All Financial Data available in Screener.in.

Jash is listed in NSE only and all financials are uploaded by the company in NSE - So if you check in BSE no data is there.

2 Likes

First of all simplywallstreet is simply bull*hit .They have machine generated dumb articles on every share you can search for .Its much better to look at screener at the raw data and draw your own conclusions rather that forming wrong ideas based on simplywallstreet .

The reduction in promoter holdings is due to recategorisation of some inactive promoters to public category . Off course this makes them free to sell their stake but it also needs SEBI approval for the recategorisation ,so it’s not really a red flag .

8 Likes

Both the points make sense. And thank you so much for the clarity. Appreciated

1 Like

My thoughts on Jash Engineering and how the business is poised. Hope it adds value to the thread.

Disclaimer: Invested heavily in the stock and hence can be biased.

8 Likes

Just to let you know, promoter is not interested selling products in India…given the long delayed projects in India…he explicitly called it in concalls…

2 Likes

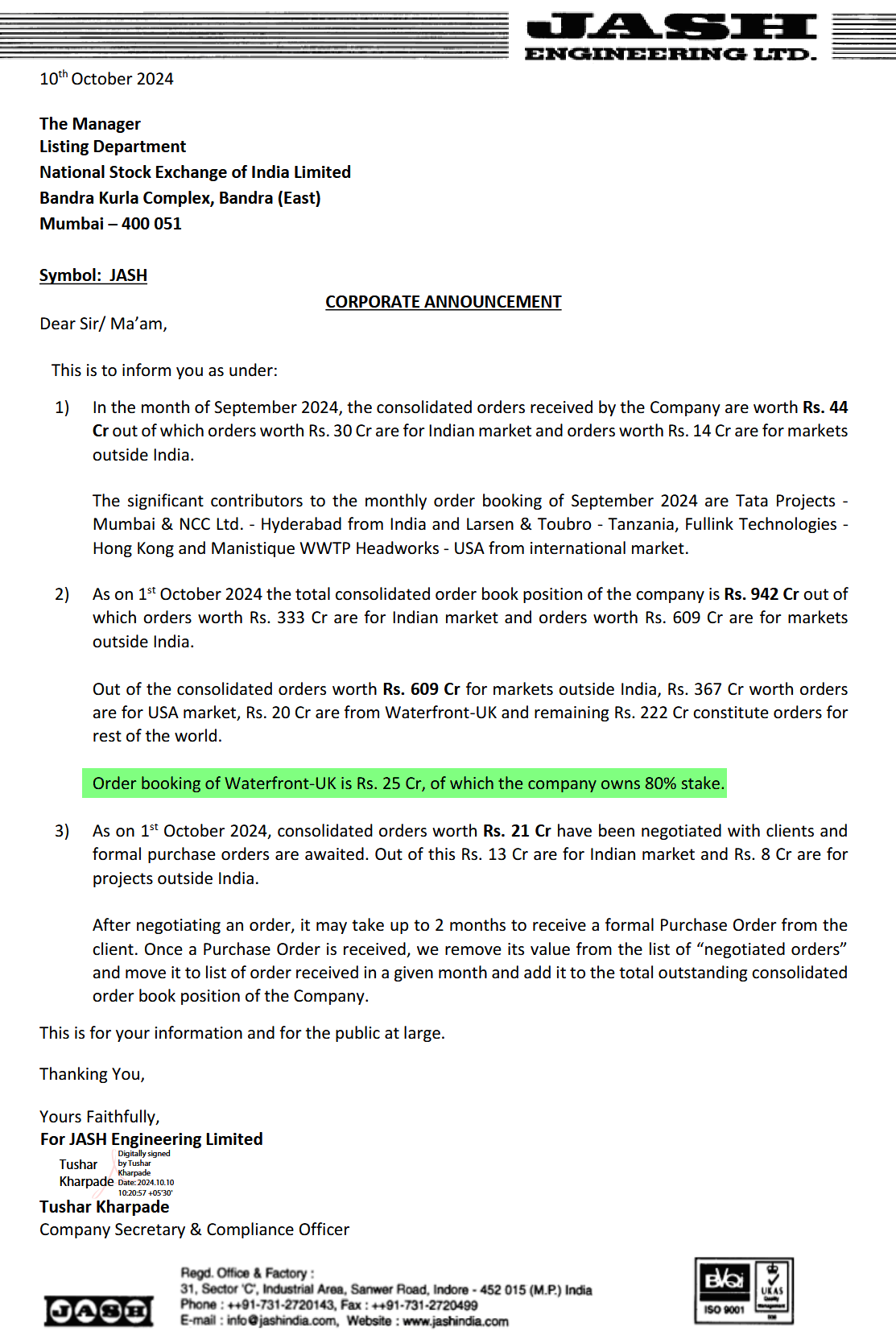

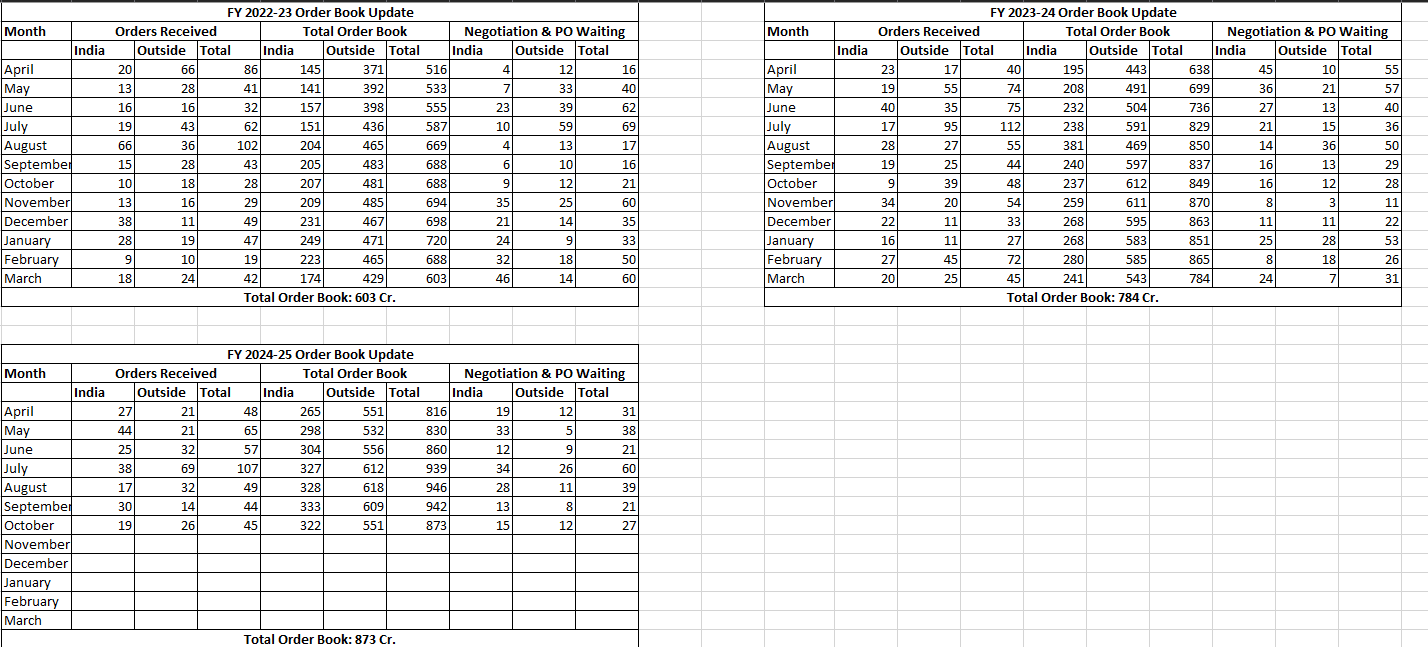

Order book - as on 30/9/24 - 942 crs

Order book - as on 30/6/24 - 939 crs

Order intake during Q2FY24 - 200 crs

Thus Execution during the quarter - 203 crs

Implying solid >100% YOY revenue growth during the quarter. This should also help in improving margins during the quarter

3 Likes

Record Date: 30th October, 2024

Sub-division/Split of Equity Shares of 1 equity share of the

Company having face value of ₹10/- each into 5 (Five) equity

shares having face value of ₹2/- each

https://nsearchives.nseindia.com/corporate/JASH_15102024122151_NSEINTIMATIONRECORDDATE.pdf

3 Likes

Management Guidance

Jash:

