Bro…I m getting the below numbers frm Moneycontrol for Q4 and Q3 of last year. these don’t match with ur figures.

what am I missing here?

Mar '17 Dec '16

Net Sales/Income from operations 40.30 67.85

EXPENDITURE

Consumption of Raw Materials 82.04 138.12

Purchase of Traded Goods – -- – -- –

Increase/Decrease in Stocks -37.81 -100.60

Power & Fuel – -- – -- –

Employees Cost 6.42 7.44

Depreciation 6.56 6.89

Excise Duty – -- – -- –

Admin. And Selling Expenses – -- – -- –

R & D Expenses – -- – -- –

Provisions And Contingencies – -- – -- –

Exp. Capitalised – -- – -- –

Other Expenses 16.81 19.50

P/L Before Other Inc. , Int., Excpt. Items & Tax -33.72 -3.49

Other Income 1.77 10.10

P/L Before Int., Excpt. Items & Tax -31.95 6.61

Interest 0.04 0.04

P/L Before Exceptional Items & Tax -31.99 6.56

Exceptional Items -59.24 –

P/L Before Tax -91.23 6.56

Tax -4.04 3.01

P/L After Tax from Ordinary Activities -87.19 3.55

Prior Year Adjustments – -- – -- –

Extra Ordinary Items – -- – -- –

Net Profit/(Loss) For the Period -87.19 3.55

If you see H2 for last 2 years you will see the following:

Sales 49.32 66.74

Net loss -5.26 - 1.16

So that means in H2 they have almost achieved break even in H2 last year.

If you observe they have reduced losses in H2 last year by Rs. 4.1 crores while sales had increased by 17.42 crores. This is classical operating leverage. This is because the fixed costs are around 35 crores for the half year.

JK is aggressively going for vegetable seeds sales which are concentrated in Q3 and Q4 and have high gross margins of 70%.

In theory if they increase sales in H2 this year by 20 crores they should achieve a profit of 6 to 7 crores in H2 this year (assuming that Fixed costs like R&D dont increase too much). This translates to EPS of 18 to 20 in H2 this year. H1 EPS was 35 so add 20 and we might end up with an EPS of around 55 this year. If they increase sales by 30 crores in H2 this year they should land up with an annual EPS of around 65.

From now on unless they increase R&D they should become profitable in H2 which was not happening in earlier years.

What is the site which you used to see the results?

I would put in a note of caution here. My projection of EPS of 18 to 20 in H2 this year can be curtailed by one time expenses of commercialization of BT cotton in Ethiopia and any increase in R&D.

Highlighting Mcap / Sales and Mcap / EBIDTA makes it look cheap in comparison to peers but neither feature in the higher debt on JK Agri’s books. There are other risks here:

- The ideological parent of the current Indian government has been inimical to GM seeds and the official policy towards GM is still evolving - it could end up favoring other farm inputs such as micronutrients. Lets not discount possibility of PRICE CAP on vegetable seeds like BT Cotton.

https://economictimes.indiatimes.com/news/economy/agriculture/how-monsanto-found-an-able-adversary-in-the-sangh-parivaar/articleshow/51592441.cms

- Changing behavior is very hard. Who will change the deeply-ingrained buying behaviors of Indian farmers? Who will bear the cost of “market making” in vegetable seeds? Farmers are also an economically vulnurable breed, so where is the guarantee of increasing margins?

Latest Economic Survey suggests farm incomes might not rise (having stayed stagnant for four years)

http://www.livemint.com/Politics/0WNR05OearQT7HVftPEJRM/Climate-change-may-reduce-farm-incomes-by-up-to-25-Economi.html

- R&D and Patents don’t necessarily equal sustainable advantage. The seed patents are not yet adding to the bottomline. In other industries we see Suven Lifesciences has a ton of patents, how does it compare to peers making generics as an investment? Point is - speculation is being priced in because there is no cash flow or evidence of earnings.

1 Like

About debt, they have got it down considerably due to which the credit rating have revised their rating for the better.

Plus they have a 20 crore aribration case in final stages. Hoping for a positive award which should effectively wipe out all their debt.

Dear Hrishi,

Would be highly helpful to have your view on Q3 numbers.

