Jagsonpal Pharmaceuticals(NSE: JAGSNPHARM) has been on a tremendous rise compared to other Pharma peers since last year, its price pattern also looks better compared to its peers.

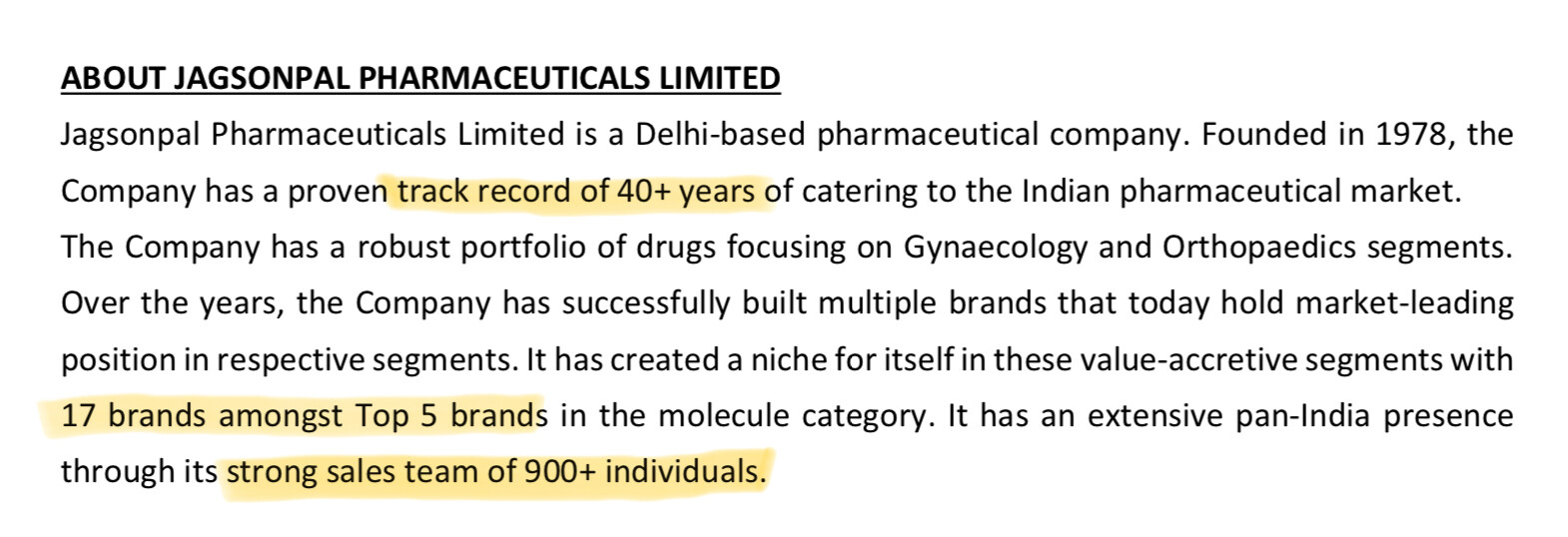

Company specialises in developing and manufacturing bulk drugs and pharmaceutical formulations.The Company has a robust portfolio of drugs focusing on Women Health, Pain and Analgesics and General Medicine.

I am no Pharma investing expert neither have any knowledge about Pharma sector as whole, hence requesting inputs from members. their thoughts on why it is sustain these levels.

