Jana Small Finance Bank: [BSE: 544118] : NSE [JSFB].

CMP 433. FY 2024 Recorded PE at 6.8 times, Normalized PE of 11.75 (PE Looks Lower due to Deferred Tax Assets they have of approximately 801 crore at year end 2024.

Small Finance bank with big ambitions.

Jana Small Finance Bank has its DNA from Janalakshmi Financial Services (JFS) that got NBFC license in 2008. It was started by NGO to provide Microfinance loans to the needy. Later it transformed into Jana Small Finance Bank when RBI granted it a Small Finance Bank License. They listed their IPO in February 2024. JSFB is ranked as the fourth Largest Small finance bank in India.

Lets Do a SWOT Analysis of this bank -

Strengths:

- Pan India Presence with no concentration risk in geographies and wide coverage of around 776 Branches.

- Appealing product suite for Deposit and various attractive features like higher Interest Rates of upto 7.5% on saving account and upto 8.25% on Fixed Deposits. Monthly Interest credit for senior citizens and plans to introduce it to all customers.

- Seasoned and experienced Management.

- Unique Banking approach in asset side to be the core banker for all loan customer needs and anchoring towards affordable housing.

- Their deposit growth is more than 200 % of market growth in the last few years due to attractive Interest rates they offer.

- Higher Share of Secured book at 65% which was almost 0% in 2018.

- High Capital Adequacy of more than 20%.

Weakness:

- They have unsecured loan book of 35% of the portfolio which may perform very poorly during a bad business cycle as it has in past. This could result in higher Non-Performing Assets.

- High Cost of Deposits even though they are a bank. Cost of funds higher as they give higher Interest on savings and FDs.

- They cannot compete with bigger banks for Prime Loan customers and are not a truly core banking partner for deposit side customer.

Opportunities:

- JSFB is not even 0.15% of Indian Deposit and Advance size. Indian Banking is growing at 15% on loan side and 13% on deposit side. They can grow by more than market for many extended periods of time for more than 10 years if they play the moves right.

- Transitioning from unorganized lenders to organized lenders.

- Huge Interest Arbitrage (5% Monthly in Un-organized Sector) and Credit bureau data available for second time borrower.

- Moving from unsecured to Secured loans in Affordable Housing as anchor Product. From 0% secured loans in 2018 to 65% in Secured loans as on Q2-2025 and guidance towards 80% secured loans in next 3 years.

- Converting into a universal bank if they meet eligibility criteria in the next year. This could lead to lower cost of funds and greater confidence in garnering deposits.

Threats:

- Bigger banks with lower cost of funds can come to take their market like in Gold Loan, loan against Property, and take away most of the lucrative business by offering lower rates.

- Any external shocks like Covid19 or say demonetization or war like situation or Global Crisis like in 2008 may affect the unsecured side of book more than secured book and result in NPA rising more than the profits.

- A small bank may have higher attrition and may find it difficult to retain good talent.

- Bank being a highly regulated entity there is always a regulatory change risk.

What differentiates a “good bank” from a “not so good bank”, is its management and their vision, systems and practices, strategic positioning and technology.**

- Management – Mr Ajay Kanwal started his journey after completing his BE in Electronic and Telecommunication and MBA. He started his career with Citibank at various positions like CEO of Taiwan and South East Asia, TGP and Mastercard for short time. He was chairman of board at Standard Chartered bank Singapore and many sister companies. He brings in 32 years of industry experience in leadership positions and navigated JSFB after Demonetization.

He has also created a second line of Management that are Focused and have a very clear deliverable goals along with risk management in place. Talking with the staff at local branch suggest that Mr Ajay Kanwal Inspires confidence to the staff members and thay a very positive view towards management. They have a very clear and simple vision of becoming a financer to tier 2, 3 cities and rural areas, and Deposit generation from Metro, Tier 1 and 2.

-

Systems and practice –The management is very system oriented rather than people focused, they spend time making the Minimum viable product in each segment and improving it over time as per inputs they get on ground. Eg If a loan is approved from all parameters line CIBIL Checks, Cash Flows, References, but if the visiting officer who verifies physically to borrower place is not convinced looking at the place the loan is rejected in tune of 10-12%. If there is a software glitch for onboarding it was rectified (Happened For my account Opening with them to test the product). These things are taken up by the top management personally.

