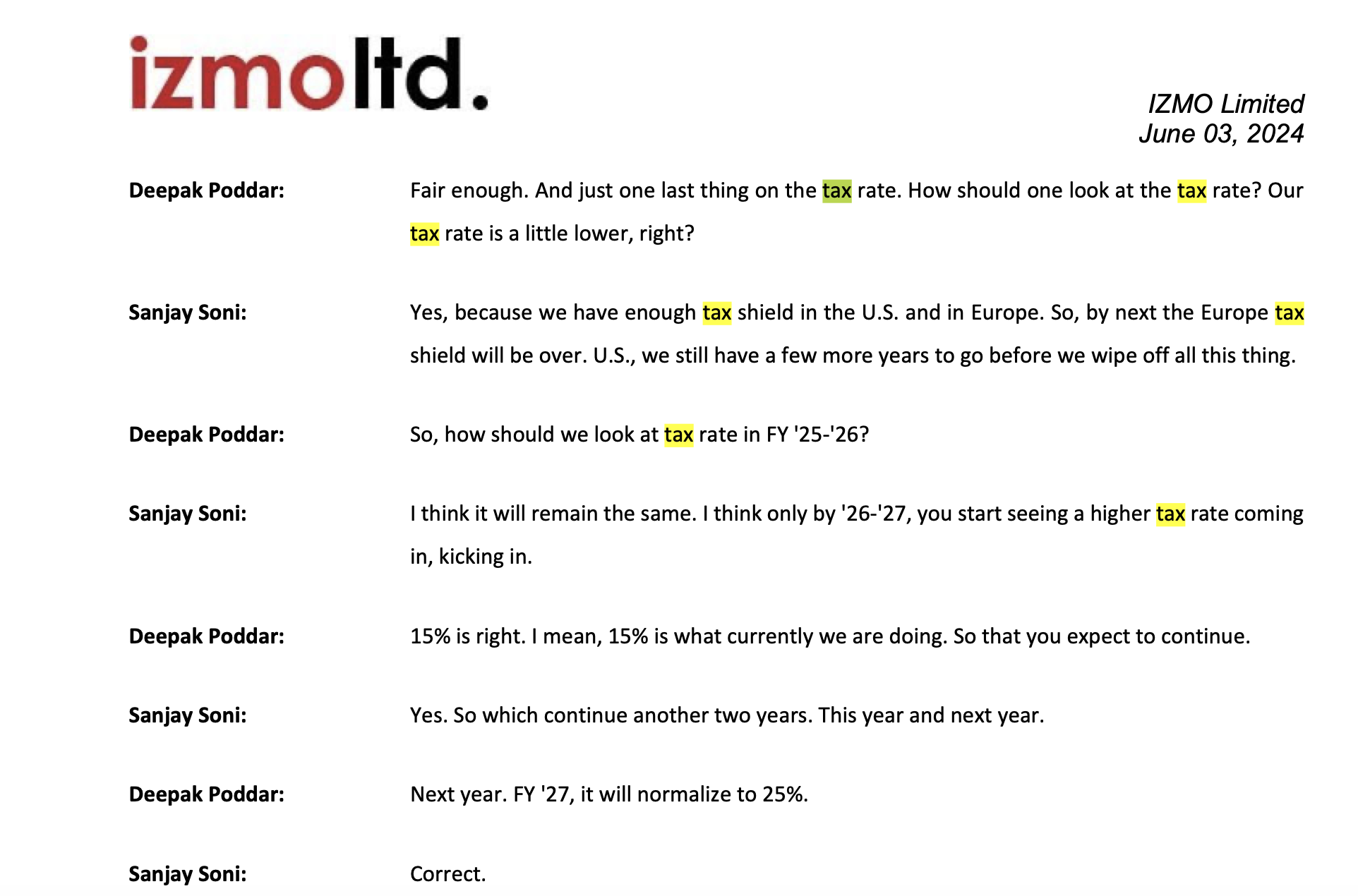

Also one question I would like to ask here? (Its a bit naive, don’t mind)

Why is the tax rate % for Izmo so low?

Also one question I would like to ask here? (Its a bit naive, don’t mind)

Why is the tax rate % for Izmo so low?

Since yesterday HFTs have became active at the counter. CMP has gone nuts in past week, is it only me who thinks information is scarce on IZMO ?

Anyone with more information on recent price movements ?

D-Holding.

Any insight on Arcstone the Mauritius based institutional investor in the company. The fund is a small cap fund has currently has only 1 other portfolio company. Margins have shown wild swings with disporpotionate changes in margins at different levels. Can see auditors comments on uncertain tax positions, 100% of loans given to RP - repayable on demand or without specified repayment terms etc. See these as red flags - would appreciate insights.