Yes. Here it. On first look seems a bad result with widening of the loss but a closer look and things seem a bit different

Yes

-

Cost of raw material as a percentage of sales has decreased.

Q3 2018 Q3 2017

Sales 20.56 18.94

Cost of material consumed 26.45 15.37

Change in inventory -18.16 -7.11

RM cost 8.29 8.26

RM % 40.32 43.61

-

There is a big increase in stock of finished goods to 18.16 crores from 7.11 crores Q to Q.

-

In the last two quarters we are seeing a big built up in inventories of around 22 crores. A large stock of finished goods has been accumulated. This clearly points to a postponement of sales to next quarter. While sales have increased just by Rs. 1.62 crores Q to Q the buildup of stock is much more almost 11 crores.

-

Other expenses has increased by 2 crores and R&D by 0.64 crores. I will give reasons I feel in my next post.

My analysis of the results in summary:

Net loss increase (1.46)

Attributed to

Other expenses increase 2.01

R&D expenses increase 0.64

Gross margins postponed 4.46 * 11.05 crores increase in inventory q to q X 60% gross margin

Adjusted profit’ 5.65

1 Like

The ETHIOPIAN Opening:

Some very very interesting updates on Ehiopia

- Ethiopia is moving towards commercialization of GM Cotton after almost four years of field trails at various locations in the country. This was done by the Ethiopian Institute of Agricultural Research (EIAR) on GM seeds obtained from JK Agri Genetics. Please find several articles on the Ethiopia’s maiden foray into GM cotton and on the GM cotton scene in Africa in general.

http://allafrica.com/stories/201710110695.html

http://www.vib.be/en/about-vib/plant-biotech-news/Documents/vib_fact_CottonAfrican_EN_2017_0901_LR_FINAL.pdf

- Ethiopia has declared a strategy about cotton which states the following:

The strategy was launched with the view of tackling the challenges faced following ever growing demand for cotton in the country. The strategy is designed to increase the size of land cultivated with cotton to 250,000 hectares and one million hectares after five years and in 2032 respectively from the current 80,000 hectares of land

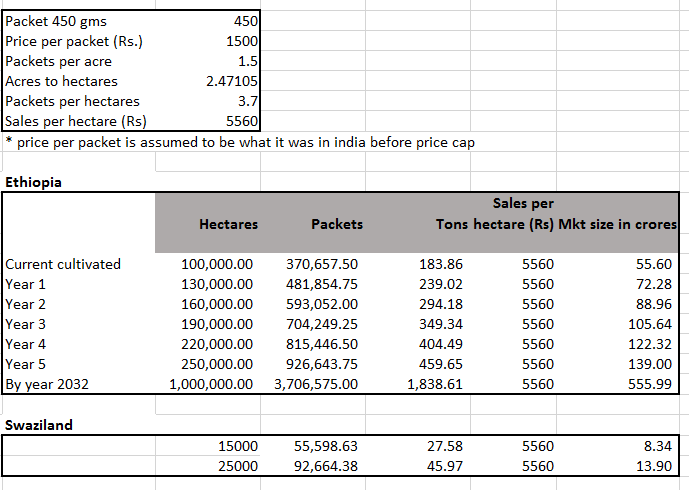

3.I have attached some rough calculations on trying to come up with a market size for GM cotton seeds for JK Agri Genetics.

-

Based on this the total market size i guess will be in the range of 50 crore to start with and 150 crore plus over the next few years.

-

JK Agri GM cotton seed trait will be the only approved one in the market and they have gone through field trials for the last 4 years. Infact, Ethiopia bypassed Monsanto to choose an Indian company as they did not want the country as they say to be an ‘experimental lab’ for Monsanto. This is especially relevant because of perceived failure of Monsanto BG2 in India and parts of Africa.

As usual market takes a short term view and only goes by quarterly numbers  Going forward expect increase in one time expenses and R&D costs in the short term which will squeeze margins as they move towards commercialization in Ethiopia and Swaziland.

Going forward expect increase in one time expenses and R&D costs in the short term which will squeeze margins as they move towards commercialization in Ethiopia and Swaziland.

2 Likes

how about the increase in interest cost?

