iValue Infosolutions: Securing the Digital Frontier

CMP: ₹274

Implied Market Cap: ₹1477 crores

FY25 PAT: ₹85.3 crores

PE: ~16.2x

Tracing the Origins:

The story of iValue began in 2008, rooted in a major shift within the Indian IT landscape. A group of approximately 40 professionals, originally part of an organization that had been acquired by Wipro, decided to move out of the Wipro entity to forge their own path. Led by Sunil Kumar Pillai, Krishna Raj Sharma, and Srinivasan Sriram, this team founded iValue Infosolutions with a core DNA focused on Cybersecurity.

In the early days of Indian IT transformation, while many focused on general hardware, this team identified that the future of large enterprises would be driven by digital applications. They realized that for these applications to succeed, they needed to be “wrapped” in a layer of performance, availability, scalability, and security (PASS). What started as a specialized Value-Added Distributor (VAD) has since evolved into a “Technology Enabler” that bridges the gap between global technology giants and complex local enterprise needs.

About the Company:

iValue Infosolutions is an enterprise technology solutions specialist that secures and manages digital applications and data. While its heritage is in cybersecurity, the company has expanded into Information Lifecycle Management (ILM), Data Center Infrastructure (DCI), and Application Lifecycle Management (ALM).

The company serves as a critical link in the technology ecosystem:

- OEM Partners: It maintains a network of 101 Global OEMs, including industry leaders like Check Point, Forcepoint, Hitachi, Arista, and Google Cloud.

- Channel Network: It partners with over 648 System Integrators (SIs), ranging from Global SIs like Hitachi and Sify to local specialists.

- Core Verticals: Its primary business driver is Cybersecurity, which accounts for over 50% of its gross sales.

What They Exactly Do:

iValue acts as a “Technology Enabler” rather than a traditional box-seller. They work with SIs to understand the business requirements of large enterprises and then curate multi-OEM technology stacks.

- The “PASS” Philosophy: Every solution is designed to ensure digital applications have the necessary Performance, Availability, Scalability, and Security.

- Multi-OEM Stacks: They have developed over 30 ready-to-deploy stacks (e.g., for BFSI, e-commerce, or cloud security) that ensure products from different vendors work seamlessly together.

- Managed Services: Through their subsidiary ASPL, they provide 24x7 managed services, monitoring IT infrastructure and security via their own Security Operations Centre (SOC).

What is the Strength of iValue?

- Diversified Clientele & Retention: They served over 2,000 enterprise customers in FY24, with a high System Integrator retention rate of approximately 71%.

- Intellectual & Technical Capital: Over 50% of the workforce is technical, holding 583 OEM certifications.

- iValue Centre of Excellence (CoE): A hybrid cloud-based platform that allows customers to test and finalize multi-OEM solutions before making a purchase.

- iAcademy: To combat industry-wide talent shortages, they launched an in-house training program that inducts recruits directly into specialized roles.

- CLCA: A key strength is its Customer Life Cycle Adoption (CLCA) platform. This homegrown analytics engine tracks the digital transformation stage of every customer. It allows iValue to predict exactly when a customer will need a “tech refresh” or a renewal, enabling them to cross-sell and up-sell the right solutions at the right time. This acts as a major offset to the lack of a formal long-term order book.

What is the Opportunity Size?

The Total Addressable Market (TAM) for their core segments (Cybersecurity, ILM, DCI, ALM) is experiencing explosive growth.

-

Indian Market Growth: The TAM in India is expected to grow from USD 22.7 billion in 2024 to USD 63.1 billion by 2029, a CAGR of 22.6%.

-

Government Push: Initiatives like Digital India and stringent data residency laws are forcing enterprises to invest heavily in information lifecycle and security management.

-

Tremendous Market Momentum: The Indian data center infrastructure and management market is forecasted to experience massive growth, with an expected CAGR of 32.7% from 2024 to 2029. This is significantly higher than the projected growth for cybersecurity or information lifecycle management.

-

Shifting Landscape: As enterprises move toward hybrid clouds and hyper-converged infrastructure, iValue is positioning itself as the middleman for advanced solutions like software-defined data centers and sustainable “green” data centers.

-

High-Power Computing: The rise of AI and big data in India is driving a desperate need for high-power computing platforms, which directly fuels demand for iValue’s DCI stack.

Pricing Power and Competitive Intensity:

- High “Stickiness”: Because iValue’s solutions are integrated into the core digital infrastructure of an enterprise, they are difficult to replace based on price alone.

- Consulting vs. Distribution: Unlike volume-based distributors, iValue uses a “consulting approach” with SIs, focusing on business needs rather than simple resale.

- Niche Position: While they face global competition, iValue’s deep local network and pre-integrated multi-OEM stacks provide a significant competitive moat in the SAARC and Indian regions.

Entry Barriers:

- Technical Credibility: It takes 1–2 years to gain technical expertise on new global tech before a vendor allows a partner to go to market.

- The Trust Flywheel: Winning the trust of both Global OEMs and major SIs requires years of proven execution and technical support.

- Certification Moat: Global OEMs require high levels of technical certification, which iValue manages through its scale and iAcademy.

What Can Be the Anti-Thesis?

-

Confusing Accounting Policy Change: The company moved from a “gross basis” to a “net basis” for software sales. While this has zero impact on the bottom line (PAT), it dramatically changes the top-line appearance. For example, in FY24, the “Gross Sales Billed” was ₹21,104 million, but the reported “Revenue from Operations” on the books was only ₹7,802 million. This makes historical comparisons and growth calculations difficult for the average investor to track.

