I started this portfolio since 2020 and I was buying stocks without understanding business or its results. I got lucky in with some (like M&M and Bajaj Finserve) so I still have them. rest I cleaned up in last one year.

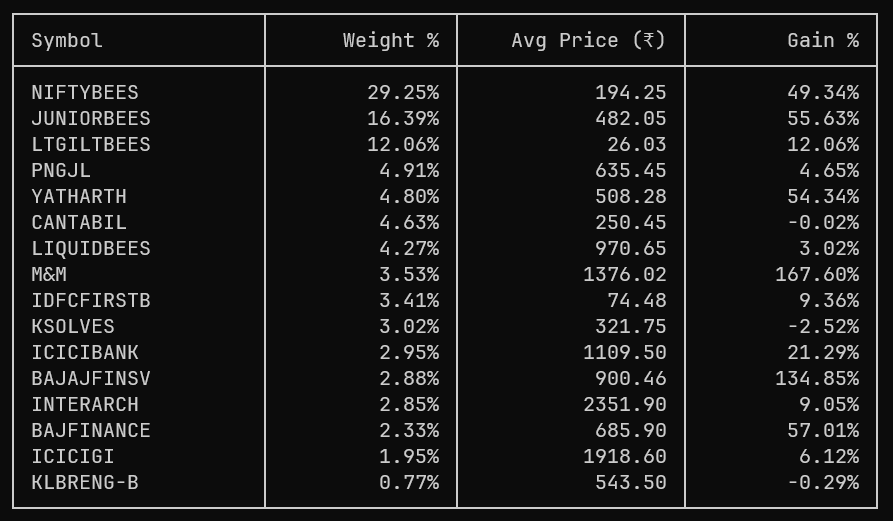

Here’s my current portfolio. Aim is to catch growth companies at reasonable valuation and hold them thru their growth period. Return expectations is to beat the index by 5-10%.

NIFTYBEES and JUNIORBEES is a temporary place to park money. When I have conviction in an idea, I liquidate NIFTYBEES/JUNIORBEES and buy the stock.

I start with 1-2% once I start tracking, once convinced I deploy up to 4-5% on an individual stock.

| Instrument |

AverageBuy |

P&L% |

Portfolio Weight% |

| BAJAJFINSV |

900.46 |

131% |

3% |

| BAJFINANCE |

685.90 |

56% |

2% |

| CANTABIL |

253.50 |

-5% |

1% |

| ICICIBANK EVENT |

1,109.50 |

29% |

3% |

| ICICIGI |

1,918.60 |

4% |

2% |

| JUNIORBEES |

482.05 |

55% |

16% |

| KLBRENG-B |

543.50 |

3% |

1% |

| KSOLVES |

321.75 |

0% |

3% |

| LIQUIDBEES |

973.03 |

3% |

5% |

| LTGILTBEES |

26.03 |

12% |

12% |

| M&M |

1,376.02 |

165% |

3% |

| NIFTYBEES |

190.33 |

52% |

38% |

| PNGJL |

635.45 |

3% |

5% |

| YATHARTH |

508.28 |

60% |

5% |

I had another portfolio, which I have liquidated and used the money or invested in debt/equity mutual funds.

