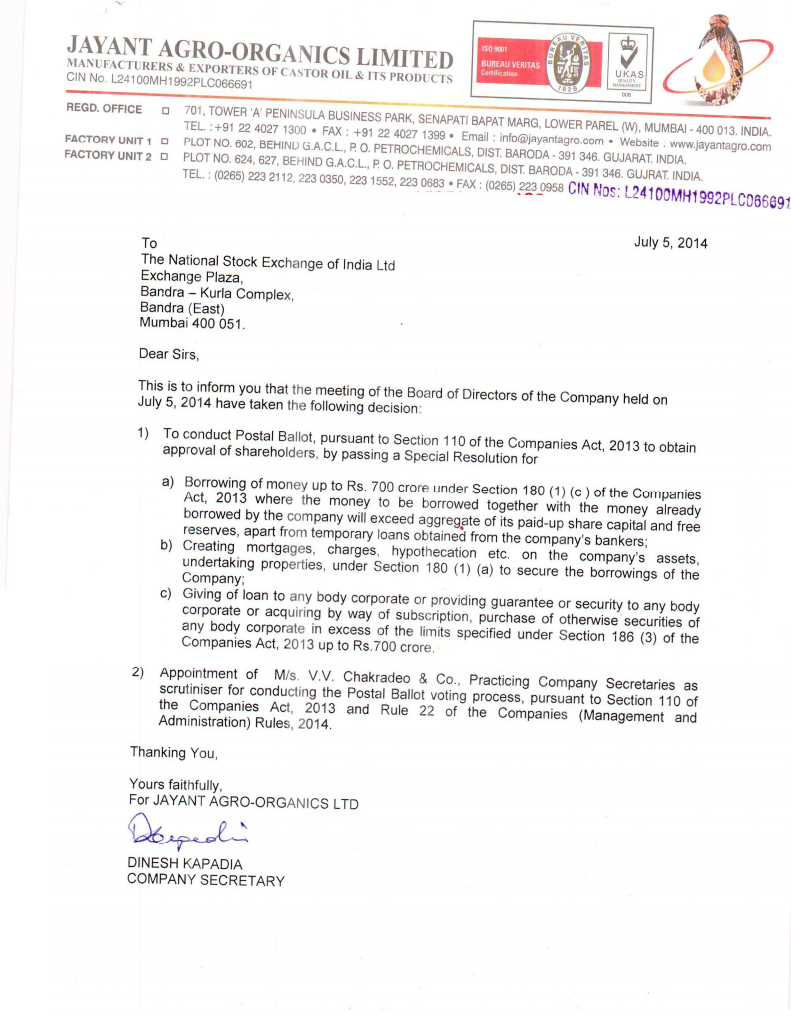

Jayant Agro on July 5,2014 had a board meeting and is now asking for Shareholder Approval for Special Resolutions.

a) Borrowing of money up to Rs. 700 Crore under Section 180 (1) © of the Companies Act, 2013 where the money to be borrowed together with the money already borrowed by the company will exceed aggregate of its paid-up share capital and free reserves, apart from temporary loans obtained from the Companyas bankers;

b)Creating mortgages, charges, hypothecation etc. on the Companyas assets, undertaking properties, under Section 180 (1) (a) to secure the borrowings of the Company.

c)Giving of loan to anybody corporate or providing guarantee or security to any body corporate or acquiring by way of subscription, purchase of otherwise securities of any body corporate in excess of the limits specified under Section 186 (3) of the Companies Act, 2013 up to Rs. 700 Crore.

=====

First glance it looks like company is looking at borrowing 700cr well above its reserve levels hence the postal ballot…

Digging deeper if you look at Point (b)

b)Creating mortgages, charges, hypothecation etc. on the Companyas assets, undertaking properties, under Section 180 (1) (a) to secure the borrowings of the Company.

now Section 180(1)(a) for which the company is asking for shareholder approval … the Company Act 2013 Section 180(1)(a) states…

180). (1) The Board of Directors of a company shall exercise the following powers only with the consent of the company by a special resolution, namely:a

(a) to sell, lease or otherwise dispose of the whole or substantially the whole of the undertaking of the company or where the company owns more than one undertaking,of the whole or substantially the whole of any of such undertakings

Explanation.aFor the purposes of this clause,a

(i) aundertakinga shall mean an undertaking in which the investment of the company exceeds twenty per cent. of its net worth as per the audited balance sheet of the preceding financial year or an undertaking which generates twenty per cent. of the total income of the company during the previous financial year;

(ii) the expression asubstantially the whole of the undertakinga in any financial year shall mean twenty percent. or more of the value of the undertaking as per the audited balance sheet of the preceding financial year;

Reading the section 180(1)(a) of the company act indicates that company is looking at substantial asset sale worth 700Cr but has watered down the Section 180(1)(a) and reworded it to sound like a 700cr loan… (creative writing and thinking…)

My understanding is that Arkema (French 7 billion Euro sales Speciality chemical giant and largest consumer of castor oil and castor oil derivatives in the world) would like to have majority stake to ensure they can call the shots in Ihsedu Agro Chem. Ihsedu Agro chem is located in banaskantha district, gujarat and Banaskantha district produces 200,000 Metric Tonnes of castor which equals to 2nd largest castor growing country’s castor production (China)

This special situations postal ballot approval for 700Cr is nothing but a stake sale in Ihsedu agrochem…

Ihsedu Agro Chem March 2013

Sales: 885Cr

PBDIT: 24.8Cr

PAT:8.5Cr

Dividend payout: 4.96Cr

Jayant agro stake in ihsedu agrochem : 75.1%

Arkema Stake in ihsedu agrochem: 24.9%

Postal ballot

http://www.moneycontrol.com/livefeed_pdf/Jul2014/Jayant%20Agro_753.pdf

Company act 2013:

http://indiacode.nic.in/acts-in-pdf/182013.pdf

Would like to get views from other investors/boarders… if my interpretation of Jayant agro Postal ballot holds some water …

if the news of 700Cr stake sale is true the stock price could react positively by a huge number as current market cap of Jayant Agro Organics is just 180Cr

Sept 27,2014 is the AGM Date … I am assuming the sale will be finalized before the AGM else there could a lot of questions to answer about 700cr loan in the AGM… also stake sale would result in an AGM “Party”!!

{kind=link}

{kind=link}

{kind=link}