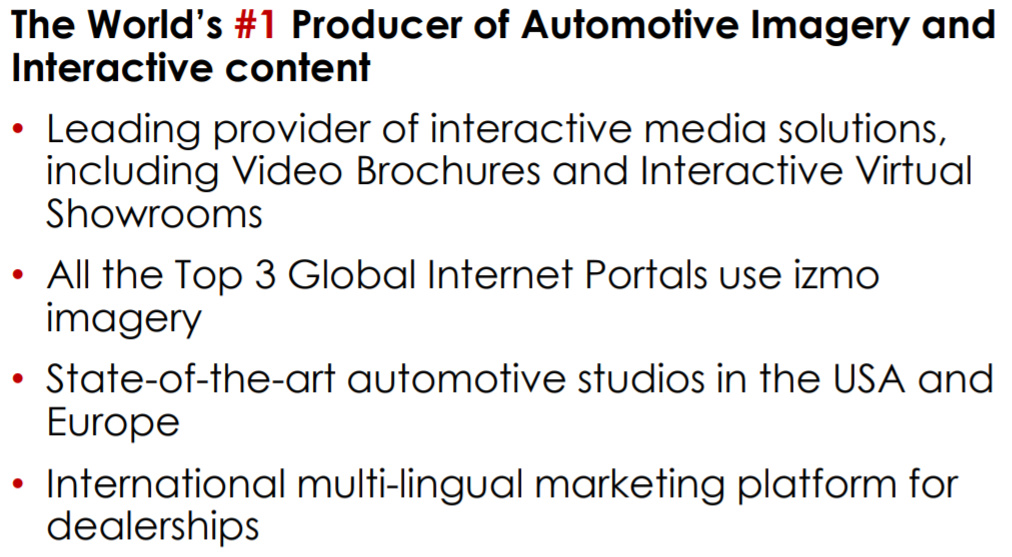

According to Bloomberg : Izmo Limited provides automotive e-retailing solutions. The Company offers interactive online stores, car animation and graphics, online marketing programs, sales performance coaching, customer relationship management solutions, and online service management solutions. Izmo serves customers worldwide.

According to Company : izmo ltd. is the world leader in interactive marketing solutions. The company offers hi-tech automotive e-retailing solutions in North America, Europe, and Asia.

Why the buzz?

Featured in Financial times- Statista 1000 high growth companies in 2018 link

Consumer demographics of auto buyers is changing and thus the buying behaviour is also changing (Global research & AC Nielson Research for India) so online will continue to dominate and here the imagery section of the company will benefit

The dealership experience influences the buying decision a lot and this point of sale is where the company’s VR product can be a gamechanger (Read Human experience section on this article published by PwC under the 5 trends transforming the automotive industry.

IZMOstudio is the digital interface that the company intends to sell to dealers which is like a cardekho.com but at a dealer level so if someone visits the dealer website they will be able to provide Big data to the dealer about the consumer trends

Caters largely to developed markets where these concepts are more likely to be accepted and are marketable.

Tie ups with Global car makers and a company claimed market share of 25% in Mexico and 12% in France with rapid expansion plans across Europe

Cons:

The threat of shared mobility (ride sharing, bike sharing etc)

Adoption of technology by Indian dealerships

Many digital channels competing for consumer attention with requisite information about products

Capex plans for Defence sector may be a drag on financials

They think that they should be valued at 10x sales… comparing themselves to likes of top SAS players

Look at their arms and ammunition projection… looks like they will be billion dollar company by 2020. Their presentation stating that they will get ammunition project license by April 2018, and small arms project license by June 2018. It’s july now, whats the status for both of these projects? I couldn’t find update on google search or company’s PR. You know about these?

No I don’t buy their forecasts or for that matter any forecasts, I am just trying to see whats in the business model that is making their revenues rise and are their any other issues that I am missing.

Business sounds very interesting considering future. Also they are stepping into defence sector? I see that is very different from existing business model as they are planning to manufacture defence equipments.

Also went through past shareholding pattern of 17 and 18. Many big shareholders and funds reduce the stake in company. Any thoughts on that?

-upbeat management commentary in Q1’20 results. The company added 9 new clients in Q1’20 and 38 clients in Jun’20 so full impact will be in upcoming quarters.

