Is thr an arbitrage here cosidering the price is 715 and Offer price is 745? My guess is that only 10% of the remaining shareholding will be acquired from public shareholders, but not sure how the tender works here, is it proportionate or not?

Rantac is regarded as number 1 brand in the market and Sales are increasing everyday currently scenario for 10 days - 1 lakh strip for Rantac in a designated part of Maharashtra are being sold. Not sure when it comes to other country/state wise.

Open offer at 745 per share less than current price

Sale to KKR is done… this was news from my friend in Mumbai (many people asked me about the sales of Rantac & sale of JB to KKR)

Sales are pretty good and till someone steps in with low NMDA then we might have to relook

good related post

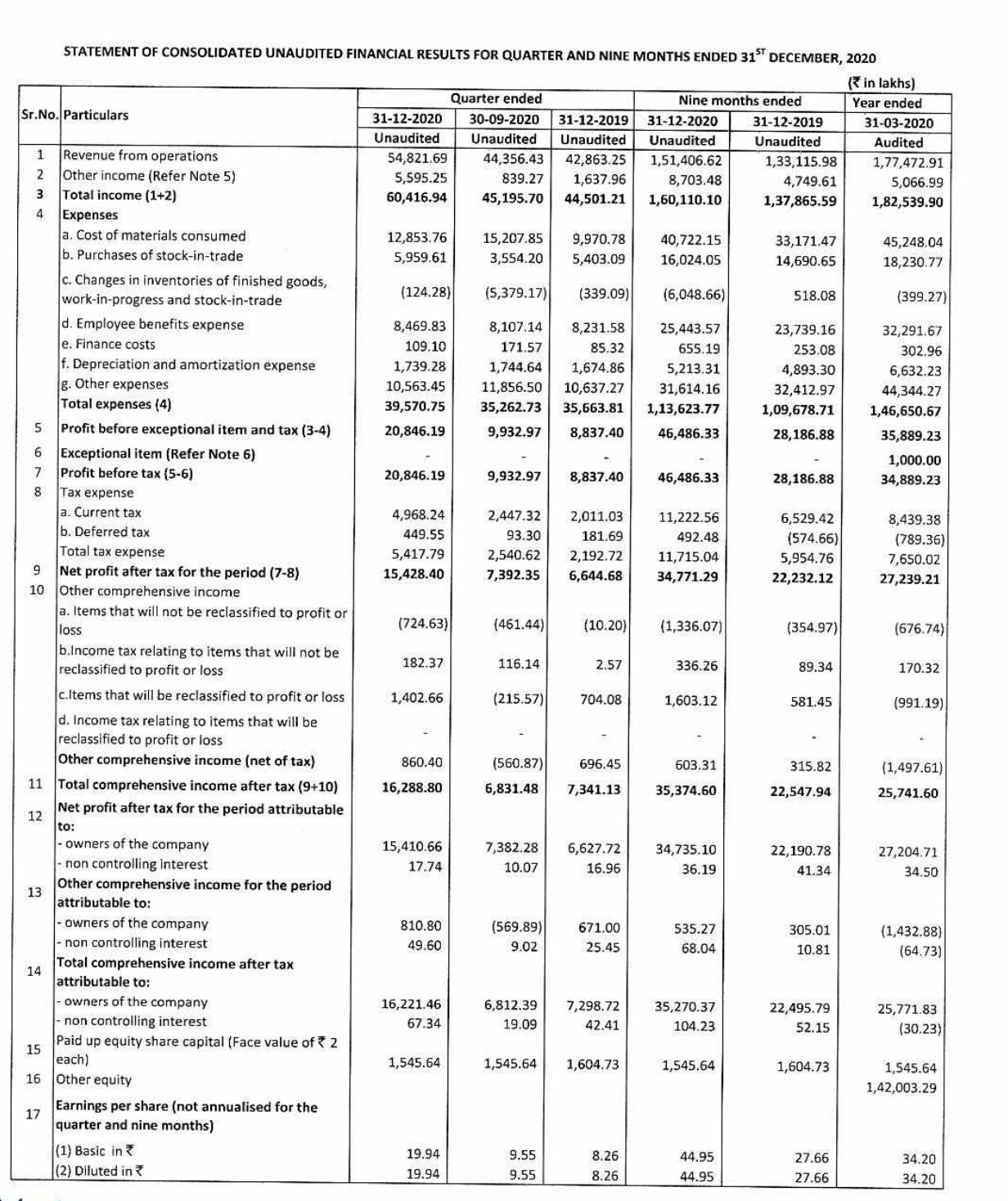

Fantastic Q1 results by JB chem. Revenue growth of 18% and EPS growth of 100%. Net profit growth is aided by reduction in other expenses by 10cr.

Like most pharma companies exports and API have contributed to growth.

