JASH Order book updates

2 Likes

This order book shows about ~61 crores of execution in the month of January which is almost >50% YoY increase (comparing only January month data) and given this month contributes historically around 15-20% of the last quarter total revenue, This quarter numbers could be around Rs. 300 crores and may be more if the trend persist. If this is so, then This will beat company’s yearly guidance by more than 15%.

Disc - Invested

4 Likes

At first glance looks like excellent results ![]() Though my maths of around 200 crores fell short

Though my maths of around 200 crores fell short ![]() but in hindsight it seems that closing year around 700 crores top line can still be a reality.

but in hindsight it seems that closing year around 700 crores top line can still be a reality.

Also, the PAT can also end up being upwards of 100 crore easily.

A very robust order book should set the business rolling for next year as well coupled with added capacity. Exciting times ahead ![]()

The PAT growth is even higher ![]() & close to 50%.

& close to 50%.

OUTCOMEJASHFEB2025_12022025151847.pdf (2.5 MB)

Disc: Invested & biased. Have added recently as well. No recommendation

6 Likes

Revenue outlook of 675 Cr for FY 25.

As March Quarter of this company has always good,

Hence minimum 239 Cr revenue for the March Qtr seems easily achievable (10-12% YoY Growth), to achieve Revenue outlook of 675 Cr for FY 25.

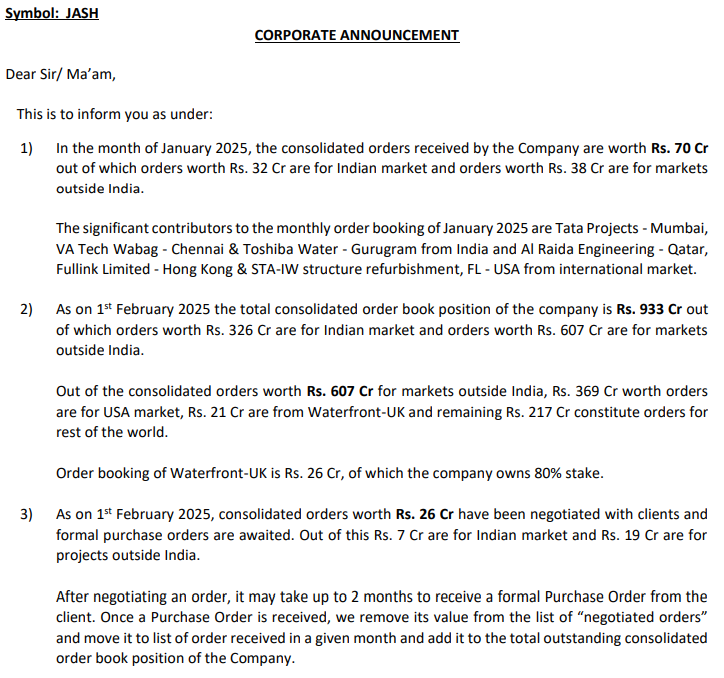

As on 1st January 2025 the total consolidated order book position of the company is Rs. 924 Cr

out of which orders worth Rs. 320 Cr are for Indian market and orders worth Rs. 604 Cr are for

markets outside India.

Disc: No Buy or Sell Recommendation.

