Jindal Stainless (Hisar) Limited (JSHL) is India’s first fully integrated stainless steel manufacturer with a capacity of 0.8 MTPA.

JSHL is world’s largest producer of Stainless Steel strips for razor blades and India’s largest producer of coin blanks, serving mints worldwide.

Currently, the only specialty stainless steel producer in India

Key projects / products:

SS fuel tanks (Ashok Leyland, Eicher Motors, Tata Motors)

SS exhaust systems for commercial vehicles (Ashok Leyland, Tata Motors)

SS bus bodies (Karnataka/ Telengana/ AP/ Goa State Transport Corporations, Volvo)

SS tanks, pipes and tubes are extensively used in the chemical industry

SS tanks and utensils in the dairy, beverage and food processing industry

Industry

Stainless steel is an alloy of Iron with a minimum of 10.5% Chromium. Chromium produces a thin layer of oxide on the surface of the steel known as the ‘passive layer’. This prevents any further corrosion of the surface. Increasing the amount of Chromium gives an increased resistance to corrosion.

Stainless steel also contains varying amounts of Carbon, Silicon and Manganese. Other elements such as Nickel and Molybdenum may be added to impart other useful properties such as enhanced formability and increased corrosion resistance.

India is currently the 2nd largest producer of stainless steel after China

The SS industry is growing at 8-9% yoy. The growth is in response to the rising demand for stainless steel, mainly from sectors such as auto, roads and highways, housing and the like.

Imposing a definitive countervailing duty (CVD) on certain stainless steel products from China have helped the industry. Government had removed the import duty on nickel, a key material required to produce stainless steel

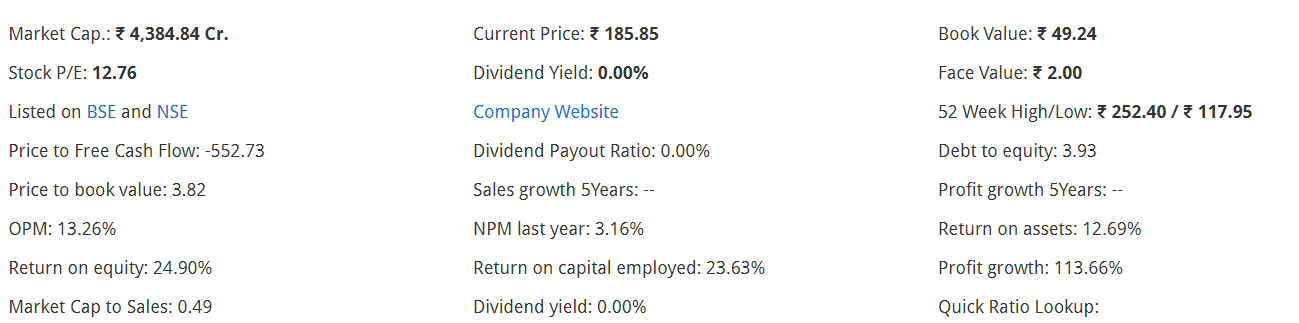

JSHL has been profitable at the operational level even before the demerger from JSL

RoCE and ROE are healthy

Debt is a major concern and is a key monitorable

Profit growth is very strong and the momentum is likely to continue

Valuations are reasonable. Company is available at 0.5x Market Cap / Sales

What is changing?

Majority of stainless steel was imported from China; with the CVD in place now, major shift of market share to Indian players is expected. JSHL is to be one of the most important beneficiaries of this shift.

Strong demand from traditional segment of kitchenware & utensils the growth will be largely driven by ABC (Architecture, Building & Construction) segment, ART(Automobile, Railways &Transportation), process industry segment & defense sector.

Focus on niche areas - Signed a license agreement with the Defence Research & Development Organization (DRDO) for manufacturing high nitrogen steel (HNS) for armour applications

With more stringent norms like Euro-VI kicking in by 2020, consumption of stainless steel is expected to get a boost, as SS reduces the weight of a vehicle.

Business Risks

JSHL has very high debt – 2774 cr (in aggregate) with 408 cr of interest payment during FY18.

JSHL has high receivables / sales ratio, though it is reducing (~8% in FY18 vs 12% in FY17)

Co has a single location operation in Hisar which increases geographical risk

Reduction or removal of CVD of imported Stainless steel

Significant delays in infrastructure spending, specially on railways & defense sectors

Diclosure: I am invested from lower levels. Please do your own due diligence before investing.

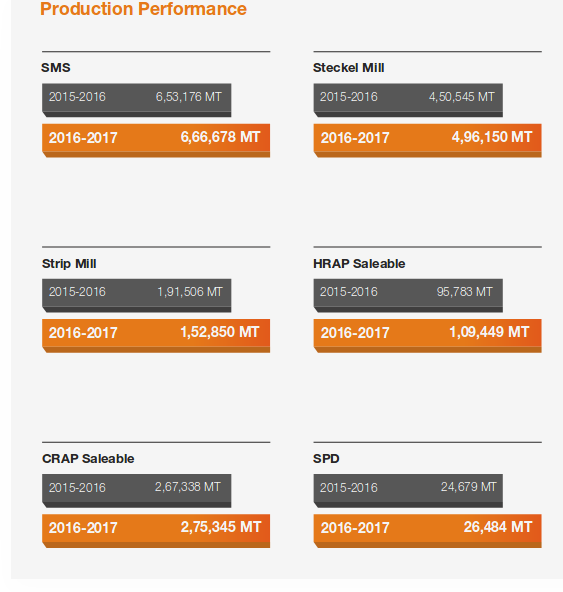

As per FY17AR, the production totals to 17,26,956 MT (M stands for Metric or 1000 kg )

Stated capacity is 0.8 Million Tonnes per Annum

So capacity utilization works out to 2x ??!! I guess i am missing something in basic calculation. Please help.