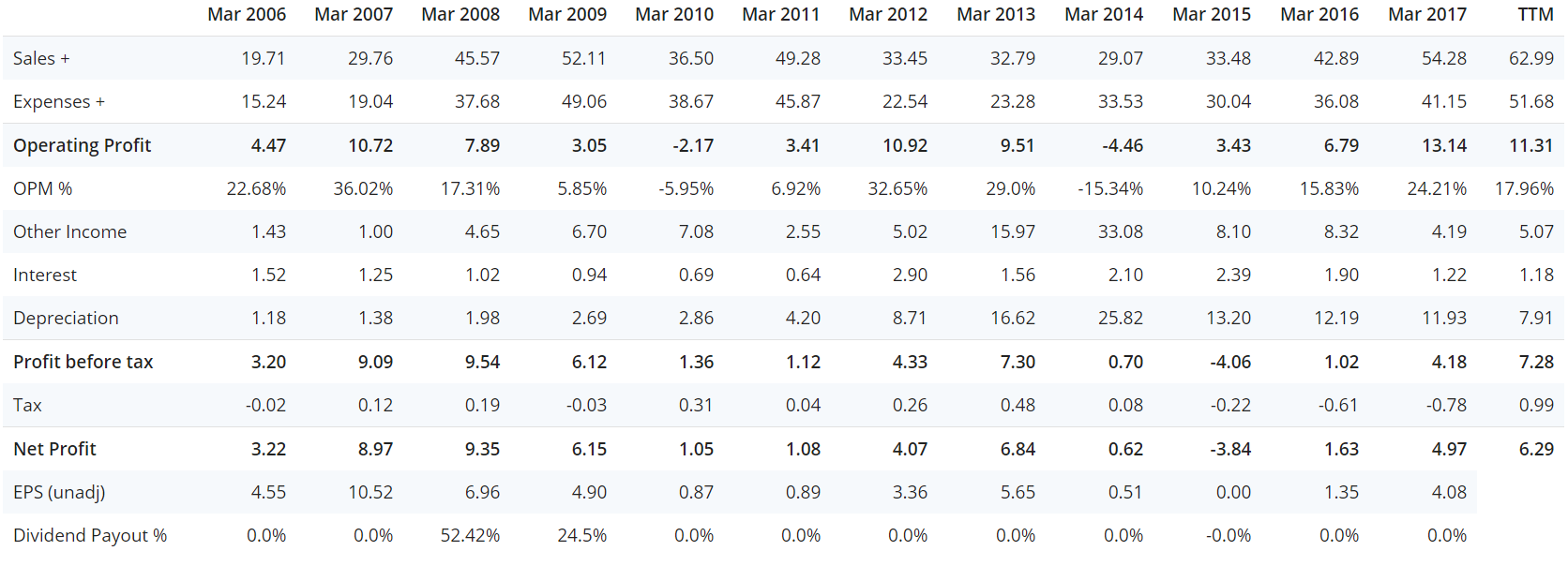

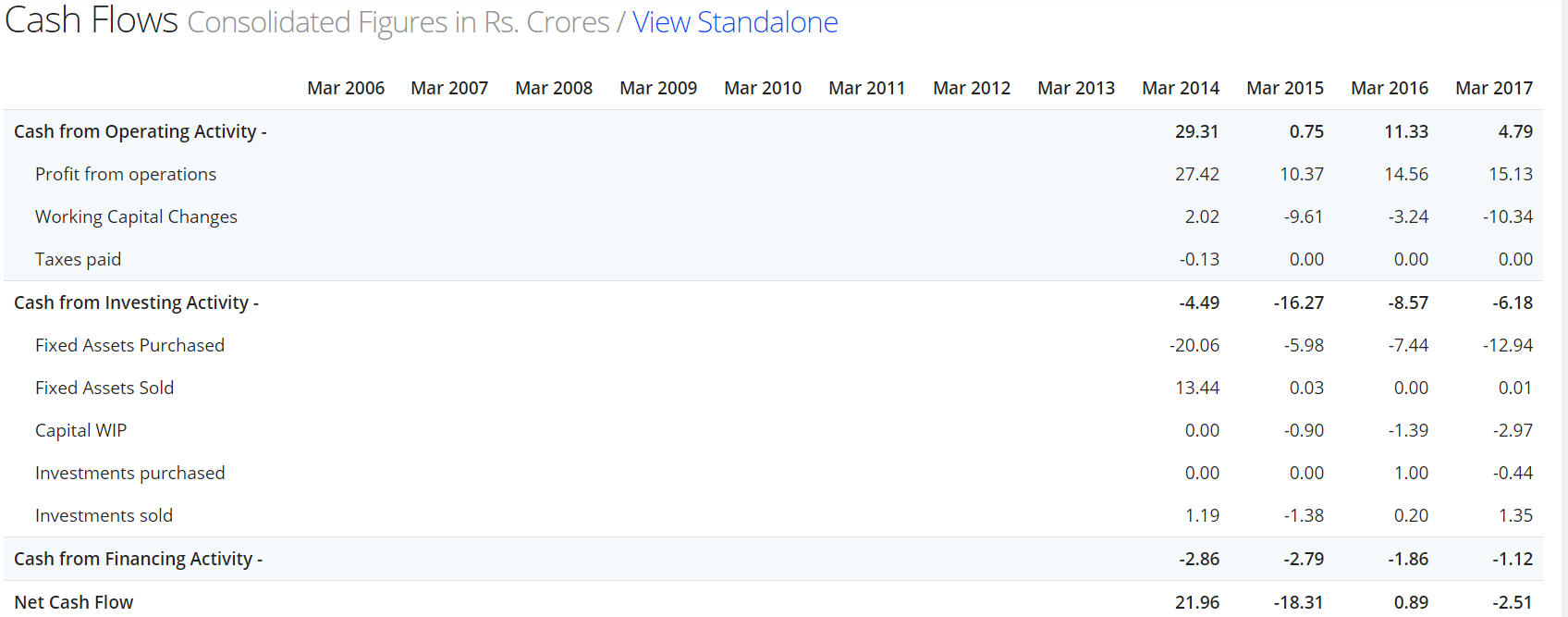

company’s annual operating cash flows close to current market cap.

Issues are as follows:

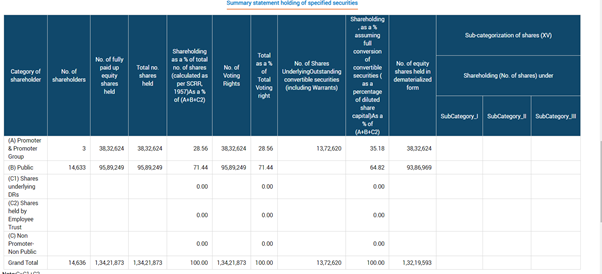

-low promoter holding at ~30%,

-the company has high intangible assets with net book value at INR 208 crs and lower amortization per year.

-contingent liability exposure towards income tax for transfer pricing

I am trying to find out revenue from defence manufacturing. The facility to manufacture ammunition was set up last year but do not see any revenue out of it.

Does any fellow boarder can put more light on IZMO ammunition manufacturing business.

It doesn’t seem to be a Izmo subsidiary as per their annual reports. Also if you go to Hughes website, it is mentioned that “The company is a part of the Deep Group, an INR 3 Billion diversified business conglomerate with interests in global automotive marketing, emerging technologies like data analytics and virtual retailing, IT solutions and services, micro electronics and electronic sub systems design and manufacturing, heritage artifacts, and more.”

I think hughes precision manufacturing is part of same group but it is not a subsidiary of IZMO. However there are related party transactions and both companies have some director in common.