2 Likes

Using airtable to track ideas-

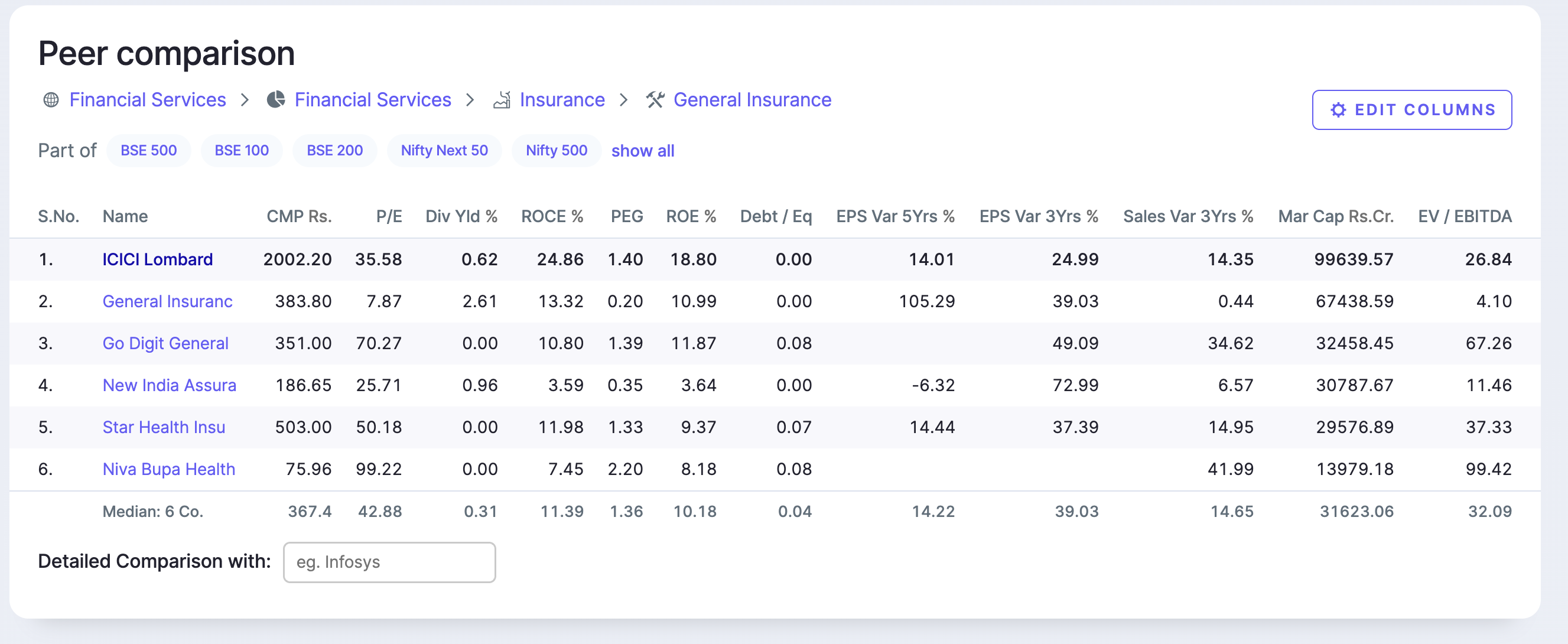

Review of recent investment ICICIGI.

Initial hypothesis, Solid growth in sales and profit, good ROE.

Lower valuation compared to peers-

Q2 Results-

Decent sales growth and good EPS growth

Financial performance

GDPI fell but PAT increased

I would like to see holistic growth starting from GDPI. I did not attend the concall so will wait for transcript.