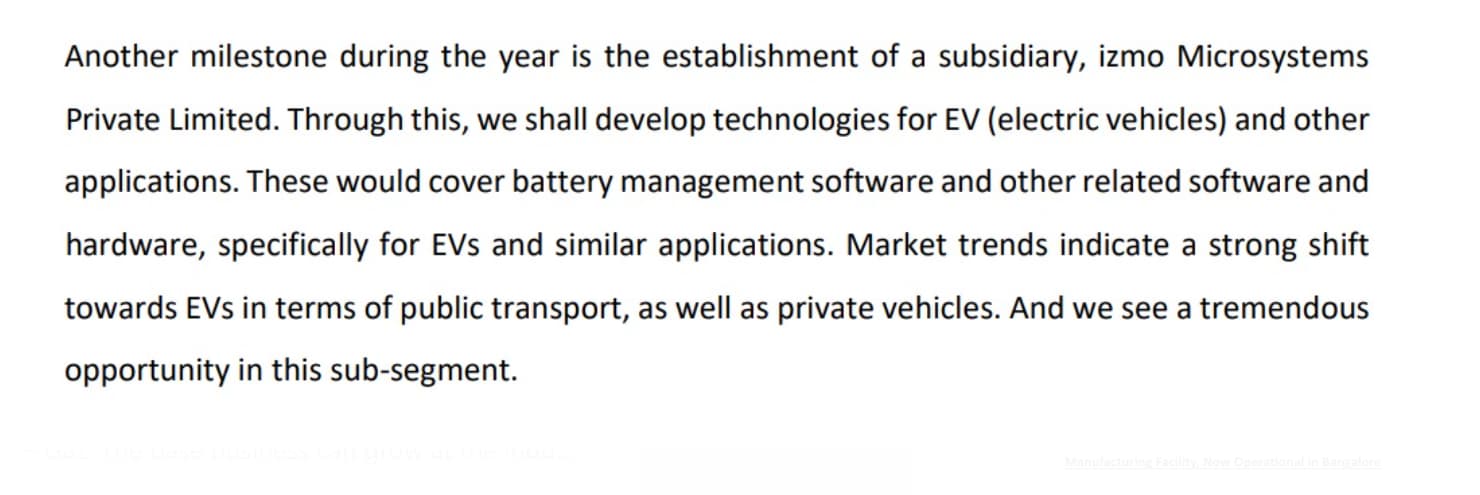

izmo Ltd. Launches izmo Micro: India’s Leading System-in-Package (SiP)

Manufacturing Facility, Now OperaƟonal in Bangalore.

Entering into Semiconductor space

In June call they were talking about this subsidiary being for EV/BMS etc…Some quick turnaround of thought process and execution !! Maybe the biggies like Kayanes, Tata’s should learn from them.

Izmo is the company that made my realize that a stock’s true value unlocking rests on a good PR. Their IR adfactor is not doing a good job IMO.

Highlights from their recent Q2 FY25 con call that makes me believe stock is significantly undervalued at the current valuation

Few other things that have improved in Izmo

Founder stake has improved to 35% with promoter mentioning maybe in future to 40% depending upon availability of funds