A friend involved in agriculture posited that most loss of agricultural productivity in India is due to wastage, so GM seeds seek to solve a problem that does not exist. This is particularly in respect to vegetable growth, which is from medium to large sized farmers. Since this is the clientele for GM seeds - one consideration is whether the farmers will focus their funds on storage and reducing wastage (output), rather than increasing yield further (input). Thoughts are invited.

1 Like

Your friend is short on facts:

- http://www.thehindu.com/news/cities/mumbai/pink-bollworm-may-eat-up-half-of-states-cotton-crop/article20493492.ece

If this a problem “That does not exist” then I have nothing further to say.

- In the vegetable seeds there is no GM seeds involved just hybrids. Other than cotton and prospective approval for GM mustard no other approval for GM has been granted.

About reducing wastage yes that is definitely a problem but this is not an either or situation.

@hrishikesh Hrishikesh, Good to see your very enthusiastic post on JK Agri Genetics. Thanks for the thread.

My questions:

-

What is going to change now? if I understood correctly, you mean to suggest that the Vegetable seed business would start growing rapidly anytime soon. What are the key reasons to have this hypothesis is unclear to me… Did they reach any critical milestone in innovation, marketing, brand building? This insight would be useful.

-

The vegetable is perishable, price fluctuation is high and cultivation depends on cultural preference of the local market (correct me if I am wrong). I am not sure if Vegetables can be transported a long distance like a field crop. Unless the agricultural infrastructure of the country is substantially improved, do you feel a large market of seeds for Vegetables can be created? I don’t know, and like to know your views.

-

Even if JK Agri have spend huge sums in R&D and created the best seeds, selling depends on Marketing and Demand generation… I am unable to make out what new things JK Agri is doing to make a change in their fortune in the immediate future… Please help to understand.

-

It would be good if we can have data of the past sales break up between Field Crop & Vegetables? Can their products be used across the geography? What are the key benefits of their Seeds vis a vis what farmers / planters use presently?

-

I find JK Agri has 410 employees with average employee cost of Rs. 6.58 Lakhs as on Mar 17 against Kaveri Seed’s 793 employees with average employee cost of 4.03 L. Total Employee cost of JK is 27 Cr (sales Rs. 192 Cr) against Rs. 32 Cr for Kaveri (sales of Rs. 700 Cr) … Why so many employees and why per employee cost is so high? R&D Expense of both companies are almost same at Rs. 12 Cr … so possibly JK spends more on R&D compared to its size but it doesn’t fully account for the difference to me.

-

Kaveri has Rs. 69 Cr receivable for Rs. 700 Cr sales and JK Agri has Rs. 60 Cr receivable for Rs. 192 cr sales… Why so high a difference in receivable? It is a critical factor in farm product sales as chances of bad debt may be quite high.

-

Why the money of Rs. 32 Cr is under arbitration? What is the root cause and genesis? Any idea?

-

One good thing I find is JK Agri pays tax which Kaveri doesn’t. However, in this Q3 2018, they made loss but provided for tax… What is reason?

Your answers would really help all of us to understand the company better.

11 Likes

What is changing now?

A lot really. I will break it up into smaller parts:

- For vegetables please access CARE report.

http://www.moneycontrol.com/stocks/reports/jk-agri-genetics-credit-rating-10141481.html specifically to para on focus on vegetable seeds.

This can be verified by comparing Q4 results of FY 2017 with Q4 results of FY 2016 47.60 vs 32.95 crores. Due to this they could almost break even last year in H2 where traditionally all seed companies make losses and eat into Q1 profits essentially. If they achieve the same growth in Q4 this year, then H2 will swing into good profits as the gross margins in vegetable seeds is a high 70% due to absence of price caps as in cotton seeds. However, I will qualify the above statement as we may take a hit in increased r and d spend and one time other expenses due to commercialization of cotton in Ethiopia. If not, we should aim at a 50 EPS for this year. Vegetable segment is the fastest growing in the seeds industry growing twice as fast as the other field crops. (Refer Kaveri presentation). Kaveri is 5 years behind JK as they have just started their vegetable seeds journey while jk is in it for the last 8 years (which is the normal cycle for a seed to be commercialized).