Any statement by management highlighting the ever declining promoter holdings? Company has decent financials along with great business model + great current and future prospects. The developments in the company is something I would want in all of my invested companies. However, the declining shareholdings of the promoter is what is not allowing to to invest in the company.

If promoters are not able to continue believing in their story, how can we! Would love if someone can correct me here if I am missing something.

Directors of Hughes Precision Manufacturing Private Limited are Sanjay Soni, Jay Prakash Susheel Kumar Saraff, Ved Prakash Soni and Susheel Kumar Govindram Saraff.

The ‘largest repository of auto images’ > Can it not be commoditized by AI image generators. Anyone can generate any auto image they want now using AI. What’s the advantage of a repository?

On May 19, 2023, the company had approved the issuance of warrants convertible into equity shares. As per BSE’s shareholding pattern, upon conversion of the said warrants, the promoter holding would increase to 35.18% (current: 28.56%).

Seems like a positive step towards increasing their skin in the business.

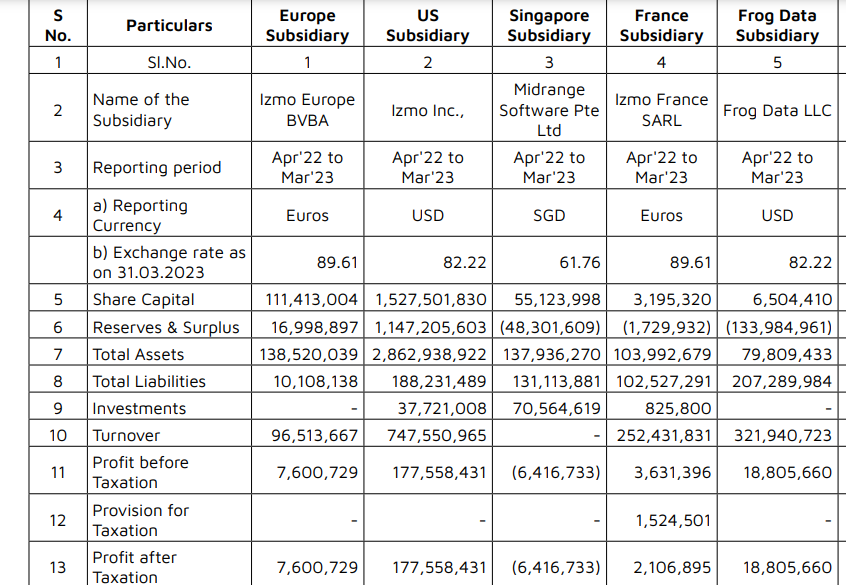

As per the FY23 annual report, Frog Data currently contributes 20% to the topline, however, it contributes only 10% to the PAT, as it has lower margins (NPM of 5.8%). This will be a key monitorable.