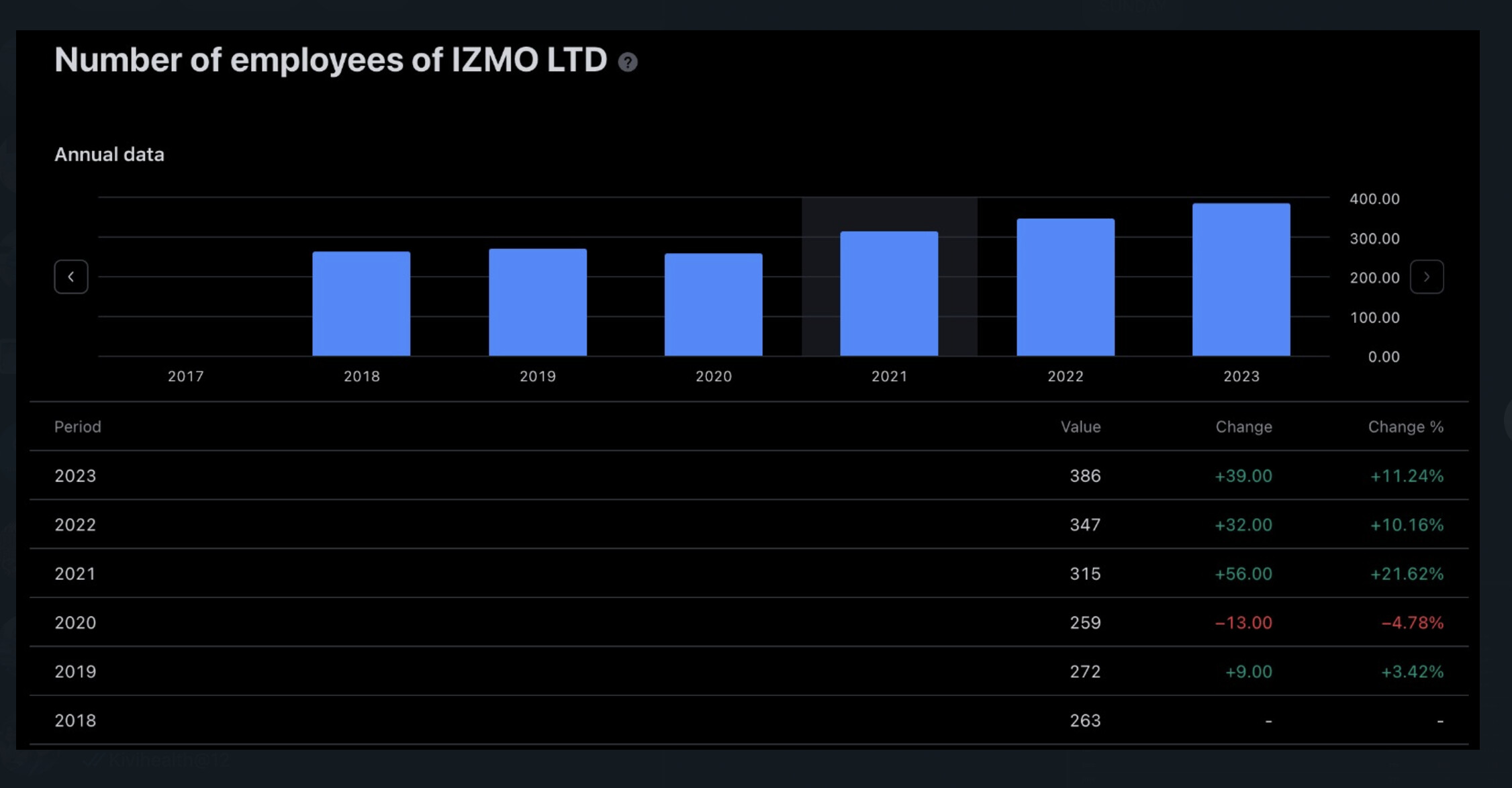

Number of employees have been constantly increasing with last number in July 2024 being 398

Geronimo acquisition has given it markets of UK, Brazil and Argentina and also Ford as a customer to which they want to cross sell

SIP assembly new division and Frog AI make this company a very interesting company

the management since the past 1-1.5 yrs were saying they were looking to raise funds for frog data but now they want a higher valuation when the market is looking weak for the foreseeable future.

Also jumping on hot sectors first in defense now in AI and EV components makes me believe this is a bull market story.

I was also wondering the same. Did you get the answer?

