Jain Resource Recycling Ltd – A metal recycling compounder in the making

1. Business overview

Jain Resource Recycling Ltd is a non-ferrous metal recycler focused on lead, copper and aluminium, using a large-scale scrap-to-alloy model. The company’s lead ingots are registered on the London Metal Exchange, which opens up global customers and benchmarks its product quality to international standards. Besides manufacturing alloys, it also does trading in non-ferrous metals and related commodities, which adds a merchanting leg to the business model.

2. Promoters and background

Kamlesh Jain leads the company with over 30 years in the metal industry; it started as a partnership firm before incorporating in 2022. The promoters come from the broader Jain Metal Group, which has built expertise in non-ferrous recycling across India and even a gold refining unit in UAE. Promoters currently hold 73.59% of the equity as of the latest quarter, giving them strong skin in the game.

3. Journey so far

Incorporated in 2022, the company has scaled very rapidly from a small base to over ₹6,100 cr standalone revenue by FY25. In three years, reported sales have grown from ₹236 cr in FY22 to ₹6,143 cr in FY25, driven by capacity ramp-up and higher volumes in recycled metals. Net profit has moved from ₹28 cr in FY22 to ₹211 cr in FY25, while the balance sheet has simultaneously absorbed large increases in assets and working capital.

4. Business model, capacities and utilisation

Jain Resource follows an integrated recycling and refining model: it procures non-ferrous scrap (mostly imported from UAE, US, UK due to weak domestic ecosystem), processes it through smelting/refining at three facilities in SIPCOT Industrial Estate, Gummidipoondi, Chennai (26.94 acres leased land), and sells finished lead, copper and aluminium products. The company’s product basket comprises lead ingots, copper billets/ingots/products, aluminium alloys, with copper-lead-aluminium at ~45%-40%-4% of FY25 revenue. Installed capacities as of Jul 2025: copper products 45,360 MTPA, aluminium 9,744 MTPA, copper billets/ingots 17,282 MTPA (total ~3.1-3.26 lakh MTPA across facilities); actual production ~64,619 MTPA (recycling) + 88 MTPA (Hosur); FY25 utilisations ~40% copper, ~88% lead, near full aluminium.

5. Industry tailwinds

Globally and in India, there is a gradual policy and customer push toward circular economy models and higher recycled content in metals, which structurally benefits organised recyclers. Recycling of lead, copper and aluminium lowers energy use versus primary metal production and fits into the broader ESG narrative for downstream customers. India’s rising metal consumption, especially in power, autos, batteries and infrastructure, provides a large and growing scrap pool over time for players like Jain Resource.

