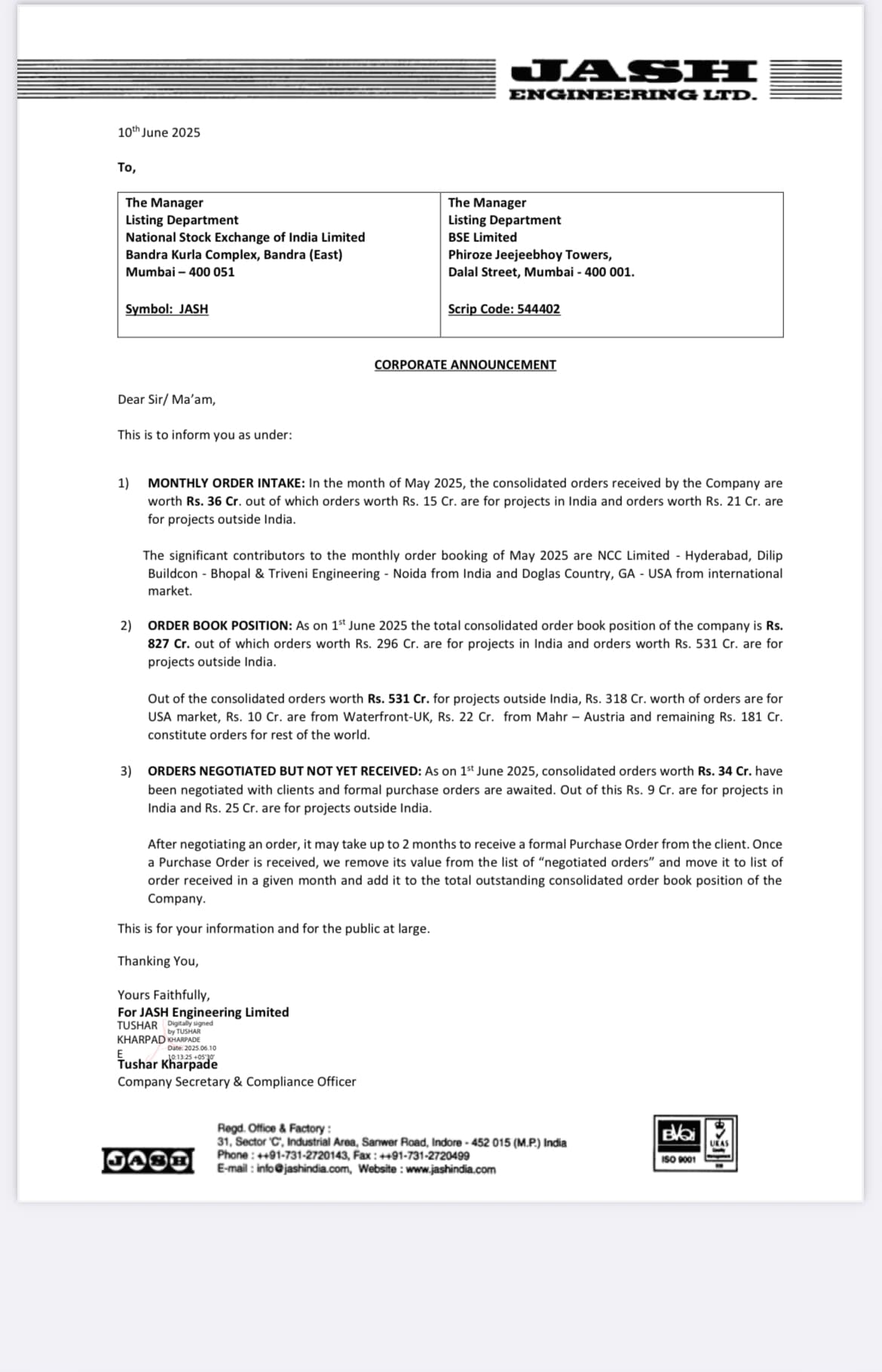

Though very early signs but April & May order inflow looks subdued. H1 shouldn’t get impacted much but it’ll be very important to see order inflows in next couple of months to see if there’s any turbulence. They could very well define the course of this year revenue estimates

Disc: No investment advise & biased