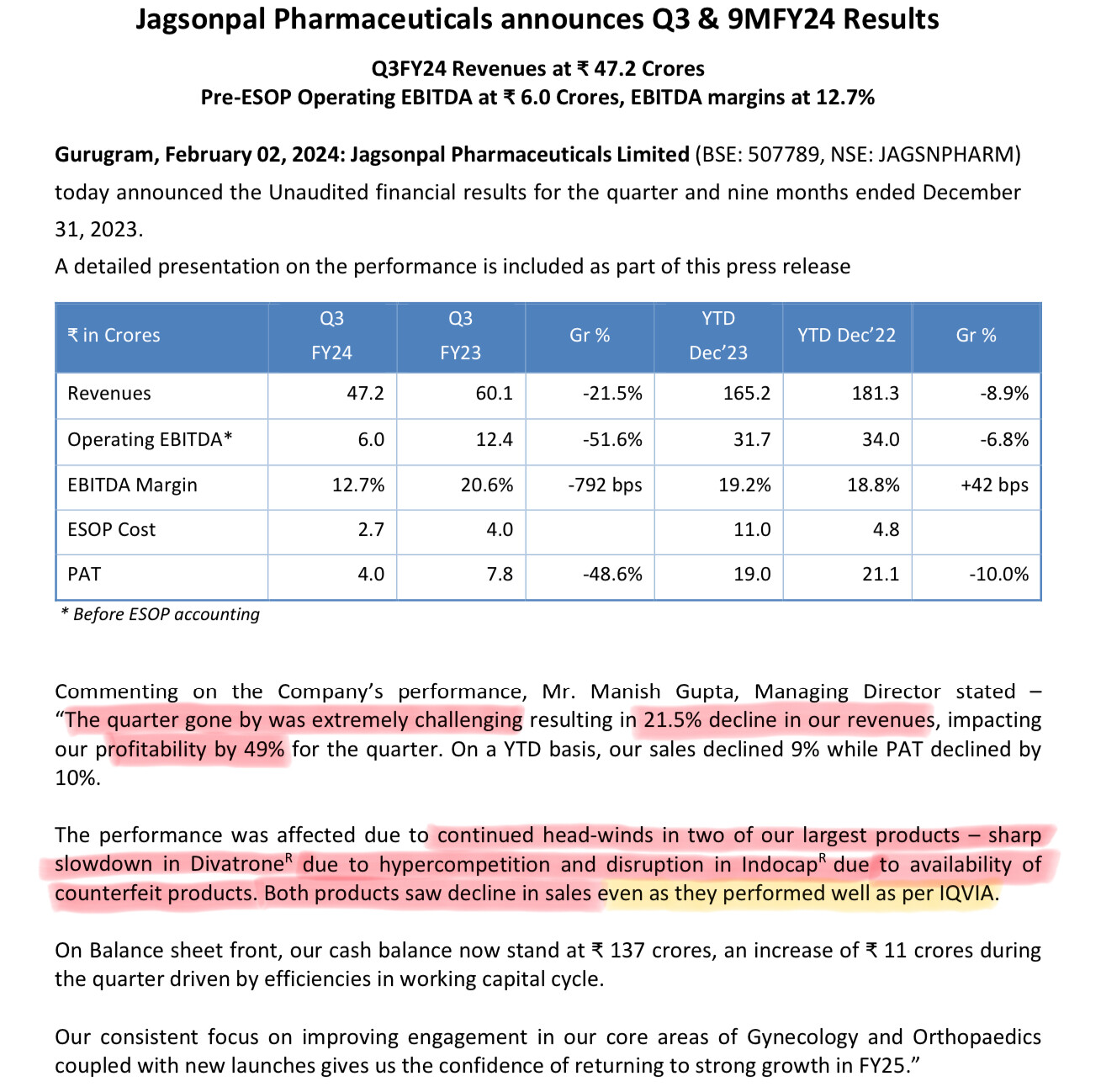

Since June 2020 it has given 1108% returns. If we compare since last year, still it has strongest returns of +135% compared to peers like Sun pharma(+27%), Vivimed labs(-56%) and Kopran(+20%). Quarterly growth on YoY basis does not look so enthusiastic:

Q4 YoY growth:

Revenue:+21%

EPS:-97%

Margin:-98%

For Q3,Q2(YoY) : Revenue growth seems flat at -4% and 5% for Q3 and Q2 respectively, EPS growth is flat for Q3(-0.48%) and up 82% for Q2, Margins up 13% for Q3 and up 100% for Q2.

Annual growth trend compared to last year:

Revenue:+20.20%

EPS:+15%

Margin:+3%

For Fy22Q4 YoY growth numbers, can you please explain if and how this line item resulted in bad bottomline growth? and what are the implications of it?

Nothing will happen. This is a mandatory open offer which was triggered due to promoter change.

There’s not much to say about jagsonpals history. There’s been no growth but it appears they have some good brands in gynaecology and ortho.

I am sure convergent has big plans but Investing here right now is just a bet on the new Jockey. No doubt the new Jockey has quite a reputation but what to expect going forward is a bit of mystery at this stage. I would wait for more details. Without details you don’t know if current valuations are attractive or not

Disc: Tracking

Does this mean the shares will be bought at predefined price of 235rs? But as its public offer, who will sell for lower price than current market price? Or they will need to readjust buying price at current market price?

You are assuming that some action needs to be taken in this open offer. lets take a simple example.Say i takeover jagsonpal where you are a minority shareholder. As the acquirer i am required to make an open offer so that you can tender your shares if you so wish to but Its not mandatory for you to tender your shares. In my case I don’t care what you do with your shares because the open offer was just something I was required to do by law. Needless to say there’s a lot more to it that I don’t entirely understand. This was just a simple example for you to get the gist of it.Read this document If you want to know more about open offer types, setting of price, etc 1503313163982.pdf (321.4 KB)