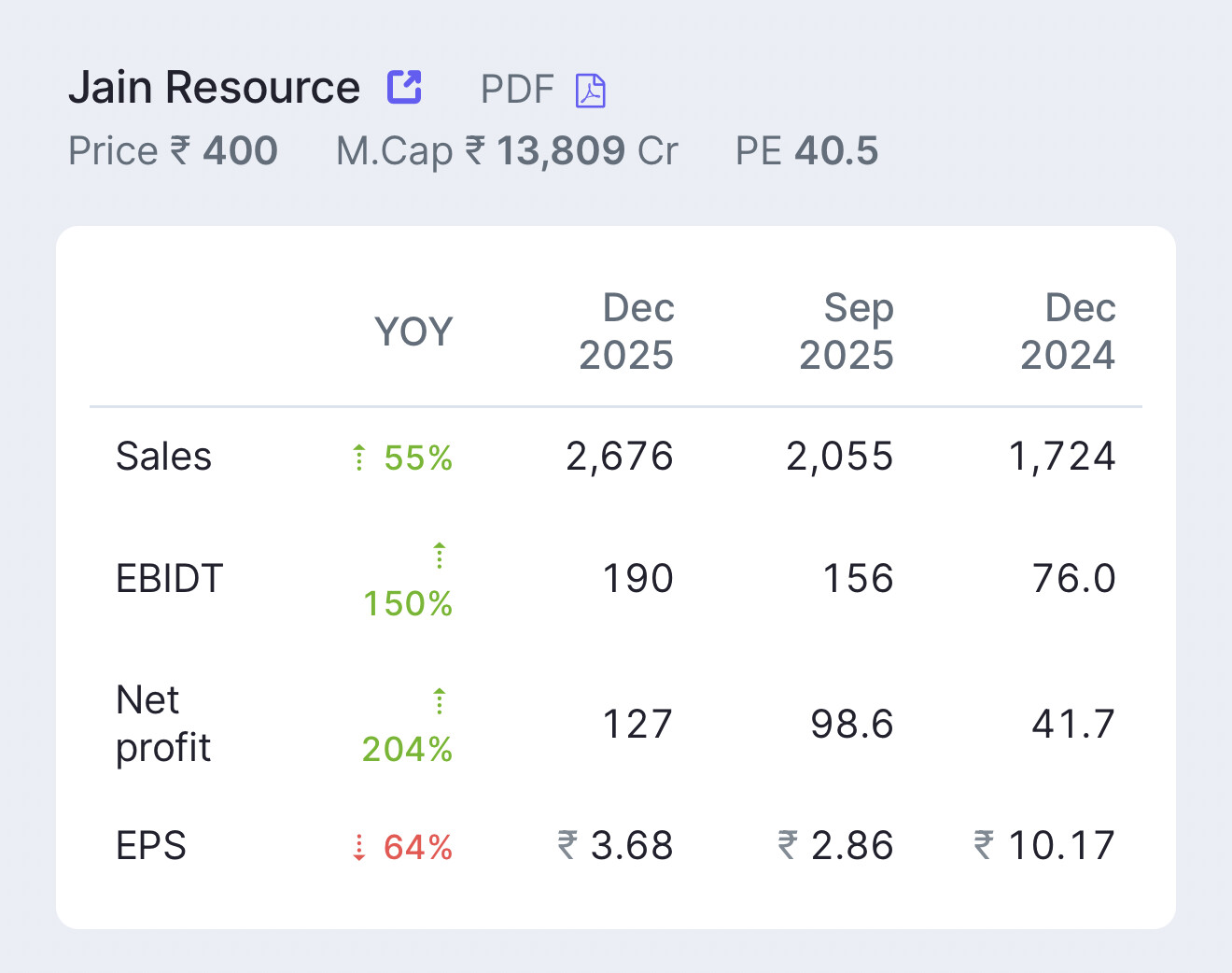

6. Financial snapshot

Market cap stands at around ₹13,900 cr with the stock around ₹404 and a trailing P/E of ~55. ROCE is healthy at about 27.2% and last reported ROE at 39%, indicating high returns on capital at the current scale. The company has not paid dividends so far and is likely reinvesting cash flows back into capacity and growth (0% payout).

Key financial trends

Revenue: ₹236 cr (FY22) → ₹1,880 cr (FY23) → ₹4,157 cr (FY24) → ₹6,143 cr (FY25). Operating profit: ₹35 cr → ₹102 cr → ₹226 cr → ₹345 cr, with OPM stabilising in the mid-single digits (5–6%). PAT: ₹28 cr → ₹61 cr → ₹160 cr → ₹211 cr over the same period, implying ~95% three-year compounded profit growth. Three-year compounded sales growth is ~196% and TTM sales growth is ~48%, reflecting a rapid scale-up phase.

7. Balance sheet and cash flows

Net worth has increased sharply with equity capital rising from ₹40 cr in FY22 to ₹69 cr by Sep-25 and reserves from ₹28 cr to ₹1,282 cr in the same period. Total liabilities have grown from ₹544 cr in FY22 to ₹4,156 cr by Sep-25 as the company has expanded its asset base and working capital. Fixed assets and related capital work-in-progress have moved up meaningfully, indicating ongoing capacity addition and brownfield expansion. Cash conversion cycle has improved from 394 days in FY22 to 42 days in FY25, with debtor days falling from 162 to 7 and inventory days normalising. Operating cash flows have been lumpy: large negative OCF in FY22 with normalisation and positive flows in FY23–25, while capex and working capital have kept free cash flow under pressure.

