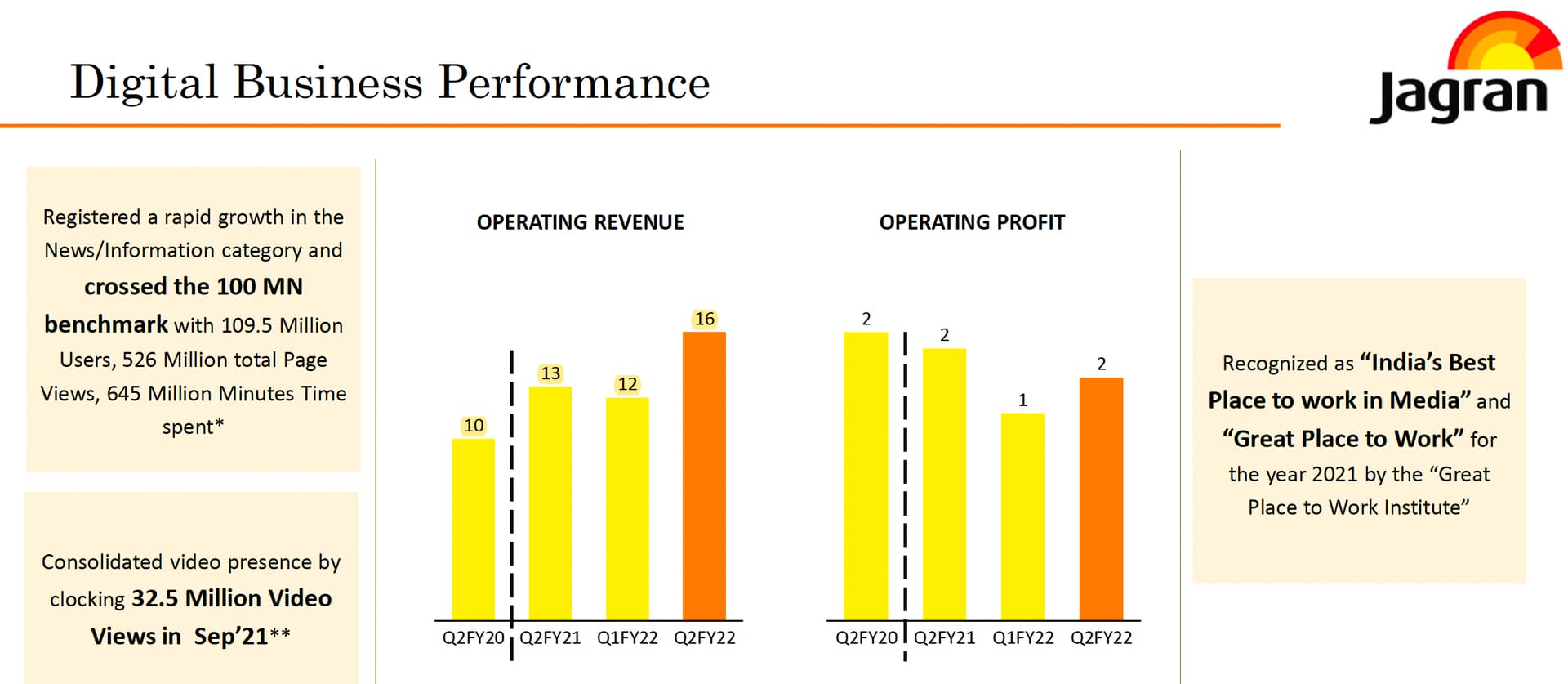

Jagran reports their online sales numbers. They are still small but growing. This is a number which should definitely be tracked.

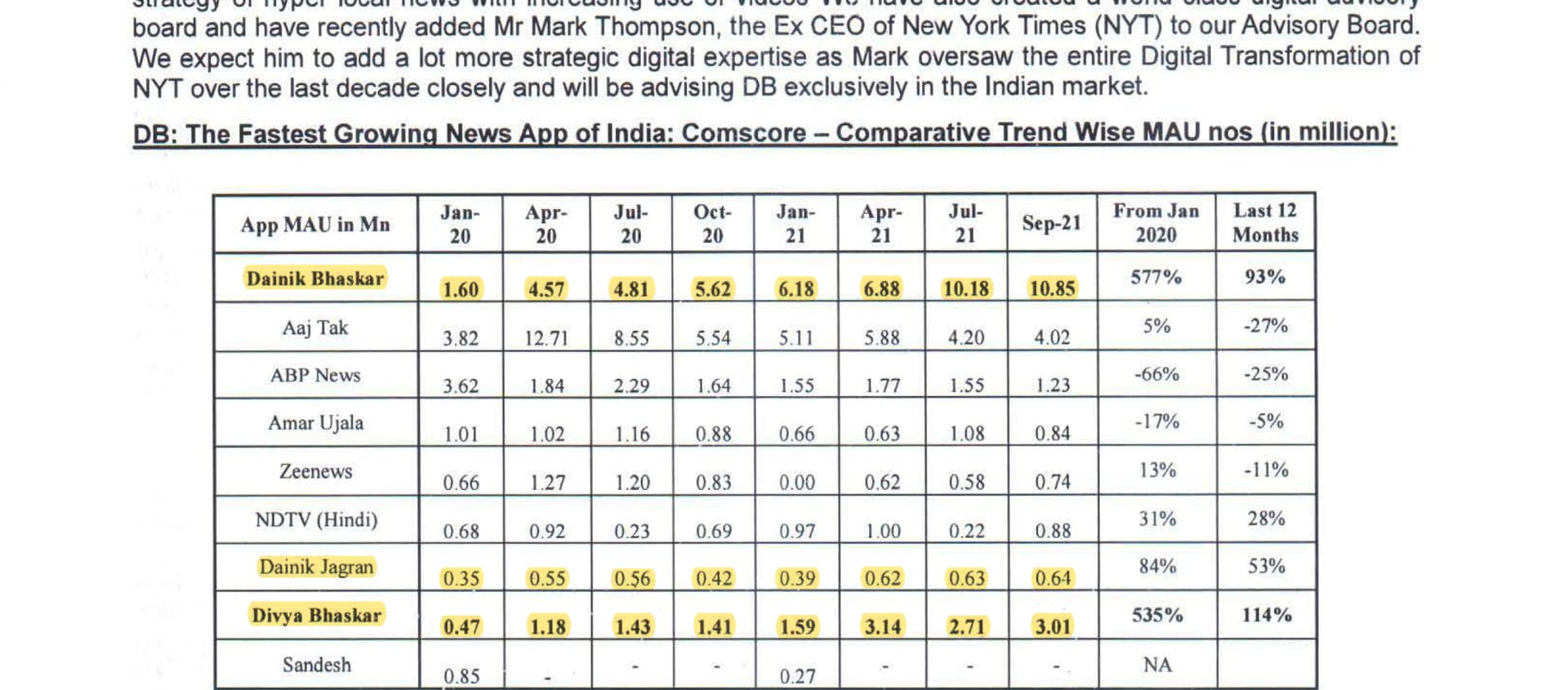

DB Corp shared monthly active users across major regional (including hindi) news and media companies in India in their last update. This might be a more appropriate benchmark and reflect economic potential of different apps. In this, DB seems to be doing exceedingly well. At the same time, dainik bhaskar doesn’t appear in the top grossing list, where jagran finds a mention. We can ask about this divergence in the next concall.

Disclosure: Invested in both DB Corp and Jagran as deep value opportunities (position sizes here)