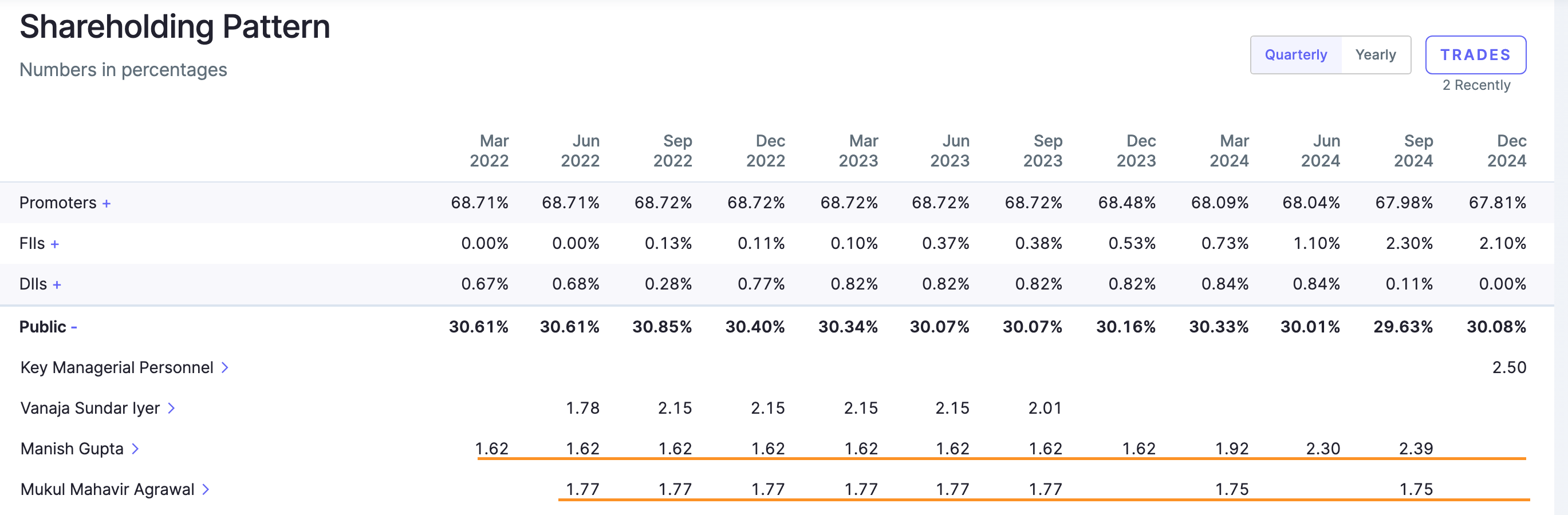

Interesting things have happened in the company post acquisition by Infinity holdings. Manish Gupta ex Sequent has joined the company as Md, Field force which at the time of acquisition was around 600 have increased to 900.

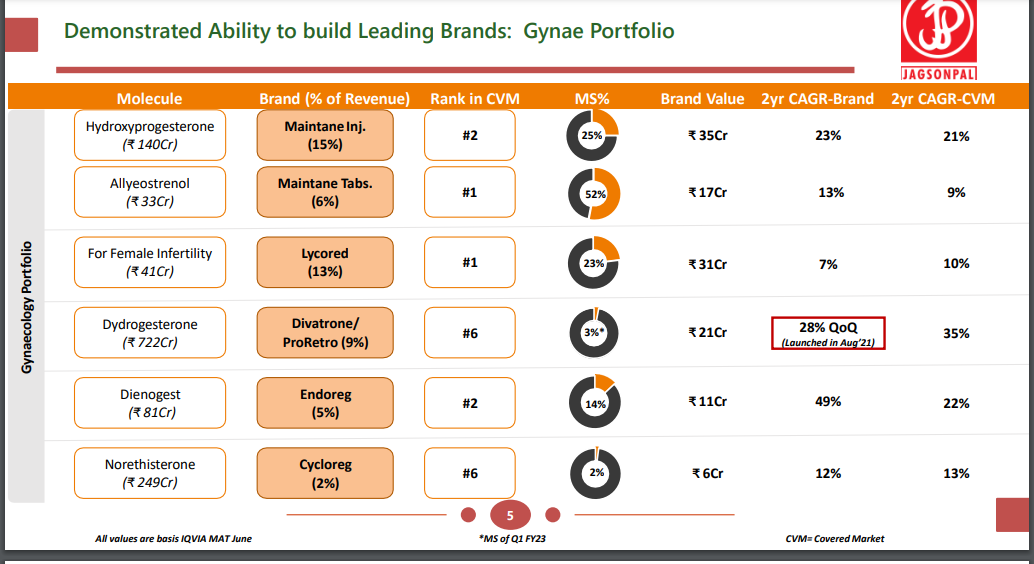

Company shared good presentation after Q1 results. Clearly the focus is on Dydrogesterone which is the fastest growing segment in Gynae. The market has opened up after patent expiry of Abbott and now its a 700cr market growing at 40% cagr !! Mankind was the first one to launch it in 2019…

is the growth sustainable or temporary?

The company outsources its products and so it is a light buniness model. you will not observe meaningful capex in the company.

i am not a expert in medical industry and that is why i require expert opinion in this company.

how is the company keeping its quality control if they do not manufacture the products themselves?

In Indian Pharma Industry, Average Yield per month is around ₹5Lakh => 60 Lakh per Year => potential of annual sales of 540cr.

