While it is difficult to predict what could happen on the demand side in the near term,on the supply side while Indian rupee depreciated about 6% against USD in the last 3 months,Indonesian Rupiah depreciated about 16%.This makes imports even cheaper than they already are.It will reduce revenues and margins of Indian paper manufacturers unless the govt puts up any tariff or non-tariff barriers.

Tariff barrier already exists since January 2019 for uncoated paper. You can run through this thread the details are there above.

Hi,

As per BSE buyback record JK Paper has till date bought back about 14.6 lac shares combined on both exchanges.

Assuming average buyback price of around 90 rs. because share price has remained in range of 85 to 100 in last month , implies that company has spent around 13 Crs for shares already bought back . And offer is open until November.

So they seem to be on track, and your concerns may be unfounded. Hope this helps.

Hi,

Thank you for pointing out the correct data.

I was under the impression that the company needs to file with the exchanges under the corporate announcement section every time they buy the share in the buy-back window.

I didn’t knew this page (https://www.bseindia.com/markets/publicIssues/CummShares.aspx?ID=532162&scripNm=JK%20PAPER&buyback_dt=11/06/2020&enddt=08May2020)

on the bse website which provides this data.

Thank you again, since the data was incorrect the whole premise of my hypothesis was invalidated. hence, retracting the post.

Sharing excerpts from Suzano Q1 2020 earnings transcript - full text here.

Increasing pulp prices are positive for integrated Indian producers such as JK and Seshasayee.

Pulp: strong demand globally, falling inventory levels in Asia & European ports and $30/ton price increase

This combination of lingering supply constraints and solid demand across all the key markets have supported our price initiatives. We announced it for April in Asia $30 more, and all the business concluded fully capture the $30 that we announced. We also announced a $30 list price increase for Europe and North America, and we believe the conditions are in place to support full implementation.

Paper: 12-15% drop in writing & printing paper demand; halting production for 2 months totaling 50,000 tons

Now coming back to sales. We foresee a very challenging scenario concerning the demand of printing and writing papers in many regions of the world and also in Brazil due to the COVID-19 pandemic and consequences of the lockdowns and quarantines. In Brazil, the first effects were felt on the week of March 23. Consumption dropped significantly across all printing and writing grades even further than the 12% decline accrued by our pulp and paper association, Iba, for January and February. Printing and writing demand fell 23% in March, with Brazilian domestic sales dropping 22% and the imports 24%. The resulting compounding statistics were 15% drop in the Brazilian demand for printing and writing papers in the first Q 2020.

Now, our expectation is that the demand will see further declines during the second quarter, even below March levels. As a consequence of this drastic decline in consumption, our stocks have risen significantly and we have decided to stop paper production at our Mucuri and Rio Verde mills during the months of May and June, totaling approximately 50,000 tons paper production curtailment which will enable us to match production with market demand. Our operational flexibility will allow us to redirect the resulting pulp from the stoppages to other markets and products. Despite this commercial downtime, we do not foresee any interruptions on the paper supply to our customers in Brazil or internationally as our stocks are fulfilled and our four paper machines at the Suzano and Limeira mills allow us to have production flexibility between paper grades in these sites.

Recently started tracking this company, can anyone guide me as to where I can find management guidance like concalls as I couldn’t seem to find it at the usual websites.

You may refer to the latest transcript of analyst meet the company did. It’s posted on JK Paper website under Investor section.

I did, their latest transcript was in 2018.

Here you go:

Management believes that prices/realizations continue to be weak on account of global pulp prices and weak demand overall.

Operations have resumed at their Sirpur plant.

was looking at paper industry and I was interested in JK paper being one of the leaders.

Raw material cost

Raw material cost as percentage of revenue has come down from 41 % in 2010 -11 to 37% in 2019-20. In the business of paper manufacturing that relies extensively on the procurement of wood resource, there is a premium on the ability to procure the largest volume at the most affordable cost within the shortest procurement distance.

Energy: The energy intensity (total energy consumed per ton of product) was 971 Kwh/ MT in FY 2018-19 and 959 in FY 2019-20.

Raw material: The material intensity (wood consumed per ton of product) of the Company was 1.60 ADMT/MT in FY 2018-19 and 1.59 ADMT/MT in FY 2019-20.

