Many a times companies will only disclose what is mandatory under law, and nothing more. You can get financials of unlisted companies from the RoC website or private sites like Tofler at a nominal cost if you are very keen.

I Believe CV slowdown is more prominent than PV. I am from same town as one of JAI’s biggest plants and the company has a very good reputation. However, last few months have been very slow. I was waiting to buy but somehow the shares do not reflect this slowdown as yet. I am expecting the shares to go down when their

Thank you for your help. I have obtained the financials from MCA of the LLP. Above here are the reported revenues of standalone, consolidated and LLP.

JAI LLP is the only revenue generating subsidiary disclosed. The standalone entity has disclosed in the RPT, the Sales it makes to the LLP. Therefore, we have arrived at the Standalone entity’s Sales from external customers[D].

Consolidated revenues should be the sum of Standalone entity’s sales from external customers and Total Sales of the LLP. Therefore, I have calculated LLP Sales as the difference between Consolidated Sales and External Sales of JAI Standalone.

However, I am getting a getting significant differences between the reported and calculated figures.

Can someone please guide me where I am going wrong?

Also, in FY19 Standalone entity made Sales to LLP of 559.84cr. If we examine the LLP’s financials, Raw Material cost(379cr) and Purchase of finished goods(126cr) total 505cr.

We can assume that RM Cost includes goods procured from JAI Standalone on which the LLP carries out certain value-addition.

Shouldn’t the remaining value reflect in inventory.

Inventory as if FY18: 13.8cr

Inventory as of FY19: 32.2cr

@Rahuldos777 Not sure with what granularity the data of MCA is. You have to check whether the definition of sales is the same everywhere e.g. sales may include or exclude scrap sales, export incentives, service income, discounts & commission etc. Also whether there are any sales from LLP to the Standalone entity? Factor that in too. It is best to write to the company and seek answers on this.

Value addition in LLP cannot be this much. Most probably, Rs.559 crores would include both RM & FG.

little dated, however gives some insight on the nature of partnership with Tinsley Bridge:

"The agreement involves the transfer of technology and the technical support required to develop the Extralite Leaf Springs for the Indian market.

Extralite technology enables the manufacture of high strength, lighter springs with increased life for commercial vehicles."

Disc:

Invested, have also transacted in last 30 days.

Tarun

Total of RM+Purchase of finished goods is only 505cr out of 559cr. What about the remaining 55cr?

Thanks for your help. JAI LLP gives no bifurcation of its sales and it has no other income

Some basic queries that I have wrt Jamna -

- Where does the company procure RM (steel)?

- What is the status of the plant that was partially shut down due to lack of demand.

- When can we expect the M&HCV sales to revive?

Q4 Results expected on 10 Jun. But till then can fellow boarders throw any light on any useful information about this company?

Disc: Tracking position at higher levels

Q4 Results as expected.

Sales

1127 cr down 47%

Profit at 48 cr down 72% - owing to high cost of raw materials I suppose.

Balance sheet

- Long Term Borrowings : 51 cr from 3 cr last year

- Short Term Borrowings: 86 cr from 0 last year

- Payables : down to 38 cr from 436 cr last year

- Receivables : down to 80 cr from 304 cr last year

- Receivable turn over: 5.88 down from 8.63

- Inventory turn over: 6.3 down from 11

Nothing to write about. Company might be burning it’s cash right now. Would love to hear fellow members’ thoughts on this.

Investor Presentation - https://www.researchbytes.com/CompanyEventList.aspx?cc=J0058

1 Like

This company seems to have bottomed out now at CMP of 29 Rs. and is only india based player in this market (as rest all player having JVs with Foreign players). After this pandemic’s effects are reduced and with government elections still away, So i feel orders should start to flow for Jamna Heavily. Recently spoke to a friend in BMC where he told that they are also going to invite fresh tender for electric buses after this pandemic

(Disclaimer: i am invested in Jamna Auto)

1 Like

40828_pdf.pdf (914.1 KB)

Jamna Auto Industries Limited is India’s largest, and among world’s third largest, manufacturer of tapered leaf springs and parabolic springs for automobiles. The Company was first to introduce parabolic springs in India. I like the business model of the company, bcos suspensions are a must for any vehicle, normal vehicle or an electric vehicle(EV), for a 2 wheeler, 3 wheeler or any wheeler . So, suspensions are here to stay, even when the EV revolution happens… Additionally, this is one of the market leaders in India as well as world, Also, it is available at such an attractive valuation. All the more reasons to buy this…

