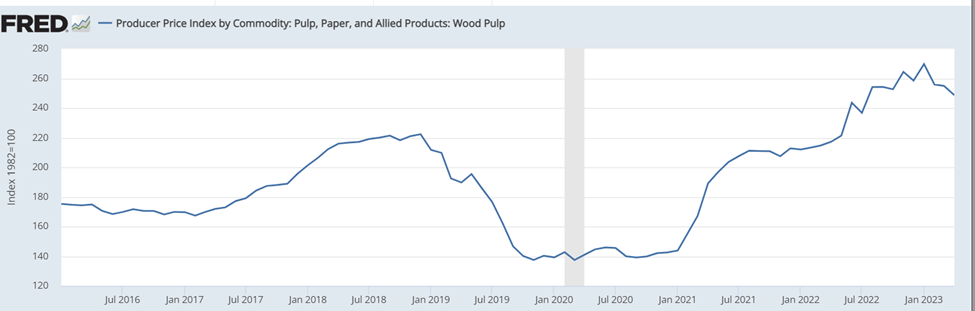

Pulp price is indicated by pulp price index

The pulp price index has come down to 248 as of April 23 from a peak of 269 on January’23. So, considering the pulp price index alone margins may come down further in the Q124.

However, it’s still far better than the peak we saw in 2018.

The company in its earnings release indicated that the selling price of some products has reduced in Q423. It also mentioned some other costs are reduced (No idea what it is)

Shipping costs

Shipping costs have fallen drastically over the past 1 year which makes import more competent. However, it may aid the company with more export opportunities. As per India Ratings, JKPL increased its export volumes 7% yoy in FY22 (constituting 12% of sale volumes), with increased opportunities in overseas markets amid global supply disruptions and rising pulp/wastepaper prices.

New Capex and acquisition of corrugated box manufacturers

JKPL acquired two corrugated boxes manufacturing companies Horizon Packs Private Limited (HPPL) and Securipax Packaging Private Limited (SPPL) in December 2022 that are leading players across seven locations in North, West and South India. Also, it has started trial-runs at its greenfield corrugated boxes plant in Ludhiana (in subsidiary JKPL Packaging Products Ltd) which is likely to be commercialised in March 2023. JKPL’s overall volume are likely to witness strong growth in FY24 as well, as additional volumes come from the entry into corrugated boxes along with higher packaging volumes.

JKPL acquired HPPL and SPPL in December 2022 for a consideration of INR5.8 billion, funded by internal accruals. Apart from this, the company is setting up a corrugated boxes capacity in Ludhiana, Punjab, for which it has already incurred about INR1.4 billion and could incur another INR0.3 billion in FY23. Other than this, no major expansionary capex is planned as per the management.

Source: India ratings Jan’23.

As per the earnings release, the company mentioned only that the operation of corrugated box manufacturing is satisfactory. No mention of any capacity utilization.

Increasing FII shareholding.

Source: Screener

It is interesting to note that FIIs have been continuously increasing their shareholding for the past 3 quarters.

Debt Repayment

The consolidated debt came down from 3079 crores to 2803 crores. Interest on a QoQ basis has come down to 63 crores from 94 crores. Adding depreciation to net profit = 365 crores. The company does have the cash flow to reduce the debt significantly. The company hinted at accelerated debt repayment in August’ 22 con call. But went on to acquire 2 corrugated box manufacturers for 586 crores. With this acquisition, the company is however able to further diversify its products.

The company’s OPM margins since 2016 haven’t fallen below 19 % even at the bottom of the cycle except for 2020.

Margins may further dip in the next quarter, but I expect the company to have good cash flows to pay down the debt. FIIs increasing the stake in the company is interesting.

Discl: Not invested. Just trying to learn about the company.

10 Likes

While its difficult to project the margins in such cases, but I think it will be fair to assume that it will not go below 22-23%. Also, the net debt should be close to 2200 Cr. Also, in yesterday’s interview they have maintained the topline target of 7000Cr+ for FY 24. In the interview they have mentioned that the capacity utilisation of acquired corrugated boxes is ~60% and they will target to improve till 70% (which is considered as peak).

Also, your observation of more institutional holding is making the shareholding into stronger hands - which should be considered as positive. I also liked that the company increased dividend to 8 Rs.

Anyways, while near term triggers are missing this company size and its efficiency and diversification in terms of the plant location and product offerings will make it a strong leader.

2 Likes

Links to some interview for Q4 FY 23

Paper mills are closing at an alarming pace due to demand reduction.

https://indianexpress.com/article/cities/ahmedabad/20-paper-mills-shut-in-six-months-association-seeks-govt-support-8669974/

We may still not be at the cycle lows yet. Management indicated lower margins next year with no growth capex, near triggers are definitely not there. I plan to shortlist this company and wait for the cyclical low and some inventory improvements

1 Like

company is available at an attractive valuation, accompanied by a lot of other paper companies. Any learned folks out here who could help me understand the larger trends in this industry?

1 Like

Broadly the global pulp cycle has come down significantly from 900$/tonne to now 500$/tonne. Industry believes that this is the bottom. However, as per recent interview the uncoated paper can still see a bit pressure for next 1-2 quarters.

Even if that to be considered and if you consider 23% as average margin (last year everyone knows it was an exceptional year). The company would generate sizable cash flow and available at very cheap valuation. Also, if you see currently it has delivered good number which honestly was a surprise as 30% was not an expected margin for this quarter.

Attaching link here of 2 interviews for your reference.

Discl: Invested

6 Likes

3 Likes

3 Likes

JK Paper’s results -

Good results given the management commentary about softer industry conditions…

1 Like

Long term debt reduced by around 200 odd crores in the HY. Interest outgo has reduced proportionally. Crisil ratings is a good read about the capex and assets.

The company is expected to undertake yearly maintenance capex of Rs. 100-150 crore and a partially debt funded capex of Rs. ~650 crore during FY 24-26 to set up a BCTMP pulp mill, which will help in backward integration and will substitute imported pulp at Unit CPM. Despite the said capex and acquisition of Manipal Utility Packaging Solutions Pvt Ltd for a consideration of Rs. ~90 crore, expected to be funded out of cash accrual.

The company’s liquidity position remains strong, characterized by healthy unencumbered cash and bank balances of Rs. 1225 Cr (Rs. 900 Cr in Mutual Fund and Rs. 325 Cr in Bonds) as on September 2023 and average unutilized fund based limits of around Rs 163 crores (~65% of total limits of Rs 250 crores).

source: crisil ratings

3 Likes

Stock increased more than 6% today with high volumes, likely because of price hike.

While looking at the 2022-23 annual results, company has crossed 100% capacity utilisation.

CWIP at the end of H1-2023-24 is only Rs.97 crores. CWIP of Rs.97 crores can only be de-bottle necking. Company has not announced any plans for major capacity increase.

acquisitions may help, and they may do it for inorganic growth…

In paper industry case, the capex are large and hence they dont come every year. Still they have announced one plant in ludhiana which is happening now and one pulp mill that will come into place after FY 25. Also, they have acquired one company in mono layer packaging recently for about 90 Crores. Some or the other thing is going on. Also, the capacity utilisation is pending in the 2 companies that they acquired (Horizon and Securipax)

3 Likes