8. Ratios and return profile

ROCE has improved from ~20% in FY22 to ~27–28% in recent years, despite the heavy scale-up. Three-year ROE stands at around 46%, with the last year at 39%, reflecting strong profitability on a low initial equity base. Working capital days have fluctuated between positive and slightly negative, but the trend in the last two years is towards better efficiency (20 working capital days in FY25).

9. Shareholding pattern (holding disclosures)

Promoters: 73.59%; FII: 6.42% (or ~3.7% per some updates); DII: 3.45% (mutual funds 4.19%, insurance 0.44%); Retail/Public: 13.56-13.99%. No major pledged shares noted; strong promoter holding signals alignment, but track any changes post-Q3 results.

10. Peer snapshot

A quick look at where Jain Resource stands versus some listed non-ferrous peers on Screener:

| Company | CMP (₹) | P/E | Mkt cap (₹ cr) | Div yield (%) | Qtr PAT (₹ cr) | Qtr PAT var (%) | Qtr sales (₹ cr) | Qtr sales var (%) | ROCE (%) |

|---|---|---|---|---|---|---|---|---|---|

| Vedanta | 679.65 | 24.20 | 2,65,769.53 | 6.38 | 7,807.00 | 95.59 | 23,369.00 | 36.96 | 25.26 |

| Jain Resource | 403.50 | 54.96 | 13,924.24 | 0.00 | 98.64 | 80.53 | 2,054.91 | 52.96 | 27.20 |

| Pondy Oxides | 1,262.20 | 32.45 | 3,851.15 | 0.28 | 37.56 | 148.08 | 776.29 | 54.51 | 16.88 |

| Innomet Advanced | 69.25 | 41.11 | 89.61 | 0.00 | 2.02 | 18.13 | 23.53 | 60.72 | 8.51 |

| Bonlon Industrie | 49.50 | 24.90 | 70.21 | 0.00 | -2.12 | -551.06 | 242.00 | 18.25 | 5.04 |

11. Key risks

Commodity price volatility in lead/copper/aluminium scrap and finished metals can squeeze thin margins (already low at 2.5-6%). Heavy import reliance for scrap exposes to forex fluctuations and supply risks, despite some hedging. Operational hazards like high-temp metal handling accidents could disrupt production and lead to liabilities. Regulatory/environmental compliance in recycling is stringent; any lapses could hit operations. Recent Q3 saw PAT drop 75-78% YoY despite 53% sales growth, flagging margin erosion from costs or inefficiencies. Intense competition in fragmented industry and cyclical demand from batteries/autos/infra add cyclicality.

12. Management communication and disclosures

The company is now covered by regular quarterly board meetings and earnings calls; a Q3FY26 earnings call is scheduled on Feb 11, 2026 to discuss the Dec-25 quarter and 9M results. Recent announcements include a board meeting notice under SEBI LODR Reg.29, postal ballot outcomes and scrutiniser’s report, and compliance certificates under SEBI DP Reg.74(5). An October 2025 concall transcript and presentation are available, which should give more colour on capacity plans, margin trajectory and capital allocation (investors should go through this in detail).

13. What to track going forward

Sustainability of margins in a high-volume, low-spread recycling business, especially given the trading component. Balance sheet discipline as assets and liabilities ramp up; ROCE/ROE trajectory once the business reaches a more steady-state growth phase. Execution on capacity additions, diversification across metals and geographies, and any move into higher value-added products or contracts. Quality of cash flows versus reported earnings, as well as working capital intensity in different parts of the cycle.

Disclaimer

Small and midcap stocks and recent IPO stocks carry higher risks due to their smaller size, limited operating history. This analysis is for educational purposes only and should not be considered as investment advice. Always conduct your own research or consult with sebi registered financial advisors before making investment decisions.

My holding : 1% of PF