Mr. Manish Gupta has ability to improve the capabilities of his team, but since last 2-3 quarters, company is facing challenges in top 2 brands for which they increased the capacity (field force).

Therefore average capacity utilisation (of sales team) can generate more than 2xTTM sales. PAT would be much higher in that case.

New launches (as planned in Q4FY24) may improve the yield of sales team.

Just want to share few points which may be relevant in the future of this company :-

1 Mr Manish Gupta, Md had purchased 1.62 % equity of the company in Feb 2022 ie before joining the company as MD @ Rs 235/share… He joined as MD in Aug 22.

2 May be Mr Manish Gupta was instrumental in Purchase of 43% shares by the Infinity Holding arond the same price.

3 Yash pharma acquired by JPL at 2 times P/S which has given exposure to Derma and childcare. Sharing the link of the presentation about both the companies.

Hope to see good growth in top line and the margins keeping in view the past track record of MD. https://www.bseindia.com/stockinfo/AnnPdfOpen.aspx?Pname=4e8819fe-ac27-486d-a702-78c42da4ea1b.pdf

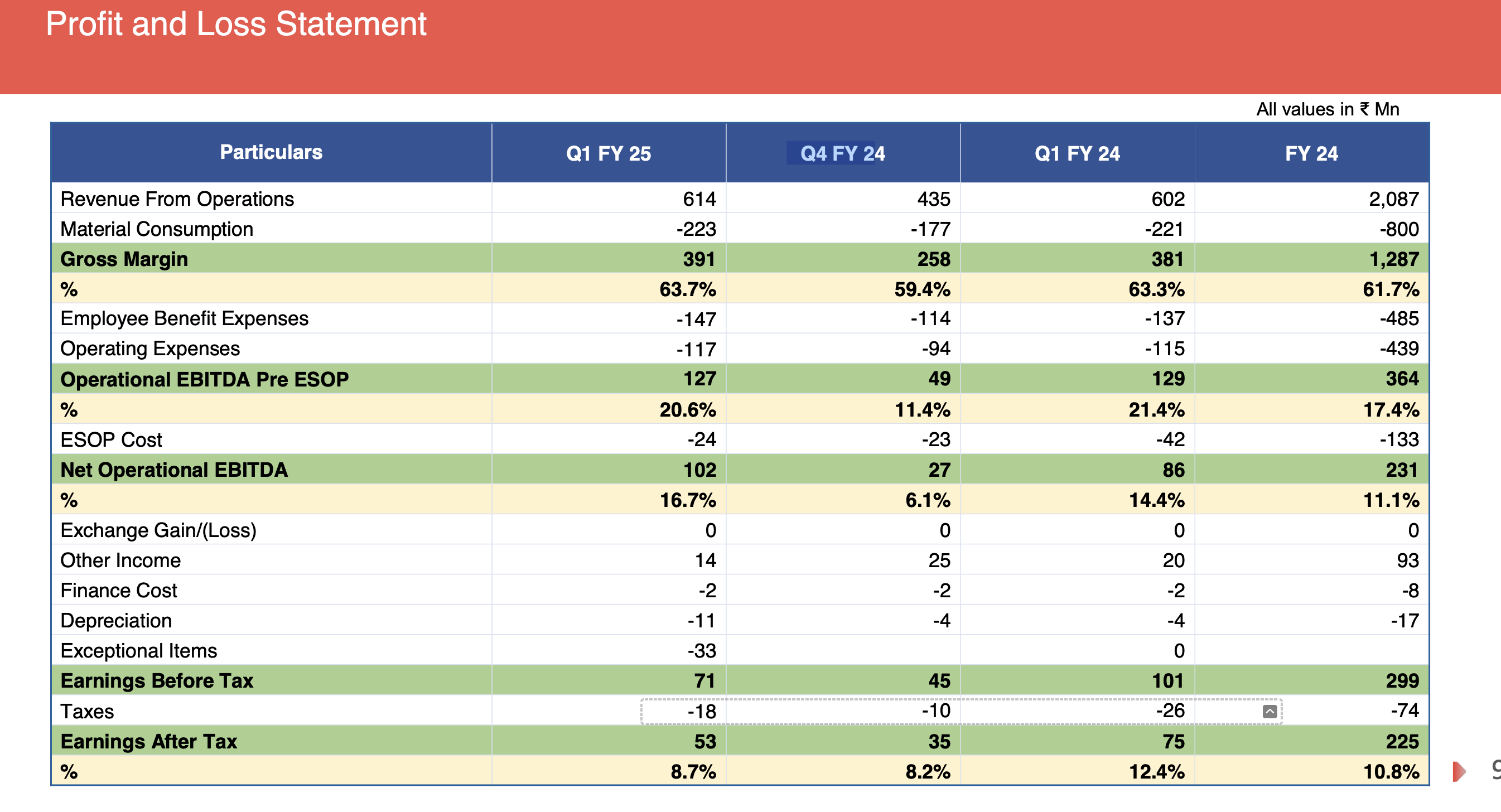

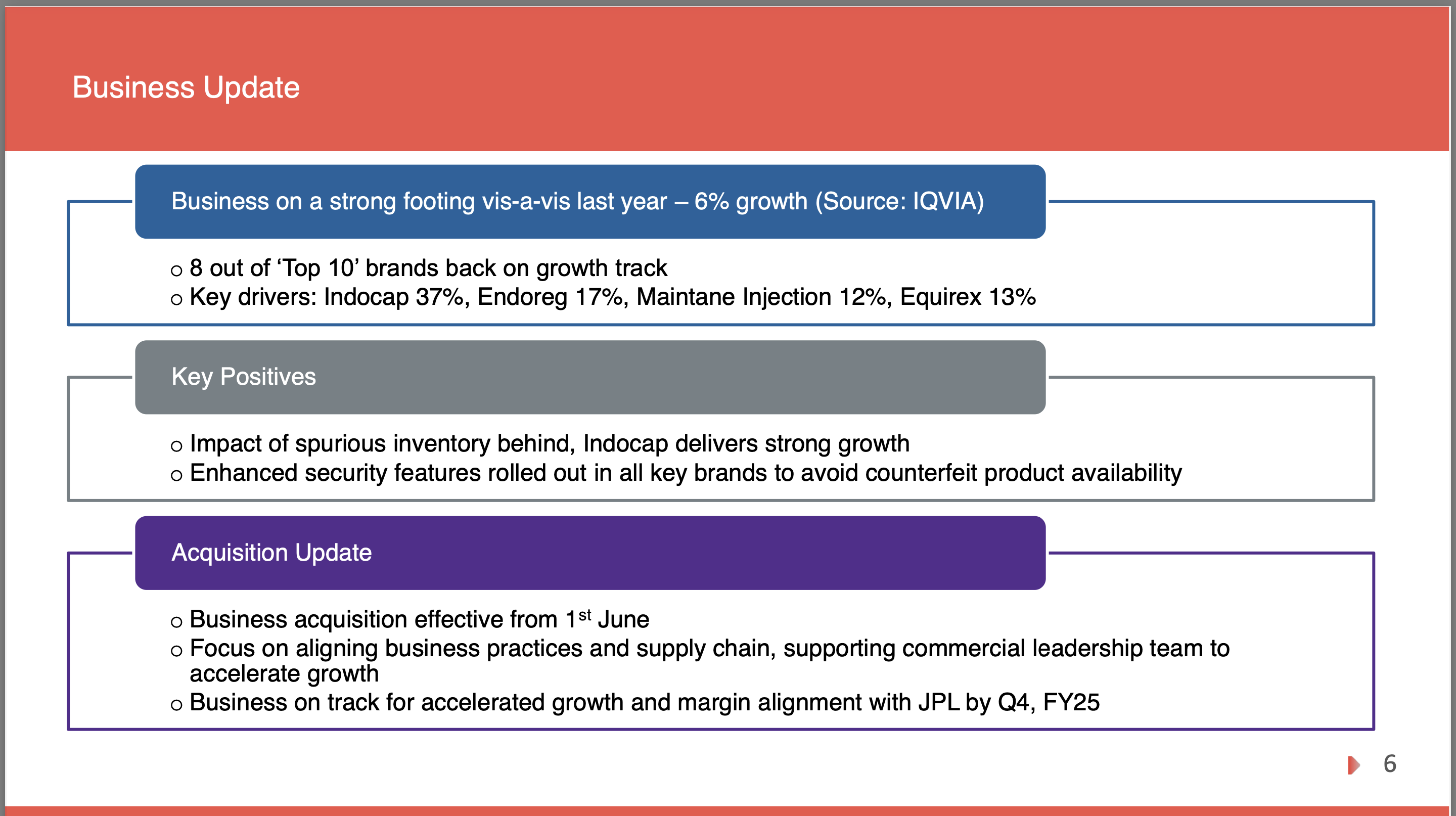

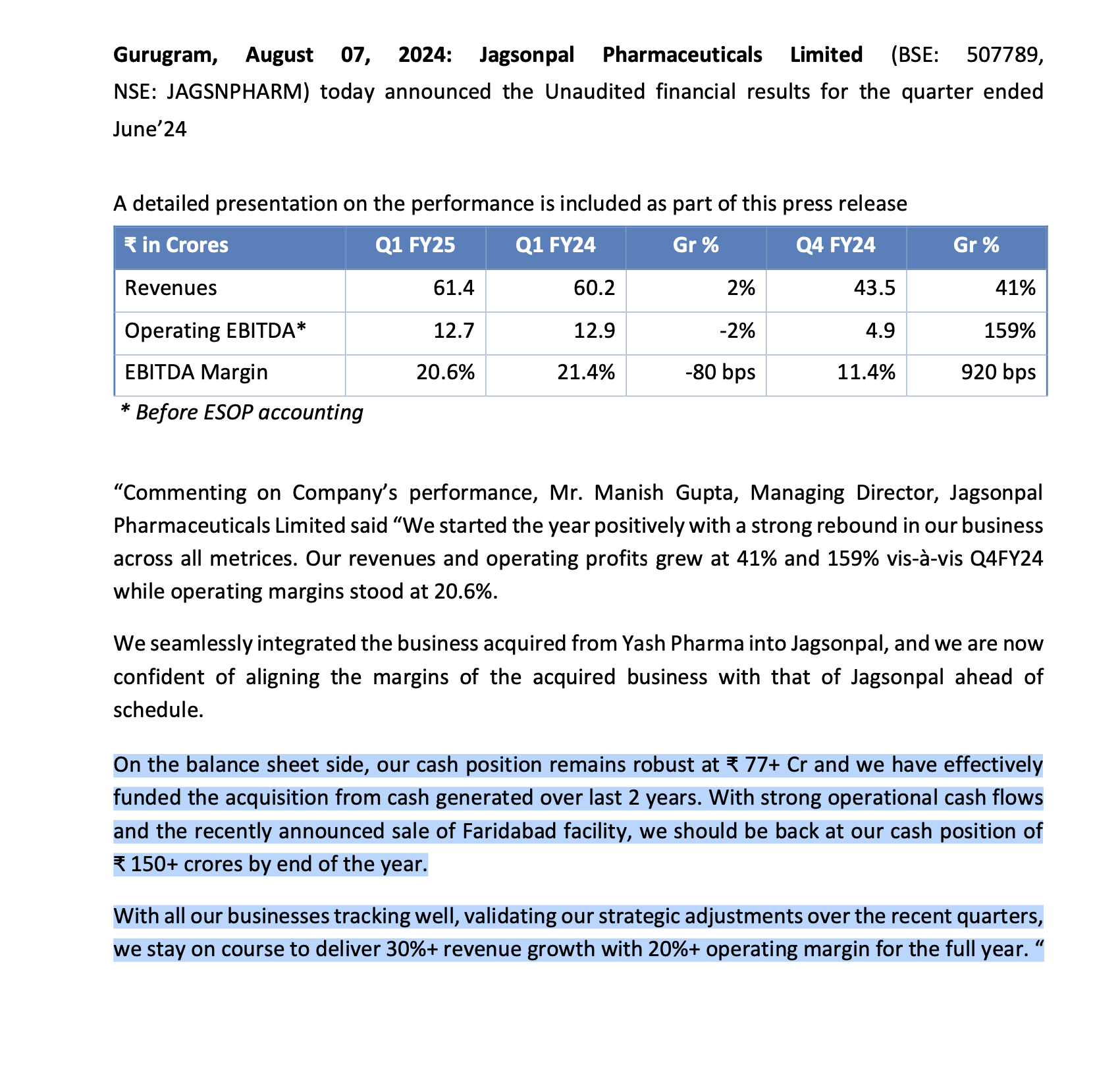

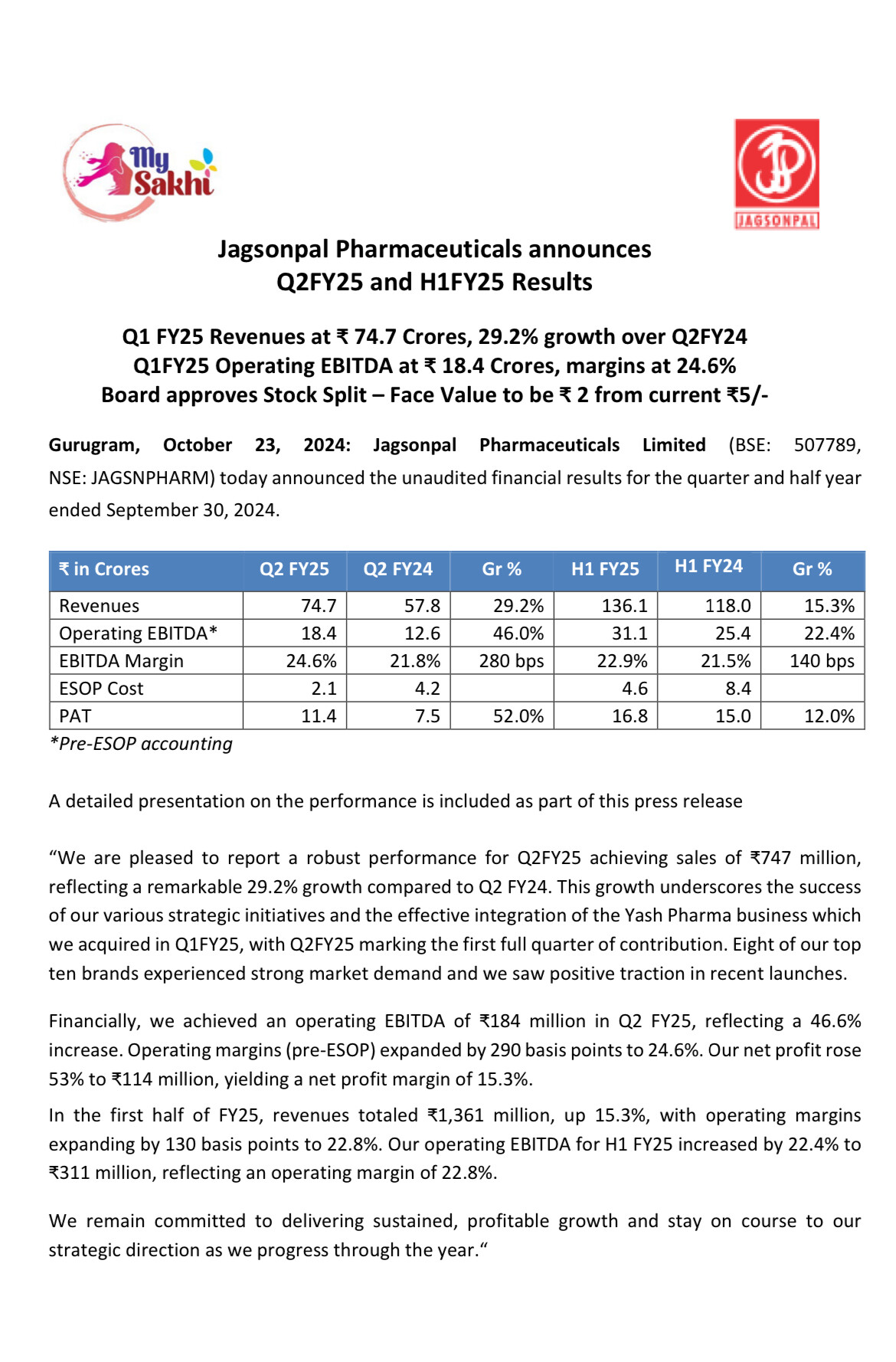

After couple of disappointing quarters, Jagsonpal Pharmaceuticals is back on the growth path. The company has