Having said all this, I am in a bit of dilemma in terms of selecting the stock to invest. On one side, I have Bajaj finance , which offers a high ROE & has a high financial profit margin. On the other hand , I have Jamna Auto, which also has a high ROE, but the operation profit margin is low ,~10%, which effectively translates to a much higher investment for the same amt of profit, which means this is a capital intensive company. Again , I am not complaining abt the margin , bcos the entire Auto sector operates at that margin. But, at the end of the day, I will be concerned abt my returns…

Now, can someone please explain me, how to take decisions in these situations. If we have a choice to make between 2 companies , which are same in terms of all the metrics , except in operating margin. One of them has a higher operating profit margin ( or EBIDTA) than the other.How to take a call in that case? If you have any other different view, different perspective of selecting stocks, I am open to them as well.

Disclaimer : I am invested partly in Jamna Auto , a bit heavily in Bajaj finance. So, my views may be biased.

1 Like

I don’t think you should compare two companies in such different industries on any financial parameter like this. You should look at the relative position of each company within its industry and assess the prospects of that company and business and then decide where you have the best bargain (risk adjusted return).

5 Likes

After some time I can see research reports on Jamna auto coming up these days . Ashok leyland management indicating good recovery in CV space, scrappage policy, chart wise it has crossed golden cross, Promotors buying shares from market and same time pledging also .

Are we getting into next CV cycle.?

This is one recent article i found on jamna auto management

Disc: Invested

2 Likes

Jamna Autos has a stated "Lakshya"of 33% revenue from new products and 33% revenue from new markets. The company claim to have been achieving this. Doesn’t this imply that their revenue growth should be minimum 33% each year or atleast close to that. Actually its much lower. Does it mean that its existing products are getting obsolete. They are not, Does it mean they are losing customers. ???

1 Like

I don’t think that is an annual recurring target. It would be something like a 5-year vision probably. You can go back to past Annual Reports and see when it was first introduced, most likely there the details will be articulated what exactly it means.

2 Likes

This is a screenshot from latest AR. So it looks like an yearly target. I am sure there is some ambiguity in my understanding because this seems like a very ambitious target. Any clarity please??

This is a screenshot from latest AR. So it looks like an yearly target. I am sure there is some ambiguity in my understanding because this seems like a very ambitious target. Any clarity please??

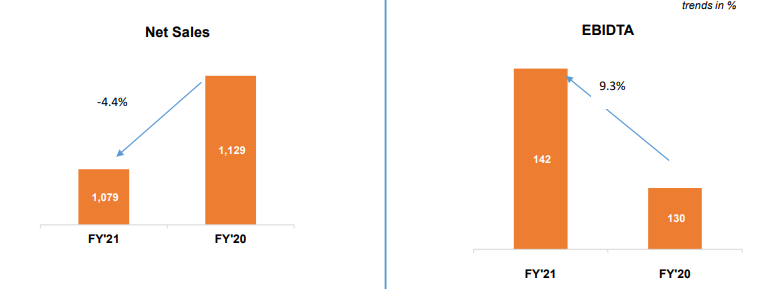

Reasonably decent results by Jamna (link).

- Q4’21 top line 484 Crs (104% growth Y-o-Y, although on lower base | 40% growth Q-o-Q).

- Annual revenue figure at 1079 Crs. (de-growth of 4.4%), however, made good by 9.3% EBIDTA growth.

- Healthy EBIDTA margins at 13.2% for FY’21 against 11.5% for FY’20.

- EPS of Rs.1.83 against Rs.1.20 (up 52%).

On BS side, significant inventory built-up and loans. On positive side, heartening to notice reduction in receivables and cash built-up. Most importantly, borrowing stands at Nil.

As an aside, this much distorted the view looks like if the graph axis is not set to 0. ![]()

Source (investor presentation)

Regards,

Tarun

Disc: Invested

2 Likes

2 reports came into my notice recently . first one provide good insight into the past performance. Other one is future looking (upcoming cv cycle)

https://www.nirmalbang.com/nb-research/institutional-research-reports.aspx

check for jamna auto

Disc: Invested

2 Likes