Water: Water consumption per ton of product has reduced from 38.85/ MT in FY 2018-19 to 34.74 M3/MT in FY 2019-20.

The Company has moderated the average distance covered in the procurement of wood resource , reducing time and distance taken on the one hand and the average cost of procurement on the other. The Company has enhanced the coverage of plantation wood in its hinterland by planting ~50,000 hectares in the last four years. The Company commenced operations in SPM in 2019-20, capitalising on the abundant availability of wood in Telangana and Andhra Pradesh, proximate to its manufacturing facility. The Company focused on local sourcing from six prime districts, namely Rayagada, Koraput, Vishakhapatnam, Nabrangpur, Vizianagaram and Srikakulam reducing its procurement and logistics costs.

In addition to reduction in raw material costs, I think this has a major advantage to the company in managing its working capital. Company has a debtor days of 10.5, whereas it has payable days of 66.2. Similarly the company’s o/s receivables are 79.1 crores whereas payables are 397 crores.

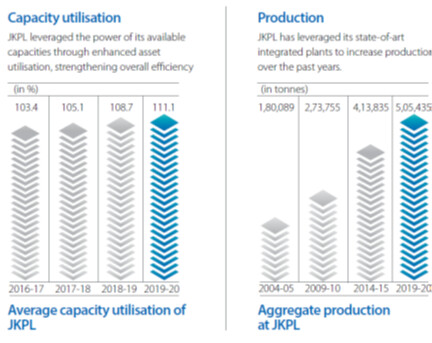

Capacity Utilization

The Company delivered an aggregate asset utilization of 111.1% during the year 19-20 , a 240 bps increase over the previous financial year. Besides, the Company’s manufacturing excellence has been reflected in a strengthening input output ratio (superior yield), enhancing overall competitiveness.

Company has been able to bring its utilization levels to above 100% in Q4’21 at both the plants at JKPM( Rayagada, Odisha) and CPM(Songadh, Gujarat). Company has shown exceptional utilization. The Sirpur plant has also become operational in Q4 and has posted a profit.

Capacity and products

JKPM( Rayagada, Odisha)

The plant (5 machines) comprising 2,95,000 TPA of manufacturing capacity, among the largest paper

manufacturing facilities in the country.

CPM(Songadh, Gujarat)

The plant (3 machines) specialized in the manufacture of paper and packaging boards. Capacity -160000 TPA

The Company announced its 1.7 lac TPA paper board expansion project at Unit CPM for about H1,900 crores (net of GST); capital cost per tonne was around 15,000 lower than the prevailing benchmarks on account of the Company’s decision to repurpose an existing pulp mill and use existing infrastructure, strengthening business sustainability

Sirpur( Kagaznagar, Telengana)

Capacity -136000 TPA.

The plant possesses a longstanding experience in manufacturing colored paper, generating superior realizations. The plant’s four stateof- the-art machines manufacture paper ranging from 44 to 400 GSM. The plant re-commenced partial production and reached a capacity utilisation of ~65% in March 2020.

Products

Office and copier paper

The Company boasts of a diversified portfolio of office and copier paper across the value chain, covering the economic to premium segments. These varieties find growing downstream application in printers, fax machines and photocopiers.

- Manufactured 2,13,486 tonnes of copier and office paper

- Exported 34,259 tonnes copier and office paper

The anti dumping was levied on copier paper and that was in 2018 which is still continuing.

Packaging board

The Company produces packaging board at its Unit CPM in Gujarat,

- Sold over 95,399 tonnes (Including exports) of packaging boards in the year 2019-20

- Exported 412 tonnes of packaging board.