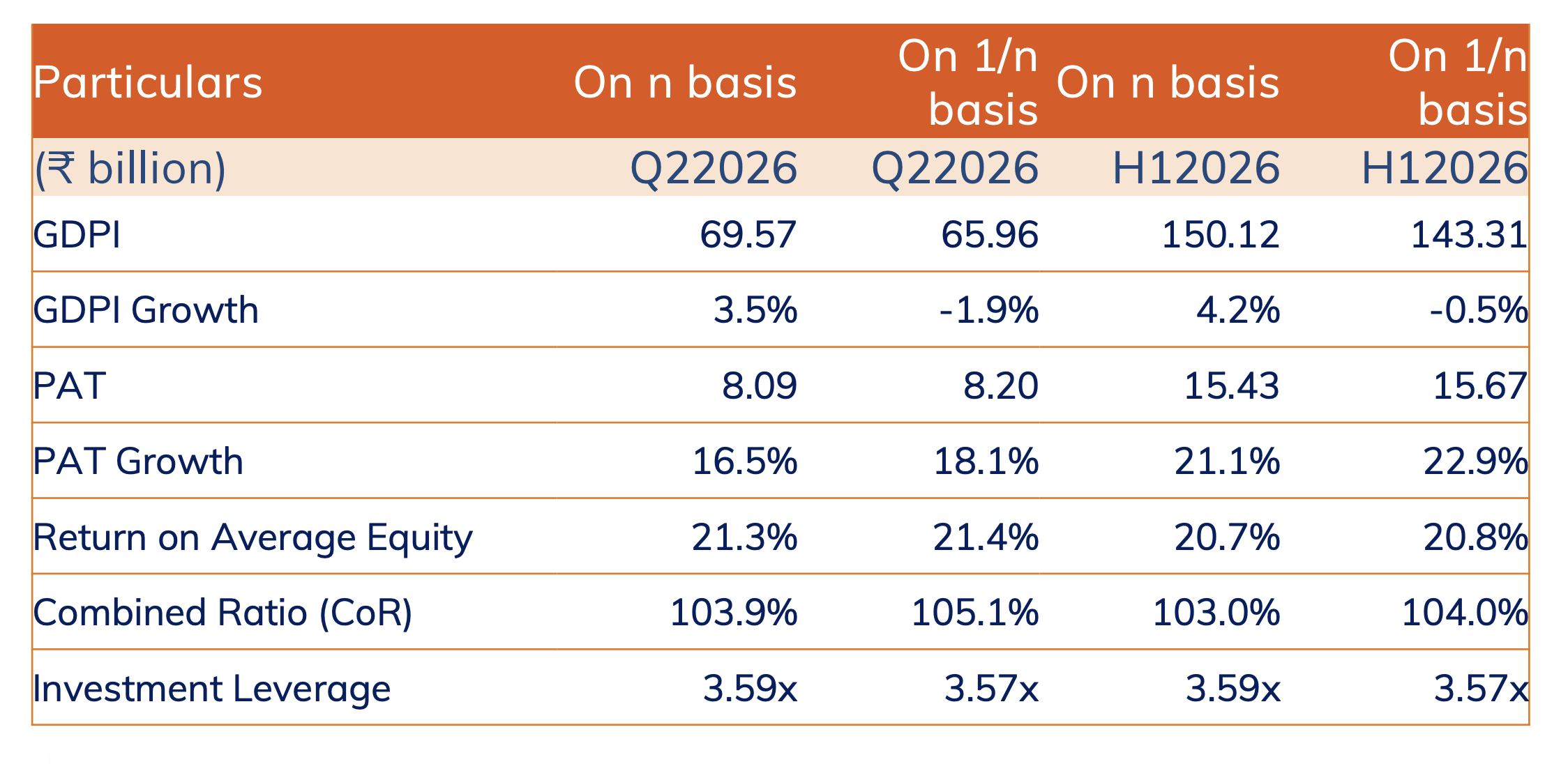

Update:

Management saying reason for lower GDPI growth is conscious effort to not chase unprofitable motor and crop sector. However the growth in their preferred segment (exc. crop and mass health) is 3.5% which is lower than industry growth 9.8%. Overall lower growth in GDPI will show in lower revenue and profit in coming quarter. So I will observe next quarter and if the GDPI growth is not even near Industry then stock will get beaten.