I am sure there are nuances like production capacity for each type of product, but most likely i am doing some silly mistake in calculation ?

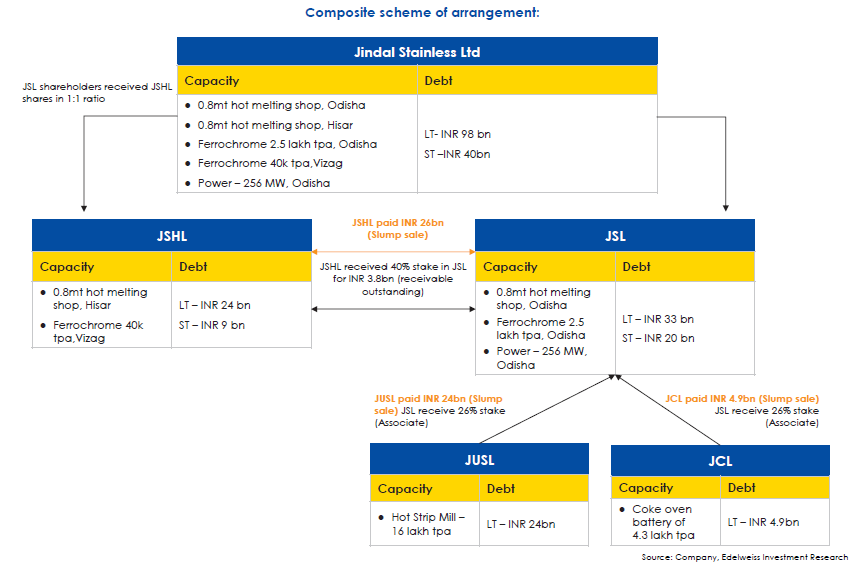

If one sees the diagram below, the company has reduced its long-term debt from 98 bn to 85.9bn. Also, as Hisar is a stable operation, it has been profitable at the EBITDA level and thus can service its debt and remain profitable.

Jindal Stainless Ltd and Jindal Stainless (Hisar) Ltd – is aiming at a 15-20 per cent jump in topline in the 2018-19 fiscal, betting big on higher value-added product mix.

“Stainless steel demand in India is growing at 9-10 per cent, while our growth is expected to be at 12-13 per cent. But, due to higher value-added product mix, our revenue is likely to jump by 15-20 per cent,” Jindal Stainless Group Sales Head Vijay Sharma said today.

@basumallick

sir

i am in huge loss in jindal hisar. can you please share ur views on its future outlook? and why its falling from 200 levels to now 99 levels?

vivek

Enclosed is the research report on a buy in November 2018 at 100 at the CMP of 89 there is a good deal. This correction may be good opportunity to accumulate.

I have been tracking JSL for a while now. The way i see it there are 2 main triggers to for the stock to realize its potential.

One is the exit from CDR. They have been trying hard for a while and i feel this year will be the one they finally exit from it.

Second is the insane pledging of the promoters. Unless im mistaken its at 90%+.

In last 2-5 days the MD , Abhuday Jindal has been buying up stake left right and center.

I feel this will be the exit of CDR.

The company has to pay import duty on ferro chrome and stainless steel scrap which is imported. If the government was to offer protection to the industry then thier profits would zoom up multi fold.

JSL and JHSL are India’s largest producers for Stainless Steel.

The debt overhand once removed would be a 2-3 x easy.

The expanse is high more than 82% however the material cost is in range 59% to 63% . The opportunity size is small .

Supplier power of scrap is low when the steel prices are low but supplier power shoot up when there is increased demand for scrap from the emerging economies we have witness same in 2005.

Overall the sector is in RED . The Green is that government intervention able to boost bottom line and reduced the import nut at the same time the import duty is high on steel scrap .JSHL will face modest revenue growth to continue going forward .

Performance of subsidiaries is adding jewels in the crown (Jindal Stainless Steelway Ltd (JSSL) & JSL Lifestyle Ltd (JLL))

what i have observed that Unfortunately, most of raw materials e.g Nickel, Chrome, and scrapped Stainless Steel is being imported in India and there is 2.5% import duty on these.

The Major ASEAN countries are dumping excessive production in india via Indonesia route .The landing cost of that steel is low as compare to domestic .

Disc : This is not any purchase sale or holding advice . I am not SEBi approved Analyst .the valuations seems mouthwatering but not invested .

I have tried to estimate the fair value of JSL Hisar.

The management in its concall has said that it had 18000rs/ton Ebitda in this quarter(Q3 2021) and due to removal of import duty on stainless steel by the government in the budget. Ebitda might drop to 14000rs/ton as guided by the management. Management says there is a healthy demand in export market from Russia and other countries, if there is drop in prices due to dumping by China and Indonesia, Co will look for export market. So assuming management walks the talk I have proceeded with my calculation.

Q3 2021 EBITDA = 350

Ebitda (future) for q4 and so on = 14000/18000*350 = 272.33

For margin of safety lets assume EBITDA as 230 cr

For full year q4 2021 to q4 2022 EBITDA = 920cr

Debt = 2090cr

Mkt cap = 2800cr

Enterprise value = 2800+2090=4890cr

EV/Ebitda = 4890/920= 5.31

For steel sector EV/Ebitda of 5-8 looks reasonable. Is it okay to say Hisar is reasonably valued? or does the stainless steel sector have different dynamics to the steel sector? I understand that the company has a branded B2C company JSL lifestyle and a stake in JSL but do they change the underlying business valuation? If I should account for them what could be the fair value?

Experts please look into this I may have missed something in my calculations.

Disc: invested