Rathi → by FY25 expect to have 70% utilization; this will have wire rods and rebars; expected run rate of 9-10k tonnes/month; 4-6k ebidta/tonne in FY25; 150crs of capex → some of it already incurred, in FY25 around 75crs of capex will happen

Rabirun → in H1FY25 should be able to start the plant; current capacity of 4-5k tonnes/month, eventually want to make 8-10k tonnes/month in the pipe and tube segment; in the beginning i.e. H1FY25 will only have 1-1.5k tonnes/month volume; Approx 75crs of capex; 100% JSL material will be used (generally 50% 200 series, 50% 300 series)

Iberjindal → in the future expect to have good demand when the European market rebounds; in FY22 did ebitda of 109crs, and PAT of 80crs; management is very bullish hence bought the stakes

Jindal Coke → valuation hasn’t been decided, ebidta last quarter was 56crs, debt 450crs; net debt ~300crs

Capex FY24 → earlier guidance was 3300crs which has been increased to 3600crs for two reasons

– Rabirun → 100crs

– NPI → tranche of $26million (225crs) being preponed to March

Pipe and tube business in the next five year will grow at 10-12% cagr

Series 400 → every quarter 2-3% contribution is increasing; currently 25% contribution

Freight Cost → not passing on the increase in cost right now, if the problem persist will pass

Guidance → 19-20k ebitda/tonnes; see good demand in the domestic market

Jindal Stainless announces Rs.5,400 cr strategic investments as part of its plans to augment its melting and downstream capacity → melting capacity to go up by as much as 40 percent to 4.2 MTPA

Becomes the largest stainless steel player ex-China

Below expectation Q4 results for JSL due to nickel prices. Expected to recover in coming qtrs.

Expecting 20% volume growth for FY25

Confident on domestic demand (8-10% growth) but US,EU demand is still not recovered to full

EBITDA per tonne target for FY25 is around ₹18,000-20,000 (FY24 ₹18,558)

Interesting price movement post results today: Stock opened at 615 with a big gapdown but recovered fully within the day and closing above last day’s price. (11% recovery intraday)

Does this mean market is bullish and confident on JSL?

Sales volume 5% up YoY, 1% up QoQ (Composition: 10% exports, 90% domestic)

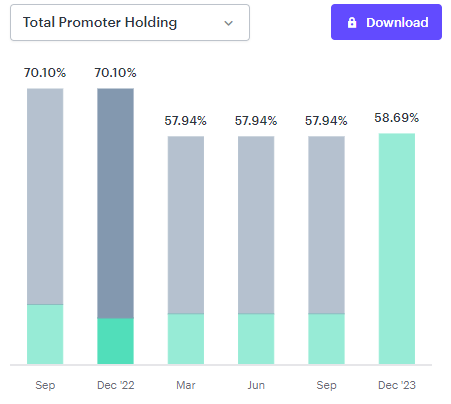

FII holdings increased to 22.49% from 20.83% QoQ

FY25 Targets

Volumes +20%

EBITDA/tn range 18k-20k/tn

Commentary:

stagnant growth in the US and EU markets, the export volumes of the company have remained flat on a QoQ level

ongoing Red Sea issue extended transit times and freight cost from India to the western markets, and paucity of containers further affected exports

company sources most of its raw materials from nearby shores and domestic suppliers, the company was largely able to mitigate cost and time risks arising from the crisis

Cheap imports from China and Vietnam continue to pose threat to the domestic industry

Other points:

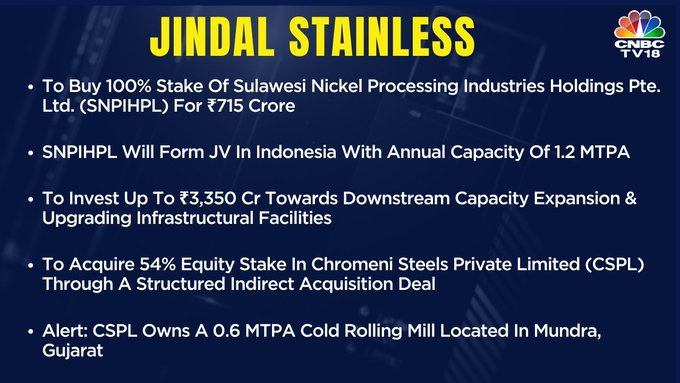

During the quarter, with an investment of approximately Rs 715 crore, the company entered a JV to develop and operate a stainless steel melt shop in Indonesia with an annual production capacity of 1.2 million tonne per annum