Source

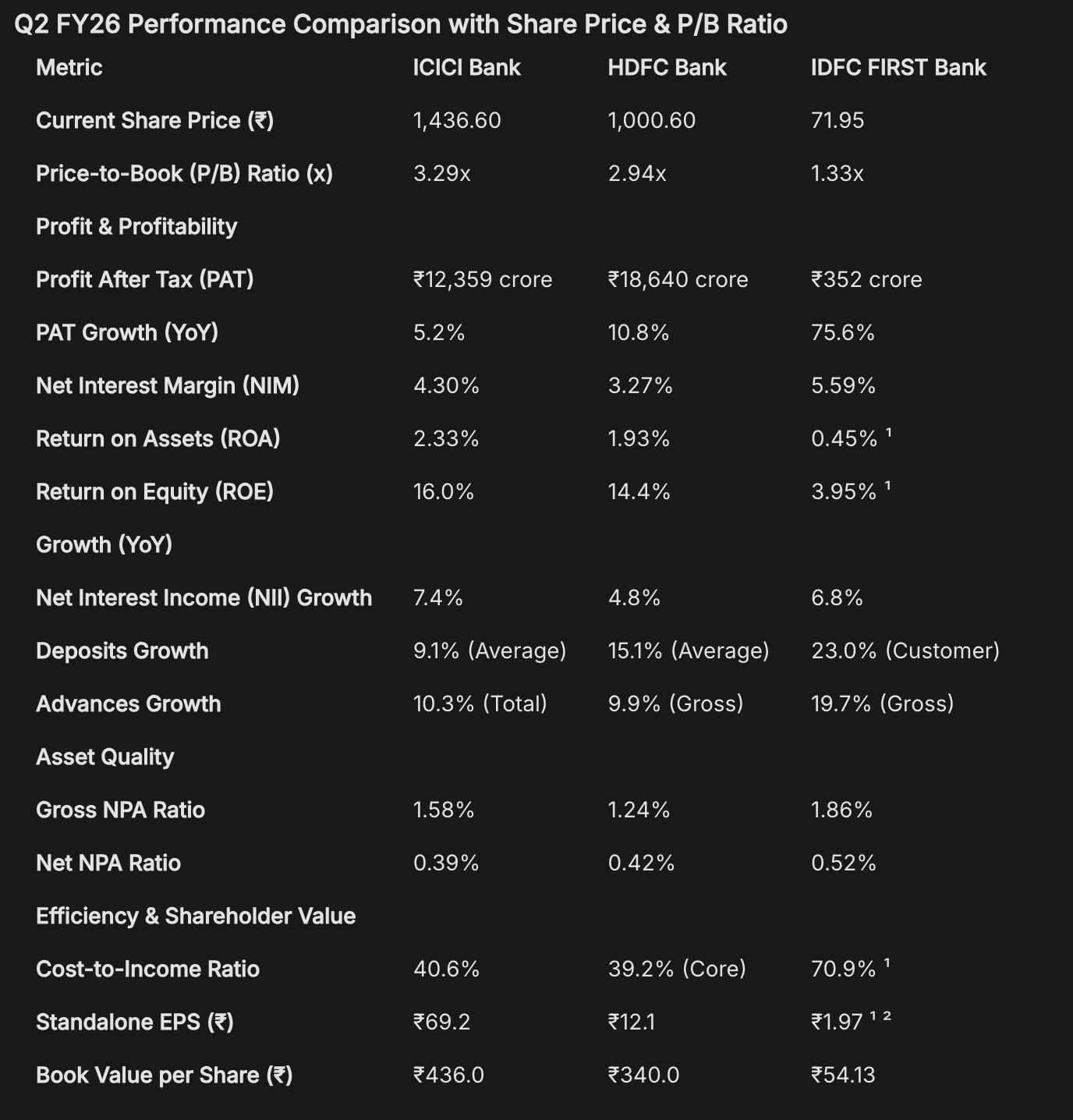

ICICI Q2 Review and comparison with HDFC and another smaller player IDFC First

Update:

Market did not like ICICI results (-3%), HDFC was strong initially but closed only 0.1% up. IDFC was up 6.9%. I was able to acquire IDFC at 72.75 and got a good head start. IDFC still looks good deal right now to add more.

I am still holding ICICI, I think it will still perform better than index in coming quarters.

