Started in : August 1997

Market Cap.: ₹ 132.80 C

Background:

Fast moving consumer Goods (FMCG) is the fourth largest sector of the Indian economy and the most consistently growing one too. Furthermore, it is the only sector that has created long term wealth for the market participants over the decades. Within the sector, Oral Care is a niche sub-segment and one of the fastest growing one. Therefore, if we get an interesting story in the sector, one should strongly consider it. Increasing disposable earnings, growing middle class, rising oral awareness, convenient oral care products, growing distribution chain and logistics storage, increasing toothpaste penetration, development in oral care solution segments and others are some of the factors expected to drive the industry’s growth in the coming decades.

The Company:

JHS is one of the biggest toothbrush contract manufacturers in the country and more excitingly has now launched its own set of branded oral care products under the brand “Aquawhite”. The company will have complete set of oral care products like tooth brush, power tooth brush, tooth paste, mouthwashes, dental floss and even oral care chewing gum. Company launched Aquawhite last year with its range of tooth brushes and tooth paste and is set to launch other products in the coming few quarters. Company has launched its tooth brush and paste in the North and East markets and is currently launching them in the southern and western markets as well. The TV advertisements have also started for these launched products. Within the first year of launch these oral care products have given around 12cr of revenue and with the launch of these brushes and toothpaste in the other two markets and impending launch of other oral care products, the future looks extremely promising. This is of course in addition to the contract manufacturing business which itself is growing by leaps and bounds.

Facilities:

- Noida Special Economic Zone which is an Export Oriented Unit, established in July 2003 and the

- Kala Amb, Himachal Pradesh, which is a tax free location (till 2020), established in April 2007

Management:

- Nikhil Nanda Managing Director

- Manisha Lath Gupta Additional Independent Director

- Piyush Goenka Nominee Director

- Vanamali Polavaram Non Executive Director(aged 66)- retired as Resident Commissioner

- Chhotu Ram Sharma Independent Director (aged 69)- He was the managing director/CEO of Bank of Punjab Ltd. from 30th June 2002 to 30th Sept 2005

- Mr. Mukul Pathak Independent Director

- Vishal Sarad Shah Additional Director

- Mr. Nikhil Vora Nominee Director

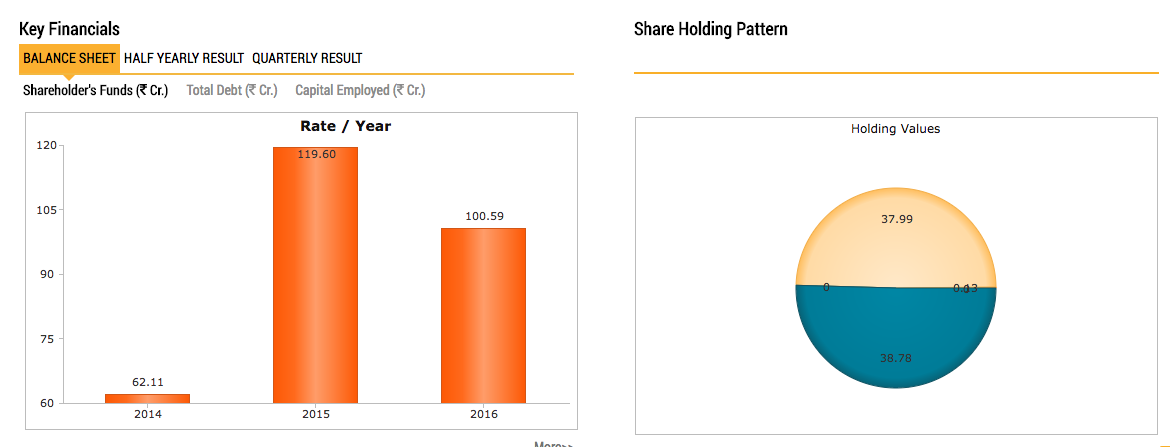

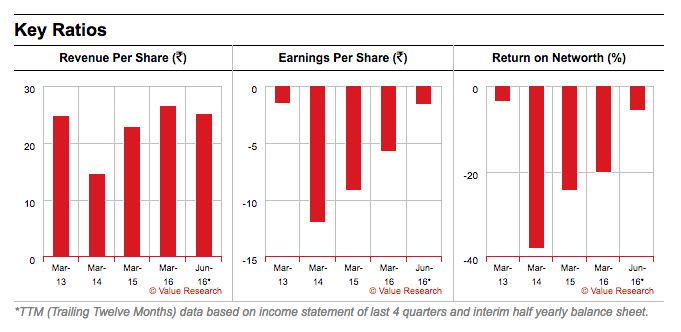

Financials:

Success Stories:

- There are a number of reasons why one is optimistic of our prospects:

- Tano Mauritius took a 14.6% stake in our Company for 24.44 crore

- Commenced the manufacture of ‘Shiny Clean’ brand toothbrushes, a sub-segment of the Oral B family

- Added large global FMCG brands to our client list which will help us completely utilise spare toothbrush capacity from a prevailing 70%

- Operated our laundry product facility at more than 100% capacity in the second quarter of 2011-12. The private equity funding in February 2011 was an important event in 2010-11, a confidence-enhancing watermark. Invested these funds in procuring moulds and other equipment for making toothbrushes for global FMCG brands; this investment will yield results over 12-18 months.

Pros:

- Company has reduced debt.

- Company is virtually debt free.

- Company is expected to give good quarter

- The penetration of modern oral care products in India is low (toothbrushes 48.6% and toothpastes 72.3%).

Cons:

- Company has low interest coverage ratio.

- Company has a low return on equity of -17.31% for last 3 years.

- Contingent liabilities of Rs.210.56 Cr.

- Company might be capitalizing the interest cost

- Inputs are linked to global crude prices. The economic crisis in Europe and the US has stabilised global oil prices at US$ 100 per barrel and this is expected to sustain.

Disc: Not Invested. Too risky call to take as Indian market is dominated by one player Colgate, and it may remain so for next decade too.