Coated paper

Coated paper is a niche sector in India with 67% demand addressed by global players. JK Paper is one of only two Indian companies manufacturing coated paper(there may be more, line is from AR’20). The Company leverages its ability to provide customised products. Depending on international prices, the Company imports coated paper that find application in magazines, books, brochures, posters and wedding cards, among others

- Sold 49,086 tonnes of coated paper

Maplitho & speciality papers

- Sold 93626 tonnes of maplitho and speciality paper

- Launched JK Ecosip, JK Sublime, JK Oleoff, JK Digi Roll, JK Pharma Print, JK Devine,JK Cup Stock, colour printing and photocopy paper and anti fungal boards (for soap wrapping)

PROJECT EXPANSION

- The Company commenced Virgin Fibre Boards (VFB) production in the financial year 2007-08 with an initial capacity of 60,000 TPA at its Unit CPM which was enhanced to 90,000 TPA in the financial year 2013-14. The current production from this facility exceeds 100,000 TPA. This segment has grown at 12% CAGR during the last 5 years and is expected to maintain its growth at double digit rates in the coming years due to changes in organised retail and the quest for more eco-friendly, aesthetic and customer friendly packaging. Looking at this growing demand particularly in the high end VFB and to build its market share, the Company had decided to set up a new Packaging Board facility along with an integrated chemical pulp mill at Unit CPM. Orders for critical equipments and some other areas were placed and civil construction started in November 2019. The estimated capital cost is about Rs.1935 crores (net of GST). Once completed the capacity for VFB will increase to 270,000 TPA along with a pulping capacity of 160,000 TPA. The new project is likely to take 24 months from zero date to commence production. Post completion of this project the JK Paper will be the second largest producer of VFB in the country with the capacity of 270,000 TPA along with a pulping capacity of 160,000 TPA.

- The new project, which is being undertaken at Gujarat plant is a new machine for packaging board only. this plant becomes fully integrated. They don’t have to depend on the market pulp, but these will be, efficient, power and utilities. All put together, this project is Rs. 1950 crore.

- The project was expected to be completed by Q4’21, however the project got delayed due to covid crisis. Currently the company expects to commence production by Q2’22. However, it will take about 12 months as per the company to stabilize operations and start optimum productions. So we may not see any major contribution in revenue from the new capacity addition.

- CWIP is currently 1702 crores. The consolidated borrowings is Rs.2540 crores. This is expected to be close to peak levels.

PROGRESS AT THE SIRPUR PAPER MILLS LTD.

During the financial year 2018-19, the Company alongwith its subsidiary had acquired The Sirpur Paper Mills Ltd. (SPML) under the Insolvency and Bankruptcy Code (IBC/Code). The Company was one of the earliest successful applicant under the then newly enacted Code. The Resolution Plan of the Company was approved by the Hon’ble National Company Law Tribunal (NCLT), Hyderabad Bench on 19th July 2018. The Company after settling the debts of the financial and operating creditors as ordered by the NCLT, took over SPML and started revival activities w.e.f. 1st August 2018.The acquisition was expected to provide synergies of a strategically located 3rd site near to sources of raw material with closer access to Coal and plenty of water. SPML commenced its commercial production on 24th May 2019 on Machine 7 alongwith Boilers and Turbines. After some challenges in stabilising operations all the machines (including Machines 3, 8, and 6 alongwith all allied equipment) commenced commercial production on 1st March 2020 after due refurbishment. There was an additional investment of Rs.210 crores compared to earlier estimates.

Before the COVID-19 lockdown, SPML had ramped up its production and achieved highest production of 286 tons from the Pulp Mill (against a rated capacity of 323 tpd) and 320 tons (rated capacity of 400 tpd) from the Paper Machines. In the month of March, 2020 (up to 21st March, before COVID-19 lockdown) the Company achieved about 70% of the capacity based on actual number of working days. Progress is also being made on improving the quality parameters of the final products to meet customer requirements and expectations

Ultimately capital cost will come in the range of Rs 550-600cr, for refurbishing and putting up the new Power plant, but, this is over and above what we have paid the banks in the erstwhile company.

When the Mill do not operate fully, the whole lot of incentive which were committed by the government we do not get because those incentives are linked to the procurement, production and other things. So once they start operating at a 70%, 80% of capacity then the incentive also and the cost structure also changes dramatically.

Cyclicality of paper industry and investment thesis

So far I have covered a bit on why I have selected JK paper as an investment from the paper industry. Industry is highly exposed to cyclicality. The industry’s prospect rely a lot on wood pulp prices. The Indian industry is mostly having integrated pulp production. So a fall in international wood pulp prices will open up Indian market to cheaper imports. Copier paper already has an anti -dumping since 2018. Even then imports are feasible when pulp prices fall.