Impressive part is their domestic formulation growth(despite Ranitidine issue) when most other companies were unable to grow domestic formulation business in Q1.

Domestic formulations growth is mainly lead by cardiac division(Cilacar and Nicardia). Going by few reports even during July and August month domestic formulation of JB chem is doing much better than industry. Last two years efforts of management to increase MR no and strengthening brands seems to be playing out well.

Another important brand Metrozyl (metronidazole) used to treat anaerobic infection and as part of peri-operative antibiotics , use of Metrozyl must have reduced significantly with postponement of elective surgeries during last quarter and should be improving going ahead. Price escalation of 50% for Metrozyl as allowed NPPA should play out with increasing sales in Q2 and subsequent quarter.

Discl: I have exited around 2/3rd my JB chem holding few weeks back missing the late rally

Amazing Numbers ,Other income boosted by 33.68 Crores from sale of one of their product registrations.

Even adjusting for that margins have expanded meaningfully.

Interim Dividend of Rs 8.5 per share declared.

1 Like

Some revenues have spilled over from Q2 to Q3 which has also contributed to margin expansion as per management.

Press release:

Investor Presentation:

Detailed investor presentation and management interaction:

3 Likes

JB chem entered nephrology segment with new dedicated division Renova.

Seven products will be launched in this division. It will be interesting to see what new products will be launched in addition to existing antihypertensive medications.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/31659473-d5f9-4426-b614-02dd8303897c.pdf

1 Like

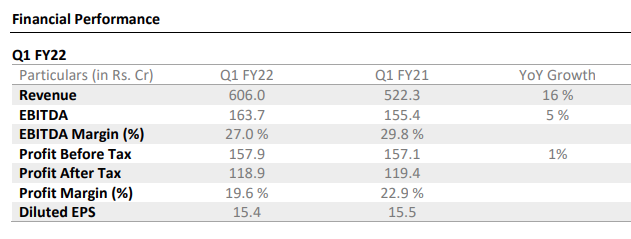

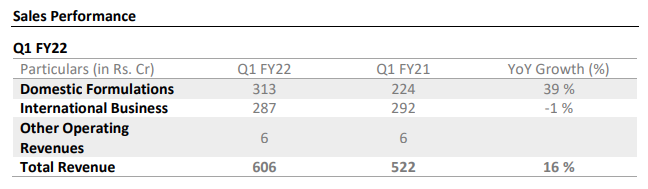

JB Chem & Pharma Q1 FY22 Results review

Revenue growth of 16 % to Rs. 606 crores for Q1 FY22

Profit After Tax was flat at Rs. 118.9 crores for Q1 FY22

Domestic Formulations Business update

Launched a new dedicated division RENOVA to cater to the needs of Chronic Kidney

Disease patients in the country

During the quarter, the company also launched the NOVA division, which will focus on

pediatric and respiratory segment in India

International Business update

Uncertainty surrounding second wave of COVID-19 in certain international geographies

impacted revenue growth for the International business

USA and South Africa business continues to show strong momentum with growth in

excess of 20% respectively for the first quarter

Despite muted cough and cold season Russia CIS has seen gradual growth revival during

the quarter

API business remained challenging for Q1 FY 22. However, the business is now showing a

good trend and a healthy order book

4 Likes

Another good quarter from JBC.

Revenue 606 Cr up 15 % vs 528 Q4 and 522 Q1’21

PAT is flat 119 Cr vs 100 Q4 and 119 Q1’21, Other income was lower than the 2 corresponding quarters due t lower bond yields.

EBITDA margins are lower at 27 %, with increased travel and sales promotion activities compared to last year (29.8%), but better than Q4 (23.4%).

Employee costs have increased. They have also implemented an ESOP scheme which will also cost about 50 Cr/year.

Revenue growth was from India, their power brands like Metrogyl and Rantac are doing well. Projected growth is ~15 %.

Exports were down slightly. Management expects better traction in exports going forward, with projected growth in low Double digits.

Investing in technology to boost MR productivity in existing divisions, and also adding MRs for the Nephrology, Respiratory businesses.

Disc: Invested and holding since a long time.

Valuations have gone up from typical 10- 15 PE band to about 25-30 PE now, due to the recent price run up. Longer term, I believe JBC is still a very promising play in the Pharma space, and would add on corrections if any.

3 Likes

A good insight on what to expect post the acquisition by KKR.

2 Likes

2 Likes

AR notes iro JB Chemicals and Pharma for FY 2021-22 -

- KKR ( PE firm ) holds controlling stake in the firm. Company has 07 state of the art manufacturing units in Gujarat. Currently ranked 28th ( up from 32 in last year ) in IPM with 05 brands in top 300. These are -

Rantac ( to treat indigestion, heart burn, acid reflux)

Metrogyl ( antibiotic for parasitic infections )

Nicardia ( to treat high BP )

Cilacar ( to treat high BP )

Cilacar T ( to treat high BP )

- Core therapy segments - Hypertension, Gastroenterology, Nephrology, Cardiology, Dentistry and Paediatrics. In FY 21, realigned our structure and portfolio to ensure focus on lifecycle management of flagship brands. Next priority is to scale up R&D and business development towards building a progressive portfolio in US, SA,Russia, SA, API and CMO business.