reported quarterly revenue of Rs. 61.4 crores and operational EBITDA of Rs. 10.2 crores for the Q1FY25, which are higher both on QoQ and YoY basis. Net profit is Rs. 5.3 crores due to exceptional expanse of Rs. 3.3 crores incurred on acquisition of Yash Pharma.

Some interesting key points from the press release:

The company is on course to deliver 30%+ revenue growth with 20%+ operating margin for the full year which means management guiding revenue of more than Rs. 275 crores ( FY24 revenue Rs. 209 crores) and EBITDA or Rs. 55 crores for FY25 (FY24 EBITDA Rs. 23 crores).

Cash position of Rs. 150+ crores by end of the year.

Yash Pharma acquisition effective from 1st June 2024.

Integrated the business acquired from Yash Pharma into Jagsonpal, and confident of aligning the margins of the acquired business with that of Jagsonpal ahead of schedule.

From the TTM financials, the company seems to be fairly valued, however, if the aggressive growth guidance of the management are met, the stock is available at discount to the peers. Capabilities of CEO Manish Gupta in running the show and clinching acquisition at good prices, who is also holding good amount of stake in the company, is another optionality.

Board meeting is scheduled on 23rd October for Q2 results and considering stock split. But what is more interesting is that the company is hosting 1st ever concall on 24th.