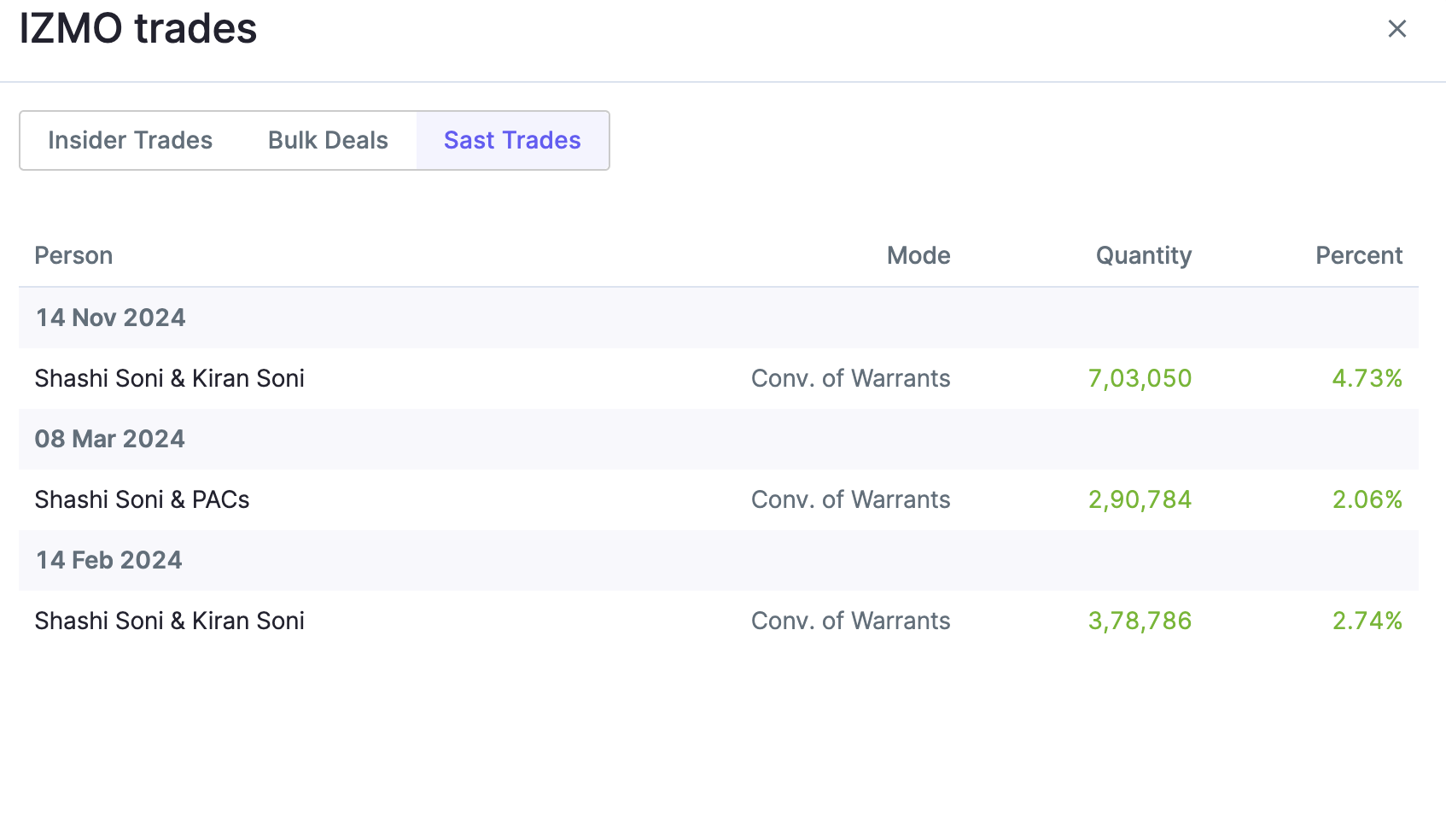

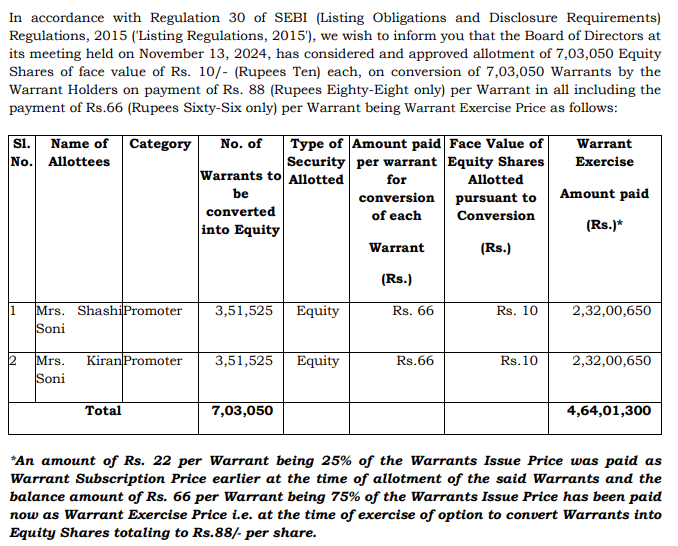

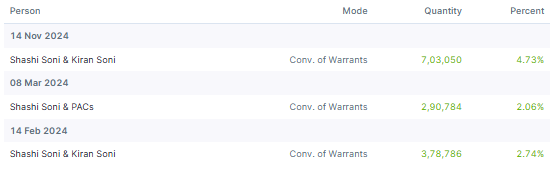

The warrants were issues at 88 which was almost at 75% discount to the share price that time. The last time it traded at 88 was in 2022. What do you think of it? How should this be taken as?

To me this looks normal practice, when the company anticipates continued growth.

This can boost liquidity and increase market visibility.

But basically its dilution and its to be watched if insiders start selling.However if we look at promoters holding it appears they are continously buying instead of selling.

@Vineetjain111 @Vidhyut_Bhawnani

Afterall if izmo is doing 500 cr FY 25 and insiders now owning 45%. I am only seeing positives…may be because i am holding it ?

However even after holding for 2 year i still dont have a clue about it growth outlook ![]()

![]() .

.

Thanks for your inputs…Can you also help me understand

This is what management had to say about tax rate in their concall

They have working relations with many OEM, they might be able to crack a few deals. But it is a completely new vertical and so management execution needs to be seen. Moreover the management have been poor in executing their guidance. So I will take their guidance in the new semiconductor business with a pinch of salt.