The company also set aside around Rs 1,900 crore and Rs 1,450 crore for the expansion of its downstream lines and upgradation of infrastructural facilities respectively, in Jajpur, Odisha

During the period, the company completed total acquisition of Chromeni Steels Private Limited (CSPL), which owns a 0.6 MTPA cold rolling mill located in Mundra, Gujarat, for over Rs 1,600 crore, comprising payment towards equity transfer and payment of shareholders’ debt

Jindal Stainless Limited maintains a positive outlook, expecting strong domestic demand across major segments. The company achieved its highest-ever sales in Q1 FY25, with a 5% year-on-year increase. Management remains confident about achieving 20% volume growth for the full year FY25, driven by infrastructure spending, railway expansion, and growth in new sectors like renewable energy and nuclear power.

Strategic Initiatives:

Acquisition of Chromeni Steels: JSL completed the acquisition of Chromeni Steels Private Limited for over INR 1,600 crores, adding 0.6 million tons per annum cold rolling capacity.

Co-branding schemes: The company is expanding its successful co-branding initiative beyond the Pipe & Tube segment to other consumer-facing segments like utensils and hollowware.

Capacity expansion: JSL is ramping up its nickel pig iron (NPI) plant and expects to start operations by Q3 FY25.

Channel financing and market research: The company is focusing on deeper tier market research and channel financing to extract better value from customers.

Trends and Themes:

Increasing domestic stainless steel consumption in line with GDP growth

Growing demand in infrastructure, railways, defense, and new-age industries

Focus on value-added and high-margin products

Emphasis on sustainability and environmentally responsible operations

Industry Tailwinds:

Government’s infrastructure push and increased capital expenditure

Growth in railways, nuclear power, and renewable energy sectors

Rising stainless steel demand in new applications like LNG terminals and desalination plants

Implementation of BIS certification norms to potentially curb low-quality imports

Industry Headwinds:

Red Sea issues affecting export logistics and freight costs

Intense competition from imports in certain segments

Global economic uncertainties affecting export markets

Analyst Concerns and Management Response:

Export market challenges: Management expects improvement in H2 and is exploring new export markets like Japan, South Korea, and South America.

Debt levels: The company maintains its focus on prudent financial ratios and aims to keep net debt to EBITDA below 1.5x.

Management bandwidth for expansion: JSL is proactively working on developing leadership talent to handle growth.

Competitive Landscape:

JSL maintains its strong market position in India. The company is focusing on high-margin segments and value-added products to differentiate itself from competitors. The acquisition of Chromeni Steels enhances its competitive edge in cold-rolled products.

Guidance and Outlook:

20% volume growth for FY25

EBITDA per ton guidance of INR 18,000-20,000

Net debt to EBITDA ratio to remain below 1.5x

Capital Allocation Strategy:

JSL’s capital allocation focuses on growth investments, dividends, and maintaining a strong balance sheet. The company has taken an enabling resolution to raise up to INR 5,000 crores through equity-like instruments for future organic and inorganic growth opportunities.

Opportunities & Risks:

Opportunities:

Expansion into new export markets

Growth in domestic infrastructure and new-age industries

Potential for further value-added product development

Risks:

Volatile raw material prices, especially nickel

Geopolitical tensions affecting global trade

Potential economic slowdowns impacting demand

Regulatory Environment:

The implementation of BIS certification norms is seen as a positive step for the industry. JSL is actively engaging with the government on the proposed National Stainless Steel Policy, which could provide further support to the sector.

Customer Sentiment:

Customer sentiment remains positive, especially in domestic markets. The company’s co-branding initiatives are helping to build stronger relationships with customers and end-users.

Top 3 Takeaways:

JSL maintains strong growth momentum with 20% volume growth guidance for FY25, driven by robust domestic demand and strategic initiatives.

The acquisition of Chromeni Steels and ongoing capacity expansions position the company for future growth in value-added products.

Despite challenges in the export market, JSL is actively exploring new geographies and maintaining a focus on high-margin segments to sustain profitability.

JM Financial initiated coverage report on Jindal Stainless with target of 910/sh

They had given EV EBITDA multiple of 10, please study report and give your feedback of this multiple