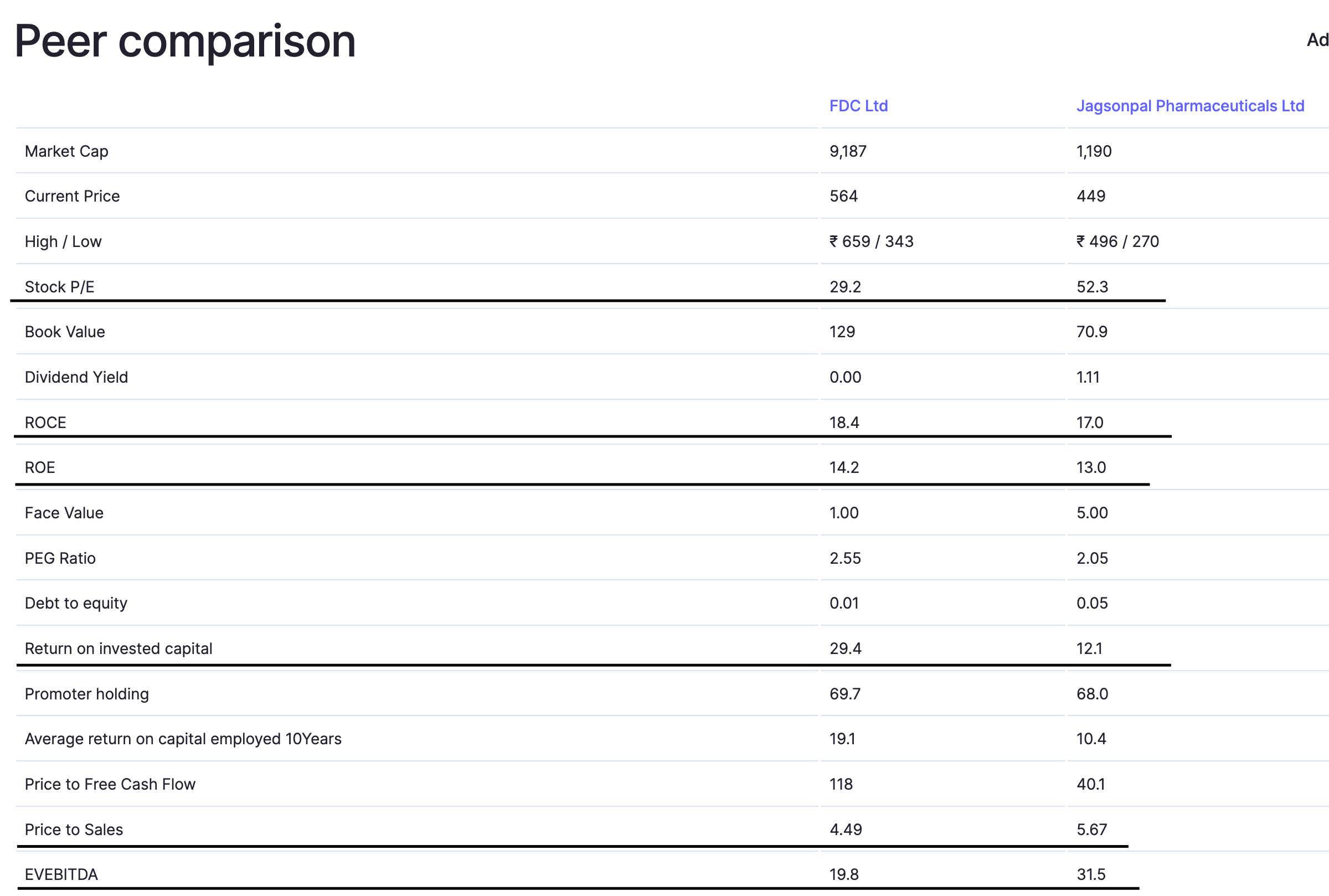

Hi, I have been following this company for the last few months. Yes, it’s a small cap with good growth prospects. But I don’t understand its hefty valuations.

Check its peer-to-peer comparison with FDC, which already has vast brands like Electral.

Looking at trailing might not be ideal in this business in particular. They have had a very bad FY24 due to multiple reasons and lead to abnormal PAT and PAT margins. Earnings were depressed. If you get a good sense on the forward numbers and estimates, valuations are still inexpensive. I dont know exactly what the FDC forward numbers would be like, but my sense is that the forward PE for Jagsonpal is still low compared to peers.

I think manish Gupta is in key managerial personal category as he is a director

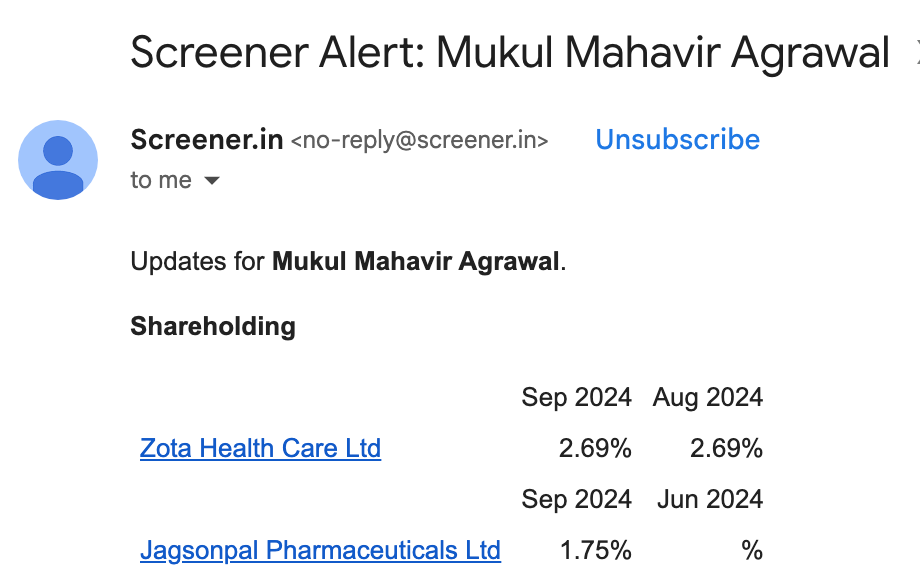

Mukul Agarwal name was not there in jun quarter but appeared in September.As he is very long term investor he is still holding