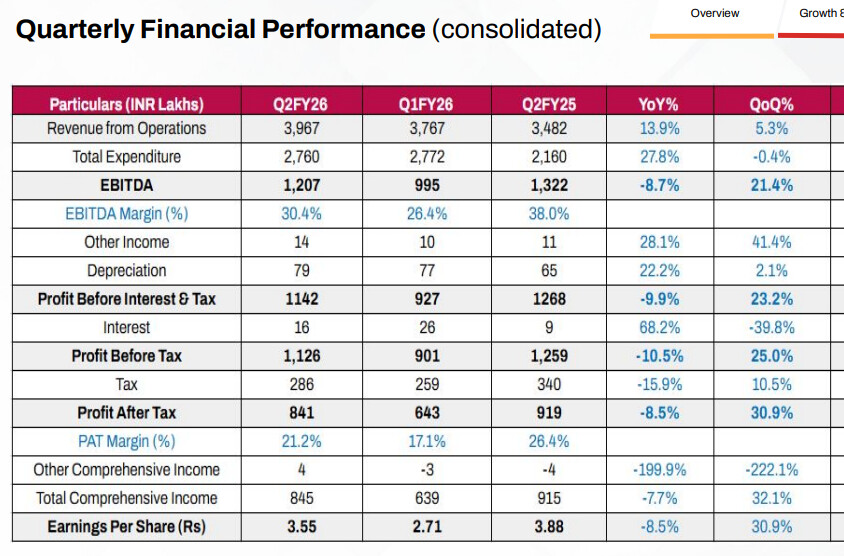

KSolves update

Quarterly growth looks to be back on track after a dip in FY Q1

Same resulting in EPS growth of 30.9% QoQ. Looks like they have started to get the operating leverage.

Will wait for transcript to see the guidance.

However only problem I have with them is, I expected more sales growth. Persistent even at this size is growing sales 23% YoY / 7.4% QoQ

Update from concall-

Guidance:

FY26 Revenue Growth Target: Management is confident in achieving 20% revenue growth for FY2

Confidence in Pipeline: Management currently has visibility into the pipeline and can see meetings with customers that make them optimistic about achieving the H2 target . However, they acknowledge that external factors, such as the US economic situation or other global events, could potentially change outcomes

Target Margin Range: Management states that the range they would like to keep is 25% to 30% minimum

Investment in Products: The company has initiated investment in product development, particularly in AI and Big Data. The IT product segment (which recorded ₹1.03 crores in Q2 revenue with a lower contribution margin) involves upfront development and marketing investment but provides long-term scalability potential. This investment dampens overall margins

Increased Standard Operating Costs: New standard expenses are now factored in, including the salary of a Salesforce director and expenses related to frequent travel by management and key colleagues (like the Chairman, CTO, and others) to meet hot leads and customers. These are considered necessary costs for business growth and sustainment

Reduction in Event Costs: Margins are expected to improve from previous quarters because the company has finished attending numerous costly industry events (approximately 10 this year). These kinds of huge event expenses will drastically reduce in the next year. Moving forward, the focus will shift to organic marketing and frequent travel to meet customers, which will be less expensive than the large events previously attended

With excellent Q2 results and this public research report I am adding

Interarch.

I have verified the report with Q1 results

Capacity expansion-

| Timeline (Quarter) |

Capacity (MT) |

Investment (₹ Cr) |

Location |

Phase/Type |

Remarks |

| Q2 FY26 |

35,000 |

Part of ₹53 Cr |

Andhra Pradesh |

Phase 2 |

Expansion of existing PEB plant |

| Q2 FY26 |

15,000 |

Part of ₹53 Cr |

Kichha, Uttarakhand |

New B* ox Column Line |

Enhancing structural capabilities |

| Q2 FY27 |

25,000 |

₹100 Cr |

Andhra Pradesh |

Phase 1 (New Plant) |

Greenfield project |

| FY28 |

40,000 |

~₹70 Cr |

Kheda, Gujarat |

Phase 1 (New Plant) |

New strategic location |

Healthy order book growth

- Order book growth of 25%

- As on Q1 FY26, its order book stood at ₹ 1695 crore (1.2x its FY25 revenues)

- 82% repeate orders

Revenue growth

- Q2 revenue grew at 52% YoY, exceeding their guidance of (20-25%)

OPM

- High Fixed Costs: Includes employee, sales, design, and project management costs — these remain relatively stable even as turnover increases.