-

675-700 Cr REV by FY25

-

25-30 % REV growth

-

Margins to improve

1 Like

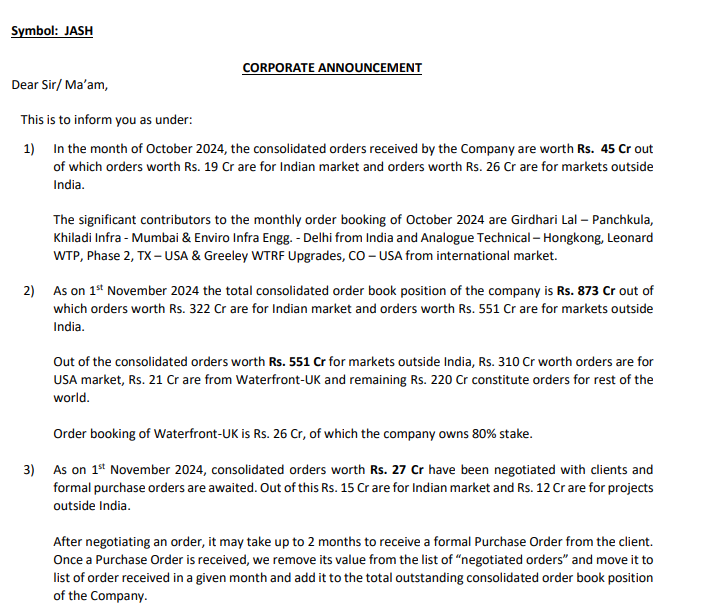

In the month of October 2024, the consolidated orders received by the Company are worth Rs. 45 Cr out of which orders worth Rs. 19 Cr are for Indian market and orders worth Rs. 26 Cr are for markets outside India.

The significant contributors to the monthly order booking of October 2024 are Girdhari Lal – Panchkula, Khiladi Infra - Mumbai & Enviro Infra Engg. - Delhi from India and Analogue Technical – Hongkong, Leonard WTP, Phase 2, TX – USA & Greeley WTRF Upgrades, CO – USA from international market.

As on 1st November 2024 the total consolidated order book position of the company is Rs. 873 Cr out of which orders worth Rs. 322 Cr are for Indian market and orders worth Rs. 551 Cr are for markets outside India.

Out of the consolidated orders worth Rs. 551 Cr for markets outside India, Rs. 310 Cr worth orders are for USA market, Rs. 21 Cr are from Waterfront-UK and remaining Rs. 220 Cr constitute orders for rest of the world.

Order booking of Waterfront-UK is Rs. 26 Cr, of which the company owns 80% stake.

3 Likes

any plans to update these tables ? would be really helpful

1 Like

Purchase of stock in trade and change inventories

Why are the negative and what do they signify

Change in inventory=Opening Stock less Closing stock. Negative change in inventory means closing stock is more than opening stock. Closing stock will be shown in balance sheet. Change in inventory will have impact in PL and cash flow.

2 Likes

Jash Engineering -

Q2 FY 25 concall and results highlights -

Revenues - 140 vs 95 cr, up 46 pc

EBITDA - 25 vs 14 cr, up 78 pc ( margins @ 18 vs 15 pc )

PAT - 16 vs 9 cr up 78 pc

Company profile -

An engineering company making critical products for Fresh water and Sea water intake systems, fresh water and waste water pumping stations, de-salination plants, storm water pumping stations, hydro-power generation and also for manufacturing industries like - Steel, cement, Paper & Pulp, Petrochemicals, Fertilizers and other process plants

Product Portfolio includes -

Water Intake systems - Like - Penstock gates, Open channel gates, Downward opening Weir gates, Flap gates, Stop Logs

Heavy fabricated gates - Bulkhead slide gates, Roller gates, butterfly gates, Crest gates, Radial / Tainter gates, Bonneted gates

Coarse screening equipment - Trash rack, MMR screen, MultiRake screen, suspended trash racks

Fine Screening equipment - Screenmat step screen, Rotoclean rotary drum screen, Rotobrush Rotary screen, Mahr Perscalator screen, Travelling band screen

