Very true. The company needs to invest in TV advertising which is very expensive otherwise I don’t see consumer base expansion.

For rest of the products margins are low, which they are supplying to patanjali,colgate etc.

Not invested.

Very true. The company needs to invest in TV advertising which is very expensive otherwise I don’t see consumer base expansion.

For rest of the products margins are low, which they are supplying to patanjali,colgate etc.

Not invested.

I wonder whats the Ad deal with HT media is doing, is it really helping JHS in any sense ? have you guys seen any Ads in HT media ? agree Ad spending is very key to the FMCG business.

Disc: Invested

HT Media is suppose to do advertising for jhs…that’s why there was a equity dilution a few months back.HT media holds a certain percentage of JHS.In return HT Media will do advertisement for JHS…Presently their own brand is contributing 10% of the revenue, They have targeted to take it to 50% by 2020 which is highly possible looking at the small size they operate till now.If they achieve this number OPM will go up significantly… Now market is pricing them a niche contract manufacturer but slowly market can give it a FMCG premium…

Disclosure: invested

The pricing of toothpaste is very competitive for example Colgate 50gm pack is of 19rs.

So as a customer why I would buy aquawhite ? Any issue with quality of Colgate ? or any additional benefit of aquawhite ?

So unless and until their market share increases and is shown on paper, I would monitor it.

I am ready to pay more once they build the confidence and grab consumer base.

(It would be very nice if someone on board use their product and give us a review.)

You may refer to jhs presentation…which has it’s new range of products they are coming up with.They are targeting specific segments…Colgate market share may be at 56% still 44% left for other players.Colgate is loosing market share as well… When jhs starts advertising , it can be seen how much market can they capture…I have not used jhs paste …But if they supply Amway , I suppose they should have good quality…But then I will wait for people to say…

Nanda in a TV interview (2 months back) stated that they will begin advertising in Q3 this year. So lets wait and watch.

Sagar: If you look at JHS’s corporate presentation released about a week back, the market they are targeting is the Kids market with Chota Bhim and other cartoon charaters. This is akin to Happy Meal strategy of McDonalds and Crax of DFM Foods. This will end up creating a new category by itself. Therefore, the market share aspect although relevant should not influence decision making. We also need to be vary of JHS trying to tell investors that they have a large market share of a small market though.

Parag:

My sense is leaving MNCs aside we now have market share from Patanjali and Dabur. These act as Dollar Shave against Gillette. Now we know that while design is an important aspect, distribution seems to the order of the day whether it is Dollar Shave or Amazon. Established brands are spending sleepless nights while Private Labels across the world are giving them a tough fight. The key is distribution costs have been a great leveler. My sense is the margin on this product is relatively small - as it falls somewhere been staple and discretionary. JHS would be happy to make a private label for Future or Amazon given its stated strategy of 50% and 50% own brands. Our analysis should be based on if Amazon or Future wants to make a private label who would they go to? Is JHS the preferred partner. My sense it is collaboration and not necessarily competition for JHS to win this battle.

As regards valuation, this is where I tend to feel that we are somether between a convertor and a brand? Would it ever trade at PE multiples closer to say other brand owners? that is a question which we should be looking for an answer.

Colgate reported subdued Q2 results, some signs for JHS?

Patanjali Taking the market share? then good for JHS contract business but for the in house brand ?

Results will speak for JHS as they have been or past 20yrs or so. IMHO Nikhil Nanda makes appearances whenever there is a bull run, check for his videos back in 2008-09 when he was saying on media that they are in talks with big players etc, also media houses were recommending the share and there stock zoomed like anything.

Recently he is appeared on TV in 2017 quite a few times.

Negatives for me:

No profit growth.

Low margin business.

Dilution of equity 2X in 2years.

These are my observations kindly feel free to comment.

Just like us the promoters of Companies undergo transformation. This is where the real test comes - JHS came back from the brink with P&G outsourcing case. To me:

If he stumbles on 1 above, we all invested blokes eat crow. My sense is he would find it challenging on 2. But this is where he is taking help from Sixth Sense who have a team from FMCG cos (ex-Colgate etc)

Jury is out.

Let us see how this plays out!!

I was invested earlier, but booked out couple of months back.

Right now this is a story which I want to track, but only from the sidelines.

I kind of agree with @arvind.calyx about Mr.Nanda being very flamboyant wrt his projections. I am usually wary of such promoters who try to sell their business too hard.

An additional point that i would like to throw in for comments:

The business model for MPS Ltd and Repro are somewhat close? These companies could give us valuation benchmarks for JHS.

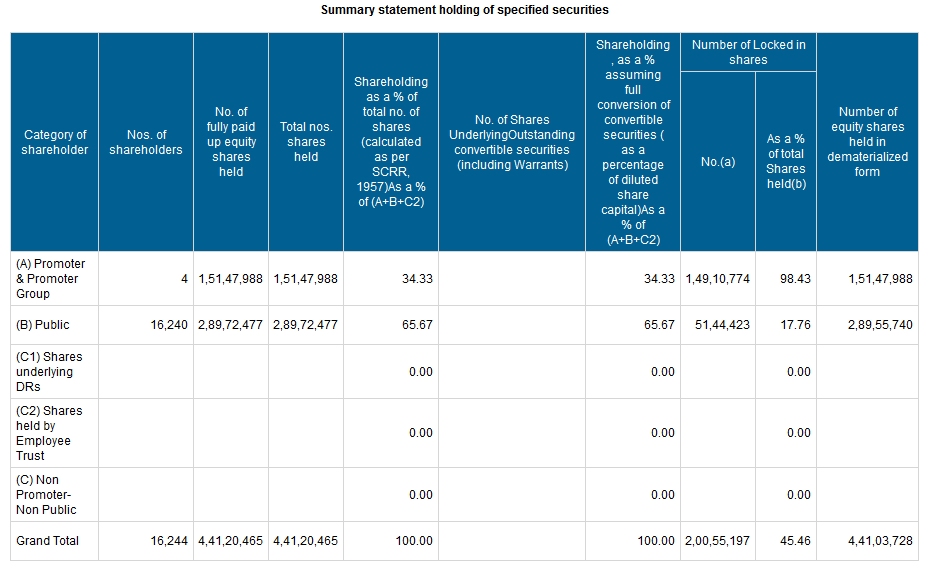

Well the shareholding pattern says that Investors and promoters have reduced their stakes:

NRI’s, sixth sense,HT MEDIA, etc have reduced the holdings.

dear sir some companies taking the delivery charges for delivering the goods ,some companies provide free delivery and some provide cash on delivery option also when the order is more than 499. Please check Amazon site or app once more .thank you for your input

Promoter shareholding has increased from 33.97 (June Quarter) to 34.33 (September Quarter), Can you check again?. Also, HT media has reduced the shareholding marginally by 0.12% and sixth sense by 0.21% (Looks like normal profit booking as share price has double)

Yes checked again, and yes the promoter holding is increased, but you can see that they have diluted the equity.

So I the increased shareholding is due to the additional dilution of equity ?

Yes that is correct, increased share holding is due to equity dilution, shares offered to HT media was one of the reason for them to do advertising for JHS which will start second half of this financial year…

Sixth sense selling continuously in open market, anybody having any idea about this???