-

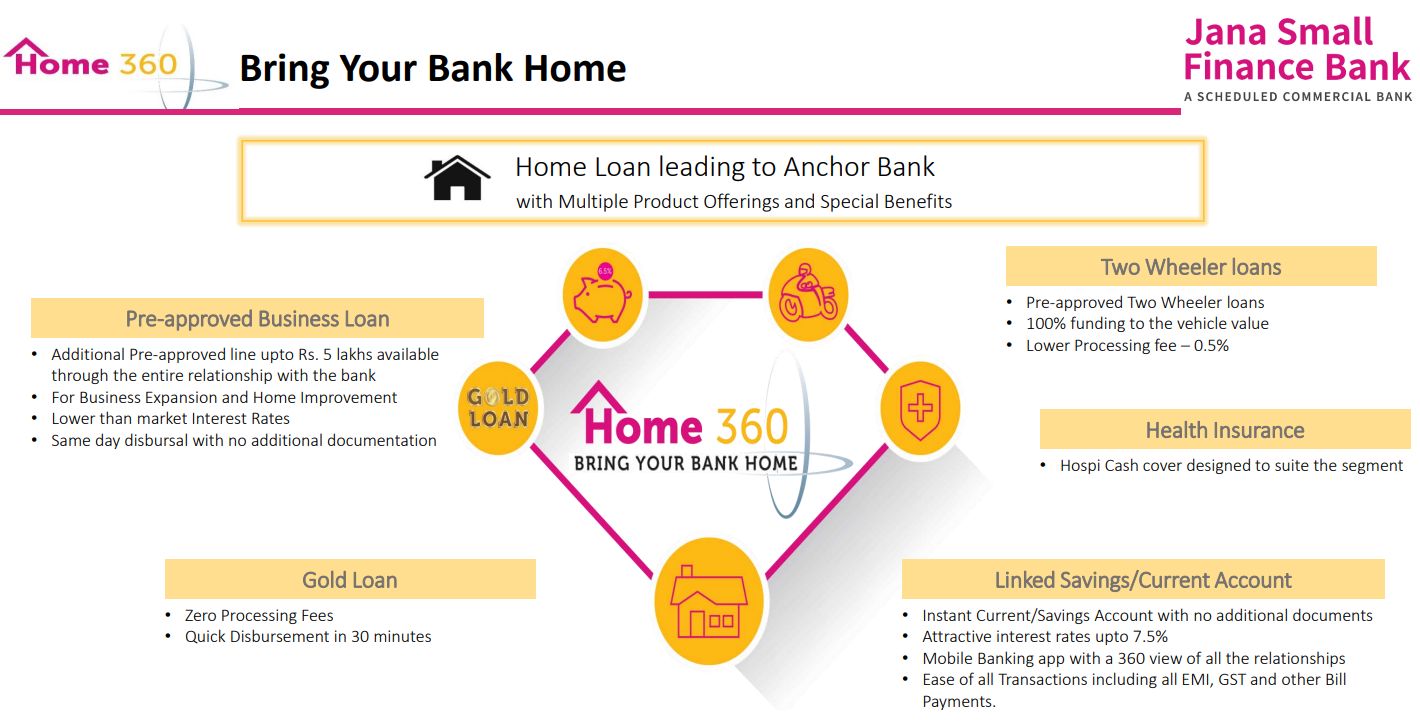

Strategic positioning – The bank has positioned itself as an anchor bank for loan customers by focusing secured affordable housing loans that yield higher Interest for the bank** at the same time they give on open loan limit upto 5 lakh on the same house itself like an LAP that can be availed by the borrower for business purposes with the same house as collateral. Similar way they give two wheeler loan to their affordable housing customer where there is dual collateralization of the two wheeler as well as home loan.

Eg If I take a Home loan of say 15 lakh and a bike loan of 80 thousand and my home loan is paid fully, I still won’t be getting property papers as my bike loan is still outstanding. Similar for say a SME loan or say a commercial vehicle. So this is a play on the biggest purchase of low income groups in affordable housing along with cross cauterization of various products that makes it a very secure play. They are now adding various untapped opportunities in a big way that have secured book along with good Net Interest Margin like a gold loan, Second hand cars, commercial vehicle. India’s Affordable housing sector is projected to grow faster than overall bank credit.