- EBITDA Margin Expansion Drivers:

- Operating leverage from scaling

- Larger order ticket sizes

- Entry into export markets

- Launch of “heavy structure” vertical

- Profitability Estimates:

- EBITDA CAGR: 23%

- Net Profit CAGR: 20%

Finally net debt free balance sheet

Latest portfolio after recent IDFC first and Interarch purchage-

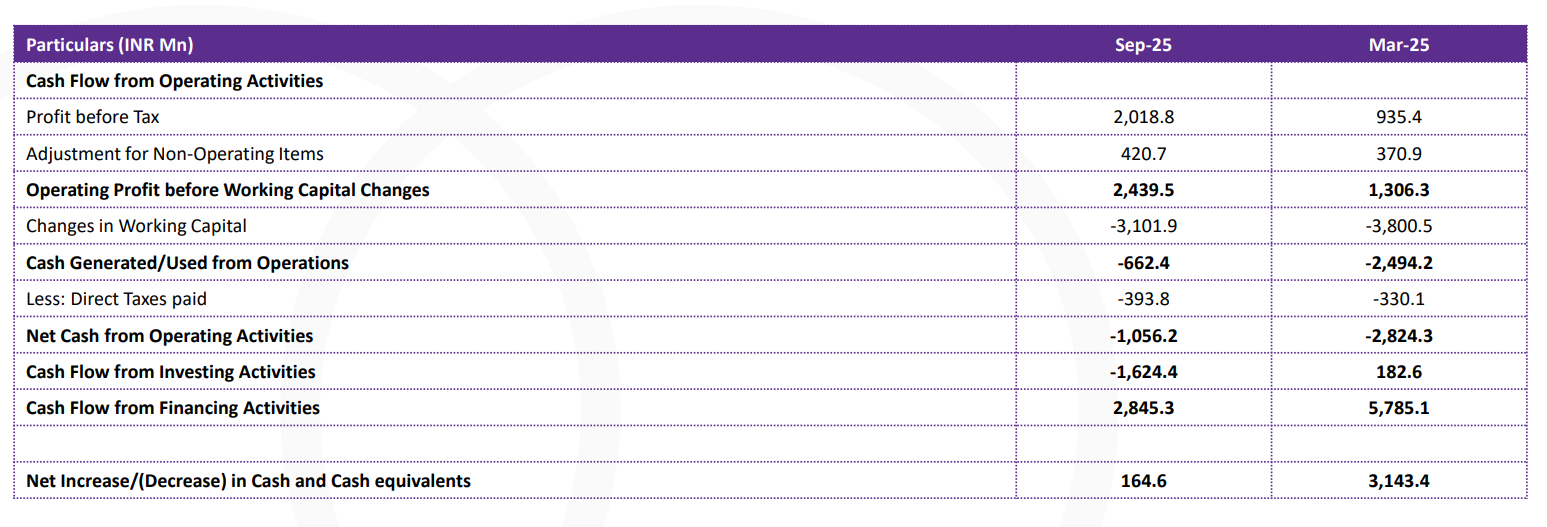

PNGJL result update-

Meets the guidance in terms of Store count, Revenue, PAT Margin guidance

Need to look out for growing Other Income, this might be interest on FD which is kept as collateral for Gold Metal Loan. Because this growing Other Income is also accompanied by growing

Cash and cash equivalents and

Other bank balances on asset side and increase in

Borrowings on liability side.

Further, Operating cash flow negative, probably due to inventory build up for Q3

Will update based on earnings call, overall result looks positive.