7 Likes

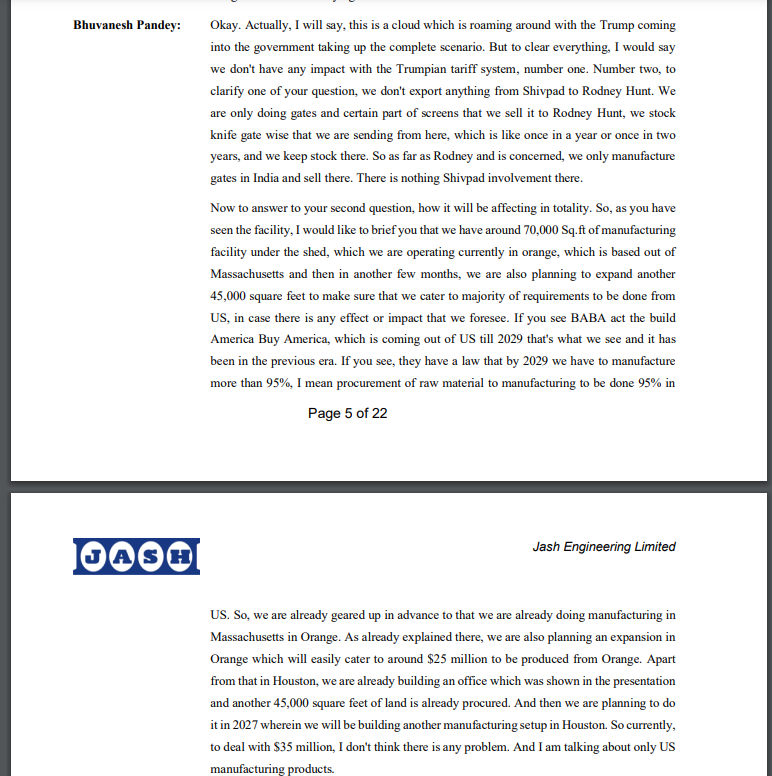

Can jash be impacted by reciprocal tariffs, as per my knowledge India imposes 25% BCD on 73089090 (this is the HSN code through which jash exports) and similarly, USA imposes zero duty on this goods, do this means lower margins for jash going forward?

View invited.

Disc - Invested

1 Like

One peculiar thing is that the imports coming from USA under this HSN is hardly 4% of the total imports, this might not be a material/too much to think for them to put a reciprocal tariff may be.

They have clarified this in the con call.

Link to concall of Q3FY25 - https://nsearchives.nseindia.com/corporate/JASH_19022025111929_CALLTRANSCRIPT13022025.pdf

9 Likes

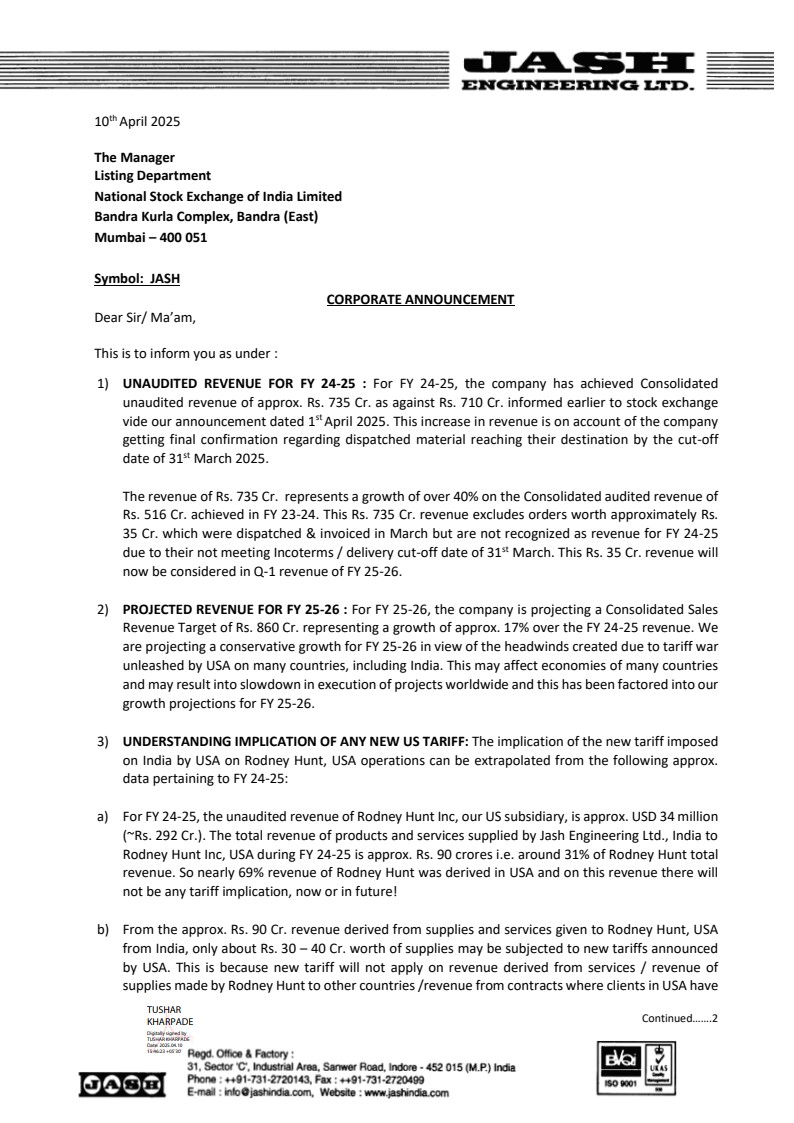

And they’ve done it ![]() Unaudited numbers of 710 crores announced by the company. What an excellent closing

Unaudited numbers of 710 crores announced by the company. What an excellent closing ![]()

Plus company is hopeful to achieve 1000 crores in FY 26-27.