- As I said H2 is the weak half. I am expecting exports to pick up in the next 3 years to Africa for BT cotton especially to Ethiopia. The market size there is a huge 150 crores and JK is the only BT cotton trait approved by the EAIR. The margins there will be much higher due to absence of price caps. H2 in 3 years can be as big if not better than H1 with vegetables seeds and African exports (African cotton season is in H2).

- In India Monstanto is in deep trouble due to failure of BG2 and unauthorized sales of BG3. Nath and JK are the only other two companies with their own BT cotton traits. Kaveri , Nuziveedu etc source this technology from Monsanto and I don’t know the impact this year in Kharif season. But it does not seem good.

In seeds growth is not linear. Third year is usually the boom period. I am expecting JK Pass Pass to do much better this year (3rd year) from the 6 lakh packets it sold in last kharif season. If they don’t achieve minimum 10 lakh packets I will be disappointed.

4. Government is geared to clamp down on the unorganized markets due to the spurious seeds menace. This being election year I think they will surely ensure a good rabi season. Unorganized markets are going to be eliminated is my guess.

5. Vegetable seeds is a localized market and each region has its flavors of hybrid. That is where the big R&D spend comes into play. JK group has a huge distribution channel and localized r and d support, and I hope they leverage it.

6. AS in the CARE report: JKAL is focused on increasing the share of the vegetable segment in the overall sales bucket as they offer better margins compared to other field crops & cotton. Share of vegetable segment in total sales have increased from 25% in FY15 to 38% in FY17.

7. On employee cost they are spending 5.21 crores on R&D annually. Don’t know about Kaveri. Why employee costs are higher in JK we need to research honestly. But on R&D spend both are spending almost equally but % to sales is much higher in JK as is obvious.

8. I am gunning for 300 crores turnover conservatively due to increased vegetable seeds, Africa cotton and increase in sales in indian BT cotton in next 2-3 years. Even after factoring an increase in R&D by 10 crores I am gunning for a 100 EPS here in next 2 years because of high margins in Africa and vegetable and operating leverage effect as all fixed costs (including r and d increase) is factored in. In Sudan, they went from 0 to 95 percent GM adoption in 3 years. Ethiopia with a 150-crore market with JK having monopoly can be a gamechanger.

9. About the arbitration you can access the announcements they have filed on BSE

http://www.moneycontrol.com/stocks/stock_market/corp_notices.php?autono=6331481

If they get a negotiated settlement of 20 crores odd, it will take off their long-term debt to a large extent which is 27 crores and already reduced from the year before 37.38 crores.

10. About receivables frankly I don’t know and is a cause of concern and needs to be checked.

Anyways I will like to warn this is going to be a 3 year story. Quarterly results can be skewed due to one off expenses higher r and d spend it. So not for those keen to make a fast buck. Hope this helps.

10 Likes

http://www.ethpress.gov.et/herald/index.php/technology/item/9824-ethiopia-s-move-towards-bt-cotton-commercialization

From above news it seems that JK Agri Genetics has first mover advantage and also possibly the institutional mechanism would support maximum one or two players in a specific geography as seems from the below attached report. It says, as on Dec 16, trial for only JK Agri generics BT Cotton in going on in Ethiopia and Swaziland has already approved it. International Plant Technology Outreach 2016.pdf (2.4 MB)

Lot of textile companies including likes of Raymond are opening Textile factories in Ethiopia so there may be opportunity.

I am yet to find out how the currency movement are in African countries… Most fluctuate widely around US$ … How that can affect companies like JK Agri…

Also any idea about the total Ethiopia market size would be useful.

This is the rough size i have calculated. But actual sales will not follow a linear trend. Generally for first year

seeds are distributed free or at low rates and third year is usually the bumper year.

3 Likes

EPS for FY18 came out to be 33

Any idea if Ethiopia operations started? Doesn’t look like Sales figures have sales from Ethiopia included.

COGS as % sales have increased from 50% to 53%.

Please read the following article carefully

http://allafrica.com/stories/201803300522.html

The commercialization is in last stages. African cotton season starts in September October so u will see the first sales to ethiopia coming this financial year. Sudan has gone from 0% to 100% GM Cotton seed adoption in 2 years flat. So next two years will be interesting here as JK has exclusive rights to GMO cotton in Ethiopia.

I will attach the relevant section.

1 Like