-

No Revenue Visibility/Order Book: Unlike traditional IT service players, iValue does not maintain a formal “order book.” Their business is driven by non-exclusive, short-term contracts (1–3 years) that can be terminated “without cause” on as little as 10 to 60 days’ notice. This lack of long-term visibility makes the revenue stream inherently more volatile and less predictable.

-

OEM Concentration: The top 10 OEMs account for a significant portion of gross sales (~65%). Any disruption in these relationships could be material.

-

Talent Attrition: The company faces a high attrition rate, reflecting the intense competition for skilled IT professionals.

-

Contract Terms: Agreements with OEMs are often non-exclusive and can be terminated with relatively short notice.

IPO Structure and Promoter Divestment:

- 100% Offer for Sale (OFS): The IPO consists entirely of an offer for sale of approximately 18.7 million equity shares.

- The PE Exit: Creador, the primary investor, is using this IPO to facilitate a significant exit.

- Promoter Divestment: All three original promoters—Sunil Kumar Pillai, Krishna Raj Sharma, and Srinivasan Sriram—are selling a portion of their stakes.

Core Business: The “PASS” Framework

iValue differentiates itself from traditional distributors like Redington or Ingram Micro by acting as a Value-Added Distributor (VAD). They don’t just move boxes; they provide the “glue” that makes enterprise applications work.

The “PASS” Philosophy:

Every digital application (like a banking app or e-passport system) requires four pillars to survive, which iValue calls PASS:

- Performance: Ensuring the app doesn’t lag.

- Availability: Ensuring 99.9% uptime.

- Scalability: Handling 1,000 users today and 1,000,000 tomorrow.

- Security: Protecting the data (the core DNA of the company).

Four Key Technology Verticals (H1 FY26 Revenue Mix):

- Cybersecurity (48% of Gross Sales): The anchor vertical. Focuses on identity management (CyberArk), network security (Check Point), and analytics (Splunk/Google Chronicle).

- Information Lifecycle Management (ILM) (25%): Managing data from creation to deletion. Includes storage and backup solutions (Hitachi Vantara, Cohesity).

- Data Center Infrastructure (DCI) (12%): The fastest-growing vertical (+71% YoY). Provides the “private cloud” infrastructure (Nutanix) for enterprises wary of public clouds.

- ALM & Cloud (14%): Helping developers secure code as they build it (DevSecOps).

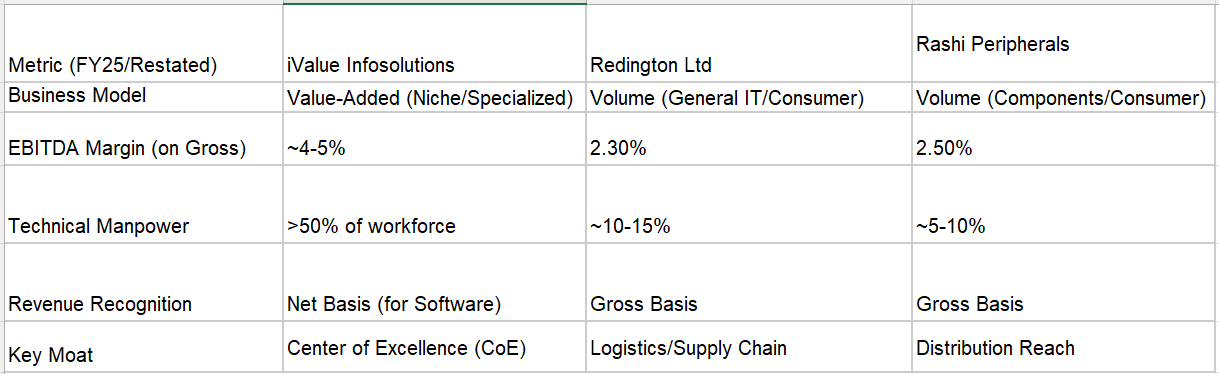

Peer Comparison: Value vs. Volume

The market often confuses iValue with volume distributors. However, their financial profile and business model are structurally different.

The Margin Difference: Because iValue acts as a “Technology Enabler,” they earn higher margins per deal. While a general distributor might make a 2-3% margin selling a laptop, iValue makes significantly higher margins by curating a multi-stack security solution that requires 1-2 years of technical certification to even sell.

Recent Management Guidance (Q2/H1 FY2026)

In the latest earnings call (Nov 2025), management highlighted that Q2 was the best quarter in the company’s 18-year history.

- Financial Growth: Gross sales grew 34% YoY in H1. PAT grew 43% YoY, showing positive operating leverage as they scale.

- Massive Pipeline: Management guided for a Q3 FY26 pipeline of ~₹2,500 Crores (on gross basis). This suggests that the current growth momentum is not just a “one-quarter wonder.”

- Annuity Momentum: 42.3% of their business is now “annuity-led” (renewals/TCO-based). This provides a significant cushion against the “no order book” risk discussed earlier.

- The AI Tailwind: Management is seeing a surge in demand for High-Performance Computing (HPC) and AI-Ready Infrastructure, which is directly fueling the 71% growth in the Data Center (DCI) vertical.

- Working Capital Efficiency: Working capital days improved to 46 days, down from higher levels in previous years, indicating better collection efficiency from System Integrators.

Points of Concern

- Accounting Complexity: The shift to “Net Basis” reporting for software continues to confuse the market. The ₹922 Cr reported revenue for FY25 is actually a margin-only figure for a business that billed customers over ₹2,400 Cr. Investors must look at Gross Sales to understand the true scale of operations.

- Negative Cash Flow: Despite record profits, net operating cash flow remains tight (reported at -₹30 Cr for recent periods). This is due to the inherent working capital intensity of buying hardware from global OEMs before getting paid by local SIs.

Disclosure: Biased and Invested