Invested & biased

11 Likes

One of the finest mgmt ![]()

5 Likes

Excellent, Excellent, Excellent. What a grand year ![]()

Congratulations to everyone. 735 crores is out of the park ![]()

Also, what’s heartening is that sales projection is done basis considering the Tariff war & slowdown.

Whatever be the case, reaching 1000 crores a year earlier than earlier timeline, is a testimony of management capability in taking advantage of the long tailwinds.

10 Likes

Order book of 808 crores. Something to worry?

1 Like

Order book ₹ 825 crores at the end of this financial year was committed during Q3 FY 25

.

Order Book as on 01.04.25 is 808 Cr excludes orders worth approximately Rs. 35 Cr. which were dispatched & invoiced in March but not recognized as revenue for FY 24-25 due to not meeting Incoterms.

Commitments are in Line.

Disc: No Buy or Sell recommendation (Position-Holding the Stock)

2 Likes

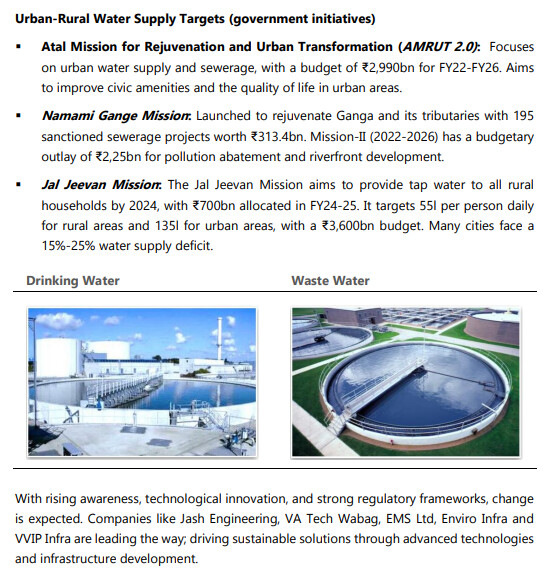

What would be the impact of significant reducing government budget on jal jeewan mission on jash eng?? Although it’s majority of buisness comes from export but I think good chunks also comes from jal jeewan mission, if someone put light on?? About how much order book impact by jal jeewan mission??

https://nsearchives.nseindia.com/corporate/JASH_05052025174943_OUTCOMEJASH05052025.pdf

Results out.

GP have taken a huge hit, despite stable raw material prices,

Any view?

3 Likes

Management should be able to address this tomorrow. Quite unexpected. Could be that certain legacy orders at low margin would’ve been fulfilled & possibly it could be really big ones since revenue growth in Q4 was also very surprising.

Disc: Biased & no recommendation

4 Likes

POSITIVES

![]() Strong Revenue Growth & Global Expansion

Strong Revenue Growth & Global Expansion

• Company grew revenue at a CAGR of 21% over 7–8 years and market cap grew from INR 170 Cr in FY17 to INR 3500 Cr in FY25 – CAGR of ~47%.

• Export Contribution: ~60% of total turnover.

• Market spread is balanced: 37% India, 40% America, remaining in RoW.

![]() Segment Performance

Segment Performance

• Jash Standalone: Revenue ↑ 37%, PAT ↑ 38%

• Shivpad: Revenue ↑ 118%, PAT ↑ 251% – Strong PAT margin expansion

• Rodney Hunt: Revenue ↑ 29%, though margin was weak, PAT still ↑ 9%

• Waterfront: Turnaround in progress; losses are strategic investments for future returns.

![]() Healthy Order Book

Healthy Order Book

• Consolidated order book: INR 838 Cr

• INR 546 Cr – Outside India,INR 292 Cr – Domestic

• May pipeline: INR 59 Cr in negotiation, with 78 Cr potential orders.

• Guidance for FY26: Revenue target of INR 860 Cr, with potential upside to INR 900–950 Cr based on execution clarity.

![]() Margin Guidance & Profitability Strategy

Margin Guidance & Profitability Strategy

• PAT guidance for FY26: 12–14%

• EBITDA guidance: 21–24%

• Focus on improving Rodney Hunt margins and breaking even at Waterfront.