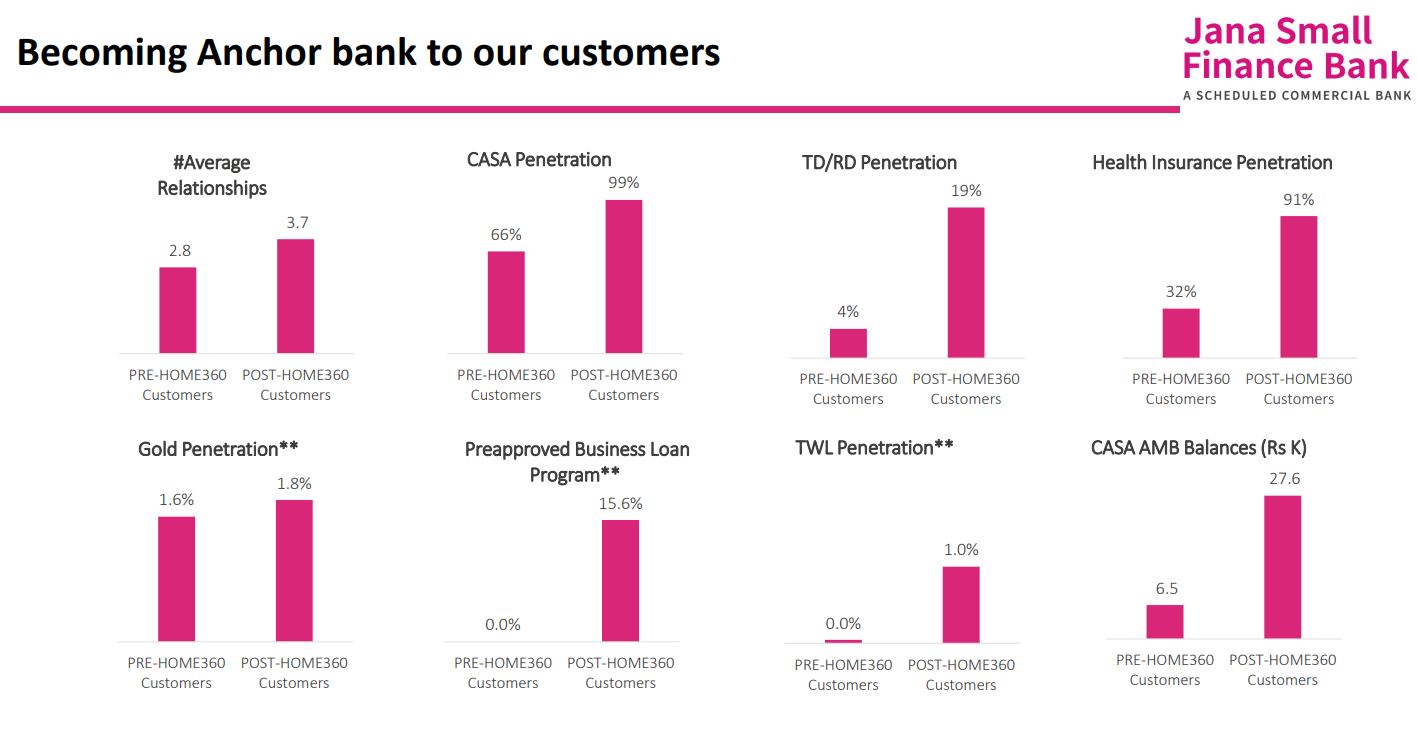

Here is a pictorial representation of average customer relationship Pre-Home360 (Home Loans as Anchor Product) and post Home360.

A)We can see a clear 32% rise in average customer relations like Saving account with loan, OD facility, Insurance, TD, Two wheeler loans etc.

B) 99% HOME360 customers have CASA accounts with bank as against 66% before.

C) Term Deposit and Recurring Deposit Penetration from Just 4% to 19%

D) Health Insurance for HOME360 Customers at 91% from just 32%

E) Pre-Approved business loan top up from 0% to 15.6%

F) Two-wheeler loan from 0.1% to 1%

G) Average Monthly Current account and Saving Account balances have grown from approximately 6500 Rupees to 27600 Rupees a growth of more than 320%.