- New products / therapies entered -

Introduced new products in Nephrology

Entered - Respiratory, Diabetic categories

Introduced - Lozenges as Nicotine replacement therapies named - NOSMOK lozenges

- Actively exploring possible M&A opportunities which can complement our strengths and accelerate our performance in key segments.

- Third largest lozenges manufacturing capability globally. Already exporting to 30 countries. A leading partner of choice for MNCs. Can make lozenges of all shapes and various flavours.

- Last 5 yrs Operating revenue and EBITDA -

Revenues - 1200cr, 1255cr, 1501cr, 1641cr, 1892cr

EBITDA - 222cr, 203cr, 288cr, 368cr, 556cr

EBITDA margins (%) - 19, 16, 19, 22, 29 percent … Last 02 Qtrs margins have been at 25 pc

ROCE (%) - 17, 14, 22, 28, 42 percent

Cash holdings on 31 Mar 21 - aprox 700 cr. As on 30 Sep, Cash holdings are north of 800 cr

- India business - Share of chronic therapies in India has expanded from 31 to 36 pc in last 5 yrs. Same is expected to go even further. Same is expected to continue due better diagnosis and compliance on the part of patients. Poor lifestyles, obesity and poor eating habits are also contributing to this trend. Key enablers for the company remain- awareness programs and penetration in Tier II and III mkts. During the year, domestic formulations sales stood at 840 cr. Company is currently employing a sales force of > 2100 MRs. Contrast media product sales of the company stood at 53 cr, down 14 pc due deferral in electives.

-

International business - Operates different models in different countries with direct presence in SA and Russia. Has distributor relationships in US and various other countries across LATAM, Africa and Asia. Company also has good CMO operations. Overall formulations exports stood at 1007 cr, up 19 pc yoy.

SA sales at 218 cr, API sales 83 cr, Russia sales at 61 cr, Ukraine and CIS countries sales at 68 cr.

Disc : invested, biased.

5 Likes

Management is walking the talk. Very positive development in my view.

Disc: invested

5 Likes

JB CHEM board approved the trademark assignment of Azmarda brand from Novartis for 246cr.

Revenue for the brand Azmarda over last 3 yrs:

FY20: 43 cr

FY21: 58 cr

FY22: 72 cr (till Feb 22).

Assuming 80cr of revenue for full FY, JB has paid roughly 3 times the revenue.

Azmarda brand is a patented product composed of Valsartan and Sacubitril.

Combination of Valsartan and sacubitril is indicated in chronic heart failure patients with reduced ejection fraction.

Use of the above combination is increasing across the world as randomized controlled studies have shown reduced mortality and hospitalization in patients having chronic heart failure with reduced ejection fraction. From 2016 it’s been included in major cardiology society (EU and AMERICAN) guidelines as a strong recommendation for use. Practically I have seen more and more cardiologists prescribing it.

Vymada is the preferred brand used by many.

Azmarda and Cidmus are the same combination of drugs marketed as ?co-brands (of Vymada) by Cipla and Lupin respectively.

Few days back Dr Reddy lab has done an agreement with Novartis for trademark assignment of Cidmus brand at around Rs 450cr ( sales of Cidmus was 136 cr for last 12 months…cost of acquisition around 3 times the revenue).

Simple search on e-pharmacy stores shows other players like Natco,Eris also marketing the generic branded version at a lesser price.

This acquisition should fit very well for JB Chem considering their strong formulation cardiology segment focusing on chronic therapies.

discl: tracking

7 Likes

JBC Q4 Results

Decent results, revenues have grown, but profits lower on higher material/transport costs and an acquisition made in Q4.

- YoY growth for Q4: Revenue + 18 % (Domestic +30 %, International +9%), EBITDA +20%, PAT -16%

- FY22 vs 21 : Revenue + 19 %, EBITDA +8%, PAT -14%

- JBC is the fastest growing among top 30 IPM companies in Q4 FY22, and IPM ranking over the past 12 months has improved from from #32 to #25

- Monthly Revenue Per Rep: PCPM is INR 5.6L for FY22, up from INR 4.4L in FY21, expect 12-14 % productivity improvement annually

- Chronic Therapies 50 % vs 46 % last year, and projected to be 54 % after Azmarda integration.

- New Products Fy22: 17 launches contributing 4 % of revenues, compared to 5 launches with 1.4 % revenue in Fy21

Inv PPT :

Disc: Invested and holding.

3 Likes