![]() Strategic Investments & Capex

Strategic Investments & Capex

- India:

• INR 2 Mn capex in Pithampur

• Chennai plant to be commissioned soon with potential revenue of INR 120–150 Cr over 2–3 years.

- USA:

• USD 4.5 Mn invested in Houston office and plant.

• Target to mitigate manpower issues faced in Orange area.

![]() Calculated Risk-Taking

Calculated Risk-Taking

• Management accepted loss-making orders strategically (e.g., Rs 50 Cr Tata Nuclear project) to:

• Prove execution capability to marquee clients like NPCIL, L&T, Tata Projects

• Gain future high-margin opportunities.

![]() Diversified Product Portfolio

Diversified Product Portfolio

• Top segments: Water control gates, screening equipment, valves, hydropower, process equipment.

• Operating in both discrete & large-size manufacturing (e.g., custom gates worth INR 2.5 Cr each).

![]() Talent Strategy

Talent Strategy

• Employee ramp-up at Waterfront from 11 to 18, targeting revenue scale-up to INR 50–60 Cr.

• Strong focus on building local teams in US/Europe to reduce visa dependency.

NEGATIVES & CHALLENGES

![]() Margin Compression

Margin Compression

• Despite revenue growth, EBITDA ↓ 2% and PAT ↓ 1% YoY.

• Decline driven by:

• Execution of low-margin projects (Tata, Suez)

• Stress on gross margins from ~800 bps drop in Q4.

![]() Project Execution Issues

Project Execution Issues

• Kansas Project (Rodney Hunt): Delays due to manpower shortage led to PAT margin drop. Management decided not to bid for Manhattan project to avoid repetition.

• Execution Stress Orders: Projects like Kansas and Tata expected to complete in Q1/Q2 FY26.

![]() Inventory Buildup & Working Capital

Inventory Buildup & Working Capital

• Sharp change in inventory: Rs 28.7 Cr vs Rs 4.86 Cr YoY.

• Result of build-up for high project deliveries & execution delays.

• Working capital cycle extended (~150+ days), primarily in export business.

![]() Manpower & Visa Constraints

Manpower & Visa Constraints

• Severe manpower shortage in Orange (US); current workforce aged 55–70.

• Visa constraints make it hard to shift Indian workforce to the US for manufacturing roles.

• Expansion into Houston planned to counteract this.

![]() Desalination Market Entry Slow

Desalination Market Entry Slow

• Despite potential, desalination market is tough to penetrate.

• Efforts ongoing, including partnership explorations with global leaders like IDE from Israel.

![]() Risk from US Tariffs & Global Politics

Risk from US Tariffs & Global Politics

• Potential Rs 8–10 Cr tariff impact if trade tariffs proceed as expected.

• Vulnerability to geopolitical tensions in China-Taiwan, India-Pakistan, and the Middle East.

![]() One-Time Losses Impacted Profits

One-Time Losses Impacted Profits

• Loss of ~INR 5 Cr from Waterfront investment.

• Management clarified this was a one-off and not a recurring strategy,even or deliver modest profit even in Q1 despite seasonal softness

11 Likes

Going by the latest commentary, it seems company will grow annually around 15% for the next 2 years. Order book seems to be around 1.25X of sales, which doesn’t provide much buffer incase if few orders face challenges. Seems fairly valued at current price, it will be hard to surpass PE of 25-30 unless the grow 20%+.

Unsure if any big investors have checked in.

Disclosure - Invested around 341 level.

My humble take & it comes from bias - Jash Engineering had a stellar FY25 & they had really surprised everyone although it included a bit of shock when it came to Q4 margins, the reasons of which were well explained in the call.

The management of Jash is a very conservative management & when they gave guidance for FY26 they’ve clearly stated that they can do 900 crores plus. We all know the geopolitical situation but one silver line is that Jash actually told that domestic demand & business is looking very good.

Now if one zooms out, then their investment plans in Saudi, the potential for margins to revert to the norm( they don’t have many loss making orders now), plus tariff situation actually not being that bad, it could be very likely that on revenue front we could see 860-900 crores of business. But what could actually be the ace is that PAT growth could easily end up 30% or more so, if things don’t turn very ugly. And if they do then horizons change then we might regret not wearing the bear hat all this while

Disc: This is solely my view & no reco.

4 Likes