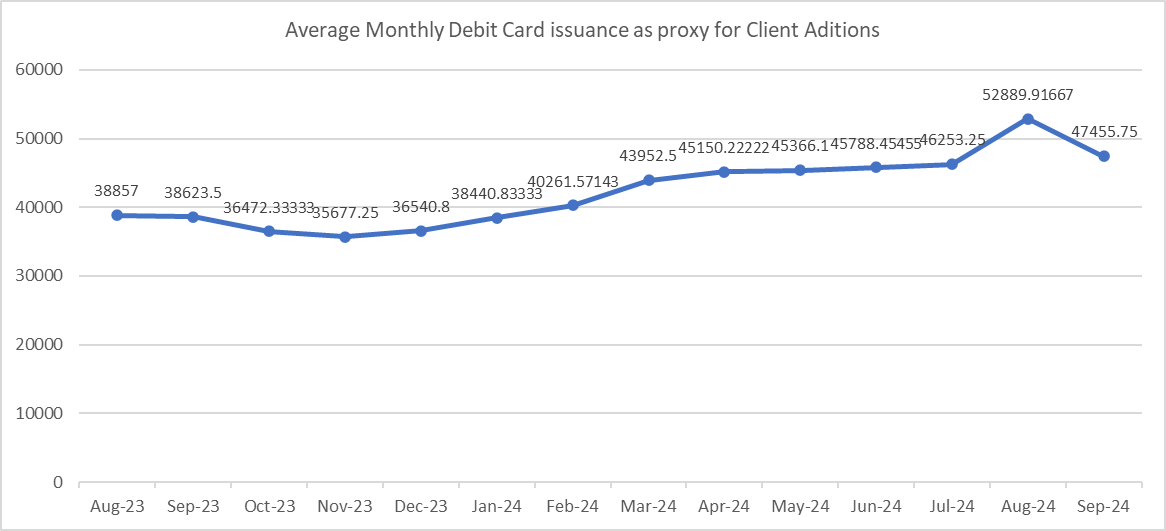

- Technology – The biggest factor in today’s world is how well an entity uses technology as enabler and how can technology be used to get competitive advantage. On asking how will they compete with legacy banks that have very high technology budget and are very big, will this lead to cash burn just to keep up with older and much bigger banks. The management replied that they have technology built in all their processes right from account opening to servicing along with ever evolving systems and continuous improvement. They have an onboarding system where you can do account opening within 5 minutes and activation within 60 minutes if you have Adhaar linked OTP based account opening and 2 days if its offline process and all the documents are as per requirements. Almost all services that do not require direct personal verification can be done online. This has resulted in Debit card issuance as a proxy of Client addition from approximately in range of 38500 odd to range of 47000 each month.

- Operational parameters – JSFB has been able to gain market share on all the parameters like Debit Card issuances, Deposit Growth as well as credit growth YOY, along with growth in Deposit per branch when compared to all the other small finance banks as well as established and the market in general by a huge margin. Let’s Illustrate it with deposit growth Year on year for Q1 FY25.

The Industry Growth rate is 13.2%, Private bank growth rate is approximately 15.75%, PUS growth rate is 8.4% but JSFB Growth rate in deposits is 41% which is more than 300% more than market. Here they are gaining market share from overall banking industry as well as from the Established big Private banks and growing by more than 260% than a well-established private bank.

I am tracking Deposit growth because it is deposit growth that will drive Advance growth and advance growth is what will drive profitability growth. A strong deposit growth is sign that the customers are trusting the bank and bank is doing something right that people are choosing this bank than others. Last quarter HDFC, Kotak Mahindra bank, AU Small Finance bank, Axis bank, State bank of India, Bank of Baroda all have actually lost deposits (Negative Growth) than March quarter as against 5% deposit growth for JSFB.

I believe only banks with robust deposit growth will be able to grow and become leaders in growth in the next cycle whereas PSUs and larger Banks will lose market share to Likes of JSFB as they are offering various incentives like Higher Interest rates and monthly interest payment cycles, Bundled lifestyle benefits like golf courses, OTT subscriptions, SPA services, Pick up Facilities of cheque, locker facilities at discount and Zero fee banking that larger banks and PSU banks are not able to give or have lower service quality than JSFB of you hold same amount of deposit with them.

In the Table you can see how much difference is there between all the banks raw material (Deposit).

| BANKS Deposit Growth YOY for Q1 FY25 | Deposit Growth |

|---|---|

| JANA SMALL FINANCE BANK LTD | 41% |

| SURYODAY SMALL FINANCE BANK LTD | 42.20% |

| UJJIVAN SMALL FINANCE BANK LTD | 22% |

| AU SMALL FINANCE BANK LTD – Ex Merger | 25.17% |

| ESAF SMALL FINANCE BANK LTD | 33.40% |

| UTKARSH SMALL FINANCE BANK LTD | 30% |

| HDFC BANK – Ex Merger | 16.9% |

| ICICI BANK | 15.1% |

| KOTAK MAHINDRA BANK | 15.54% |

| AXIS BANK | 12.83% |

| STATA BANK OF INDIA | 8.18% |

| PUNJAN NATIONAL BANK | 8.5% |

| BANK OF BARODA | 8.9% |

| BANKING INDUSTRY | 13.2% |

JSFB along with many small finance banks have a PE that is less than Nifty, Banking sector as well as private banks, Higher growth rate in profitability for next 3 to 5 years and available at cheap valuations along with high margin of safety on the downside

Key Triggers –

-

Higher Growth rates than market in Deposits, Sales and profitability

-

Cheaper valuations than Indian market, banking sector as well as private banks

-

Converting into a universal bank after 1 year subject to eligibility criteria which they qualify and need to be qualified for 6 more months

-

750 Crores of additional capital will come for next 3 years as they have Deferred tax assets that they will receive so no Income tax for next three years

-

One of the highest secured books in small finance banks at 65% and plan to raise to 80% in next 3 years thus reducing Risk in the book, increased stability and predictability in profits.

Disc - Holding in family account and can add or reduce any time.

Not a recommendation, for educational purposes only, consult your financial and investment advisor before investing.