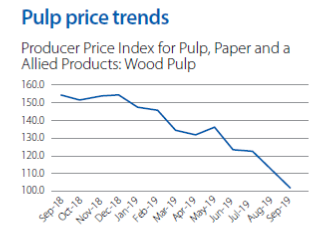

The price of coated paper is largely governed by the movement of global pulp prices and the landed cost of imported coated paper. In the second half of 2019-20, pulp prices went down and there was an improvement only in the last quarter in realisations. declining pulp prices result in lower landed prices that affected the profitability of companies like JK Paper.

AR’20 had a brief reference to pulp price index with a graph

It indicates that PPI is on a continuous fall from Sept’18 to sept’19.

.

This made me look into how the Purchase power index for wood pulp looks like.

It is seen that the PPI has started to move up from Jan’21 and is still moving up in April. Values in AR and this graph is differing may be because of different base years.

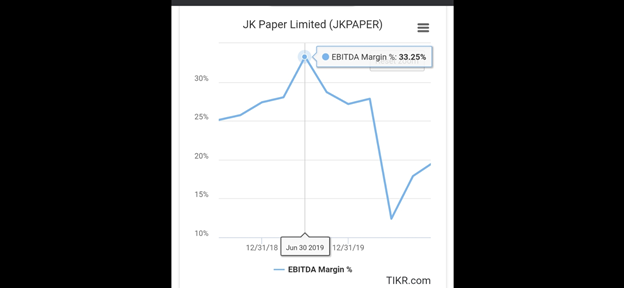

Company’s EBITDA margin history

Company’s margin is seen peaking at 33% in 2019 when pulp purchasing power index peaked. It would have been a great Q1’22 had the domestic demand not severely affected by second wave of covid 19. Company’s export has largely remained very low over the years, however there were details of exports done in 17-18 where it mentioned in an investor presentation in 17-18 that it had Highest ever export at 48313 MT in 17-18 against 42577 MT in 16-17. So the increasing PPI may open up an avenue for the company for exports and be a saving grace fir the company in Q1’22.

Conclusion

JK Paper and the paper industry may gain significantly if the domestic demand gets revived. As the company has a very high capacity of printing and writing paper a lot will depend on how the second wave progresses and lock down is eased. Also resumption of educational institutions may also be a key to the recovery. A key trigger will be completion of capex for packaging boards on time.

Key risks

- Usually cyclicals are to be picked when the margin is lowest. Currently the EBITDA margins are at 25% in Q4’21. So the margin of safety is low.

- Domestic demand revival is key. If the 2 nd wave is followed by a 3rd wave, domestic demand may get severely hit.

- Eventhough company’s expansion plan is justified by previous utilization levels and demand for packaging boards, it needs to be seen when the company will be able to achieve optimum utilization.

Please point out any inaccuaracy, many of the data is taken from ARs.

Discl: Invested and hence biased. Has used tikr, screener and thesis.com for arriving various conclusions. I may exit without prior notice if the idea doesn’t play out. Please do your due diligence.

What is the reason for poor sales figure compared to last financial year…any input?

The positive part is that the Sirpur Mills started contributing to profits. Dividend of 4 Rs gives a good signal despite the covid year where they got significantly hit.