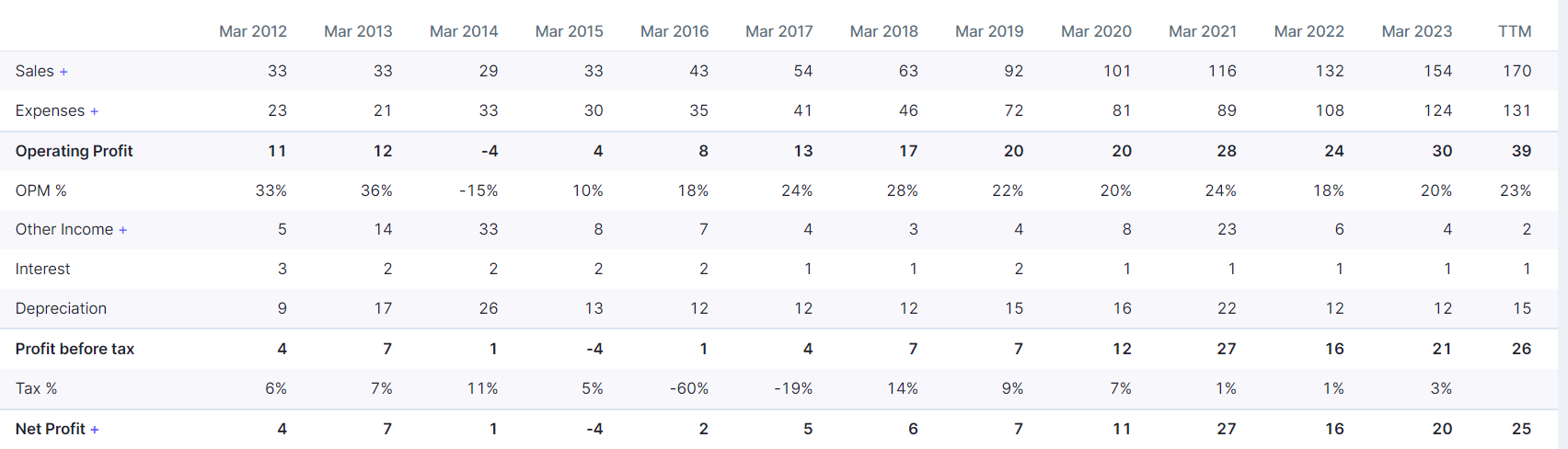

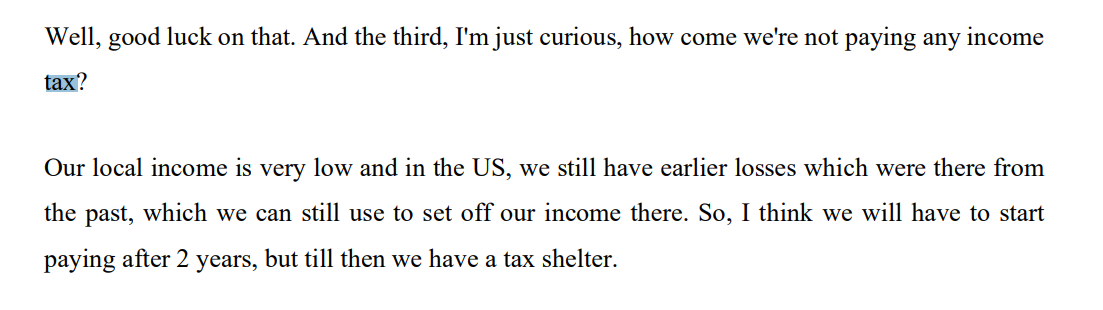

The company is not paying substantial tax as of now, and as per the management they have another 2 years of tax shelter left. Post that, the net profit will have an impact.

However, the company is currently at INR 300 cr market cap, with a P/E of 12-13x (vs median Industry P/E of ~40x) and they have guided 25-30% growth this year for IZMO Ltd.

Frog Data contributes to ~25% of sales (as of H1-FY24), and if they manage to raise private capital in Frog Data at INR 650-800 cr valuation ($80-120 million) as suggested by the promoter, the rest 75% of the business would effectively be available to the shareholders for free. (the deal is expected to be closed by March’24 as per the management).

Does anyone have a good understanding of their Frog data Platform? if one has to believe management, this company sure looks like a no-brainer buying opportunity.

I recently bought few shares to just track and looking to understand their product offerings in a bit more detail.