Gate Valves

Solid Bulk handling Valves

Special purpose Valves

Process equipments like -

Water clarifiers

Detritors

Slow speed floating aerators

Slow speed fixed aerators

Hydropower Screw generator

Screw Pumps

Filtering equipment

Secondary treatment Equipment like -

Diffuser aeration

Mixing and Aeration equipment

Decanting equipment

Turbo Blower

Segment wise revenue contribution for H1 FY 25 -

Water Control Gates - 59 pc

Screening equipment - 22 pc

Valves - 10 pc

Hydropower & Pumping, Process Eqpt and Others - 9 pc

Geography wise revenues in H1 -

US - 87 cr

EU + Africa - 23 cr

ME - 1 cr

SE Asia - 46 cr

India - 97 cr

Order Book of company and its subsidiaries -

Jash Engineering + Shivpad Engineering - 460 cr

Rodney Hunt ( Jash USA ) - 280 cr

Waterfront Fluid Controls ( Jash UK ) - 40 cr

Guidance for FY 25 -

Revenues - 675 cr vs 516 cr LY

EBITDA margins in 21-23 pc band vs 19 pc LY

PAT margins in 12 - 14 pc band vs 13 pc LY

Rodney Hunt ( Jash USA ) has done H1 revenues of 89 cr and has reported a net loss of 9 cr for H1. Company expects Rodney Hunt to report a revenue of 275 cr for full FY 25 with significantly positive PAT

Capex - currently working on a new manufacturing plant @ Shivpad ( Chennai ) and brownfield expansion @ SEZ Unit 4 in Pithampur. Both these plants should get commissioned in FY 26. These plants should help them achieve their revenue tgt of Rs 1000 cr by FY 28 ( a conservative tgt - company’s admission )

Company - at present operates via its 6 manufacturing locations - 04 in India, 01 each in UK and US. Current employee strength @ slightly above 1000. Company is approved by most municipal authorities in India and Abroad. These approvals are extremely critical in the company’s line of business

Overtime - company has made 04 major acquisitions - Rodney Hunt ( US ) , Waterfront ( UK ), Shivpad ( India ) and Mahr Maschinenbau ( in Europe )

Shivpad was acquired to help in treatment process equipment

Mahr Meashinenbeu was acquired to get bet screens technology in the world

Rodney Hunt was acquired for their brand value in US

Waterfront was acquired for their penetration in the UK mkts

Company has a technical collaboration with Invent ( Germany ) to make Disc Filters and have already started manufacturing the same

Equipment like - diffusers, Mixing and Aeration equipment, Decanting equipment, Turbo Blowers are recent additions to company’s products portfolio

Company executed some legacy orders from its Rodney Hunt subsidiary in Q1. These had thin margins. Future pipeline of Rodney Hunt has much better profitability

As the company’s turnover keeps rising, even Q1,Q2 will start to report descent profits from FY 26 onwards

Most of the manufacturing is done by the company - in-house, as the products made by them are custom made on order to suit the customer requirements. This also increases the number of SKUs and is a natural entry barrier

Expect Q3 to be the turn-around qtr for Rodney Hunt ( their US subsidiary )

Order book as on 01 Nov has risen to 873 cr. In Oct alone, have generated revenues of 75 cr alone from US

Re-focussing on ME markets - to accelerate business growth in that area

At present, 231 employees hold ESOPs in the company

Company has a JV with Invent ( Germany ) to make and sell diffusers, blowers and Decanters. However, the products made by Invent are on the costlier side ( but have the best quality ). The total mkt in India for these products is currently @ 300-400 cr

Expect to get orders worth aprox 450 cr in next 4 months Ie Dec, Jan, Feb, Mar

Company commands a mkt share of aprox 65 pc in India in Water control gates business. Total mkt size in India is about 250 cr

In US, the size of mkt in water gates segment is about 1700 cr. In UK + Canada + ME + SE Asia - the combined mkt size should be around 700 cr

As per BABA act in US ( Build in America, Build for America ), 65 of products being sold in US have to be built in US and by 2029 this must go upto 95 pc. This Act only applies to projects being funded by US govt. Since company have their manufacturing facilities in US ( via Rodney Hunt ), they should be benefitted. Plus they intend to put up another facility in US in FY 27

Rodney Hunt had to execute some legacy orders which are low margin in nature. Only 50 cr worth of these low margin orders are pending out of an order book of > 300 cr in US

Rodney Hunt did revenues of aprox 220 cr in FY 24. Should do revenues of aprox 275 cr in FY 25 - naturally, the EBITDA margins should get a boost as most fixed costs remain constant

Most of company’s clients are EPC players - hydro power projects, waste water treatment, implementing flood prevention projects, sea water ingress management kind of spaces

Disc: invested, biased, not SEBI registered, not a buy/sell recommendation

17 Likes

Continuing the legacy of @Lajja_Shah

7 Likes

Currently dont own the stock so not tracking. Exited at 2362 (before split). Post Bonus, i dont think i will enter the stock before 500. So not tracking the order book anymore. But thanks for sharing.

1 Like

Any reason why you exited the stock? I have started tracking the company recently. I feel like I’m late to the party. However, there further growth left if bought at the correct price.

1 Like