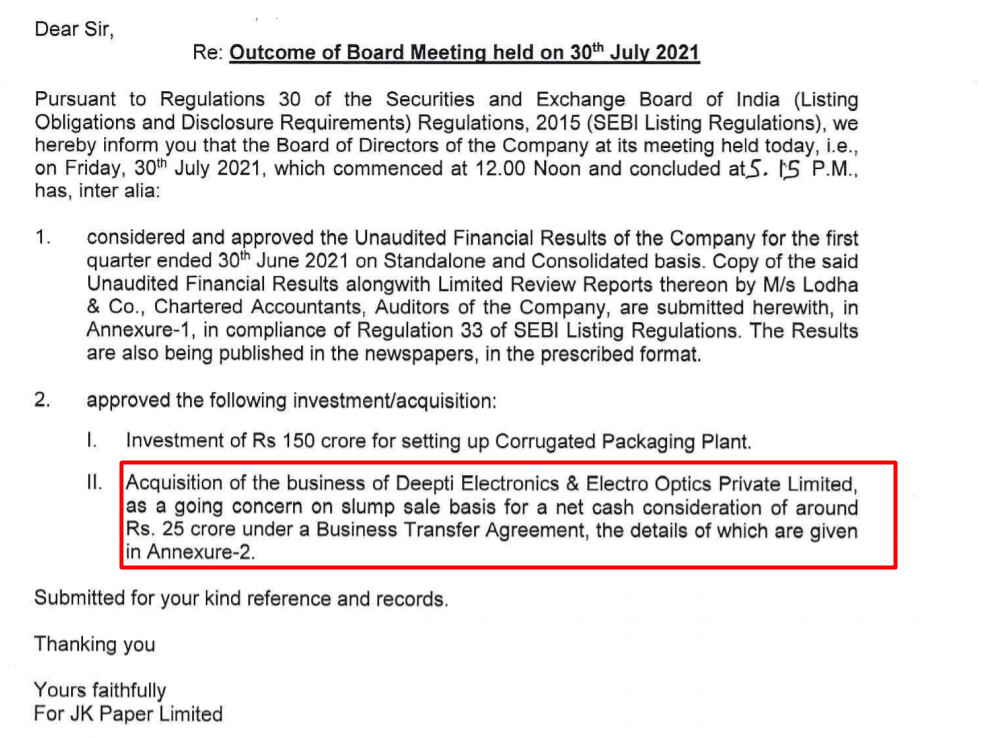

Company has incorporated a wholly owned subsidiary company

with the name “JKPL Packaging Products Limited” today.

150 cr cappex approved for Corrugated Box also.Corrugated box is high demand product and strong demand is there from exporters,domestic retail and online businesses. Going forward this is going to be exciting sector.

But is this 150 cr announced under newly incorporated JKPL or under same old entity?

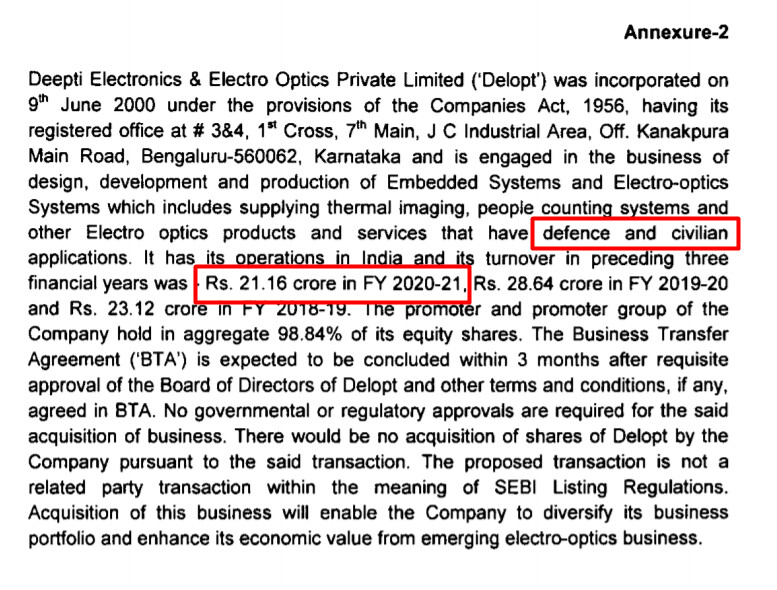

I went through website of Deepti electronics and optics and it seems hi-tech company catering to some reputed clients.

JK paper is a commodity player how they are going to bring technology bandwidth to manage such business?

Here is my piece of Analysis on the Paper sector from CRISIL Research data and my study on one Micro Cap Company Pudumjee Paper Products Ltd focussed on Specialty Paper and Hygiene Products within the Paper Segment

In manufacturing especially commodities whenever new capacity comes online and if there is reasonable demand it creates twin effect.

1.As the technology is superior quality is better.

2.Also new improved technology brings in efficiency and brings down cost of production.

Reasonable demand takes care of cost of servicing debts and creates good cash flows.

Jk paper has hit all the above three sweet spots and timing is also perfect.

Additionally replacement demand from single use plastic ban can create additional tailwinds.

Risks come from third or forth wave of corona, import duty reduction and execution risks in new plants.

But overall stock looks reasonably well placed among all other paper stock to capture favorable paper cycle over next few years.