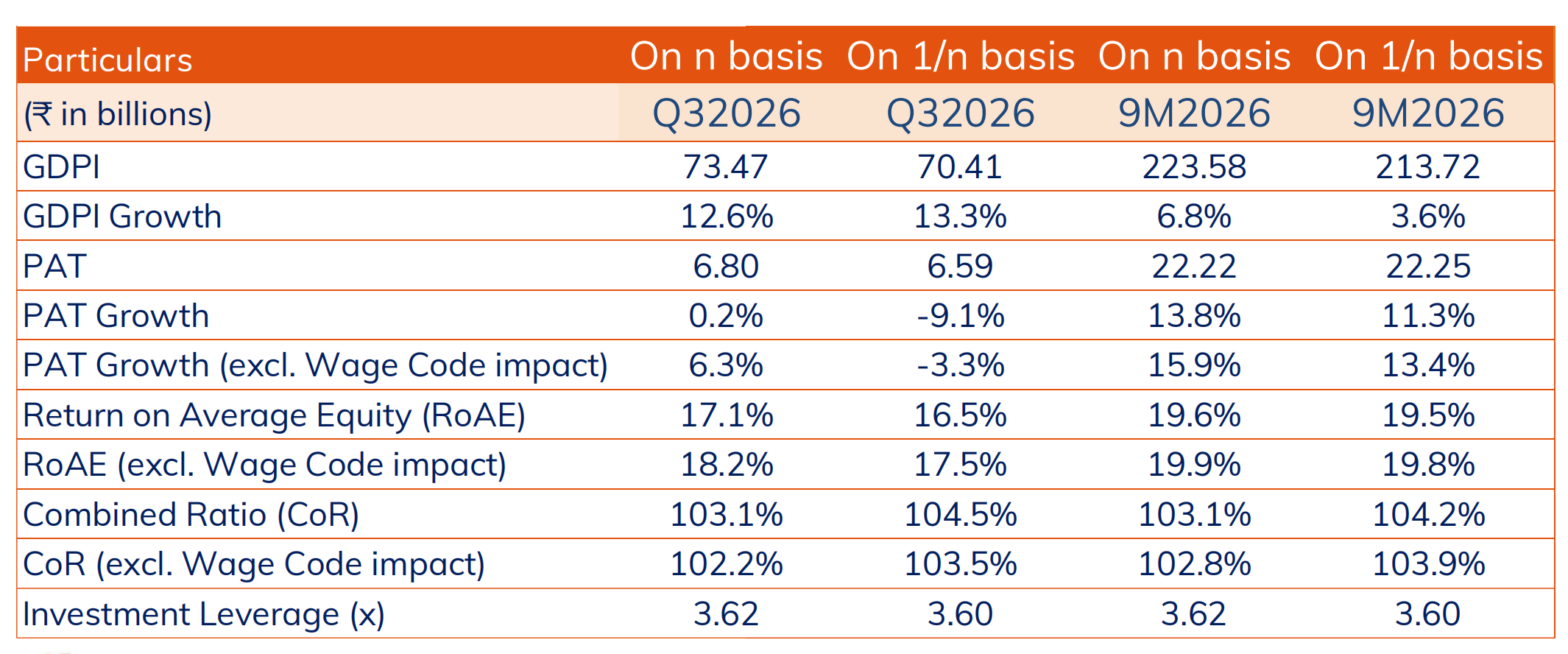

Q3 ICICIGI Performance-

Decent GDPI Growth, however all other metrics degrading

As per their earlier commentary, they are focussing heavily on Health, Travel & PA segment. Overall 40% growth in this segment. Awaiting earning call transcript.

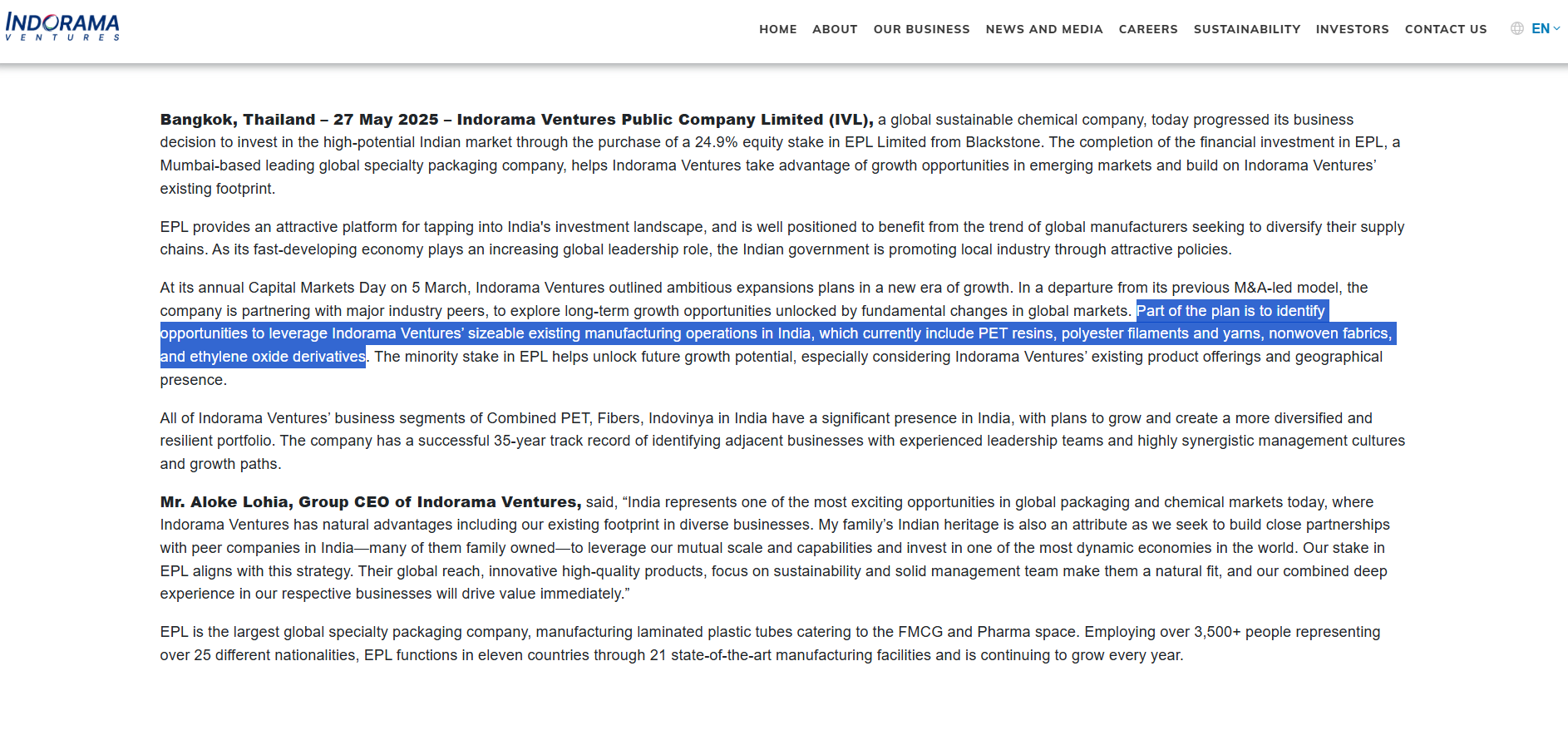

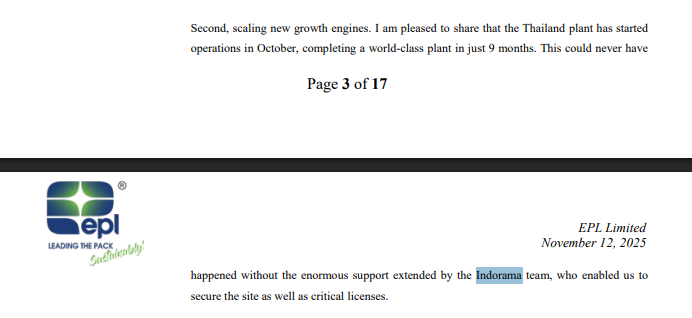

Recently added EPL at 213 rs based on this ICICI report. The business is well diversified across geographies, it has plants in US etc so it is some what unaffected by tariff situation. EPL also has shown consistent operating leverage and its looks very cheap at current valuation.

Watchouts:

- Promoter offloading stake - Blackstone has sold major percentage, however it is acquired by synergistic Indorama group. I dont see this as a bad thing, its just something I need to watchout for

- Change in CEO- Need to watchout how business performs under new CEO

EPL-ICICI.pdf (502.4 KB)

Promoters sold from 51% last year to ~26% this year. Why is this so?

The promoter is a private equity (BlackStone), by nature of their business, they turnaround a company and sell it eventually to another promoter, In this case Blackstone has not shared much in their announcement, it might be they want to payback their investors or they want to invest somewhere else while retaining control.. we can only speculate.

However the acquirer has shared their intent, Indorama wants to integrate itself into EPLs value chain, Also, in recent earning calls, CEO acknowledged Indorama team played key role in setting up factory in Thailand, so it looks like synergistic play.Announcement:

Earnings call transcript below-