This is my first thread on the Forum. I would appreciate the feedback of senior people and would also invite fellow members to research more on this company.

![]() ITD Cementation India Ltd – A Deep Dive into Its 90-Year Legacy and New Chapter with Adani Group

ITD Cementation India Ltd – A Deep Dive into Its 90-Year Legacy and New Chapter with Adani Group

Company Name: ITD Cementation India Limited

Ticker: ITDCEM (NSE) | 509496 (BSE)

Current Promoter: Adani Group (via Renew Exim DMCC)

Market Cap: ~₹11,400 Cr (as of June 2024)

Industry: Infrastructure & Civil Construction

Listed Since: 1990s

Website: www.itdcem.co.in

![]() Legacy and Historical Timeline

Legacy and Historical Timeline

-

1931: Originated as the Indian branch of The Cementation Company Ltd, UK, known for high-pressure grouting and foundation engineering.

-

1978: Incorporated in India as Cemindia Company Ltd.

-

1994–2005: Went through multiple name changes reflecting its foreign ownership:

- Trafalgar House Construction India Ltd (1994)

- Kvaerner Cementation India Ltd (1998)

- Skanska Cementation India Ltd (2001)

-

2005: Acquired by Italian-Thai Development PCL (ITD PCL), Thailand’s largest civil contractor; renamed ITD Cementation India Ltd.

![]() Core Competencies

Core Competencies

ITD Cementation is a pioneer in EPC (Engineering, Procurement & Construction) with 90+ years of experience across:

- Maritime Structures

- JNPT Phase II, Karwar Naval Base, Mazagon Dock

- Urban Mass Transit (Metro)

- Delhi Metro (CC26 – TBM record), Kolkata Metro (Hooghly River tunnel), Mumbai, Nagpur & Jaipur Metro

- Airports

- Terminal expansions at Delhi & Hyderabad Airports

- Roads, Highways & Bridges

- NH projects in Maharashtra, Tamil Nadu, Andhra Pradesh

- Hydro & Irrigation

- Saurashtra Canal, New Umtru Hydroelectric Project

- Industrial & Specialist Engineering

- Refineries (IOCL Paradip), NTPC, BS-VI upgrades, IIT Ropar Campus

![]() Leadership Timeline

Leadership Timeline

| Year | Leadership Milestone |

|---|---|

| 2000 | Mr. Sunil Singh (MD till 2009) – Steered early metro & marine projects |

| 2015 | Mr. Piyachai Karnasuta joins Board (EVP, ITD PCL) |

| 2019 | Mr. Jayanta Basu appointed as MD (joined as GET in 1986) |

| 2019 | Mr. Santi Jongkongka appointed Executive Vice Chairman |

| 2025 | Adani Group gains majority control; new board expected |

![]() Financials Snapshot (FY24)

Financials Snapshot (FY24)

- Revenue: ₹9,097 Cr

- PAT: ₹373 Cr

- 5-Yr Profit CAGR: 38.3%

- ROE: 22.4%

- P/E Ratio: ~30.6×

- Order Book: ₹47,051 Cr (diversified)

![]() Adani Group Acquisition (2024–25)

Adani Group Acquisition (2024–25)

- Oct 2024: Renew Exim DMCC (Adani Group) signs SPA to acquire 46.64% from ITD PCL at ₹400/share (deal value: ₹3,204 Cr).

- Dec 2024: Launches Open Offer @ ₹571.68/share for 26% additional stake.

- April 2025: Successfully acquires 20.83% via open offer; total holding becomes 67.46%.

- Jan 2025: CCI approval granted.

- Result: Adani Group now holds controlling interest and becomes promoter.

![]() Investment Rationale

Investment Rationale

- Robust Order Book across metros, ports, tunnels, and bridges.

- Transition to Adani Group could lead to better capital allocation, margin expansion, and order inflow from group infra projects.

- Strong execution capabilities with proven track record in complex marine and tunneling infrastructure.

![]() Risks & Monitorables

Risks & Monitorables

- Transition of leadership under new promoter (Adani).

- Execution risk due to size and technical complexity of ongoing projects.

- Working capital intensity of infra business; debt levels need monitoring.

- Any potential delisting (purely speculative at this point) if Adani increases stake further.

![]() Conclusion

Conclusion

ITD Cementation India Ltd has transformed from a legacy civil engineering arm of a British company into one of India’s most trusted EPC players. With the Adani Group acquiring a 67.46% controlling stake, a new growth phase may begin—backed by strong parentage, financial bandwidth, and access to mega infrastructure projects.

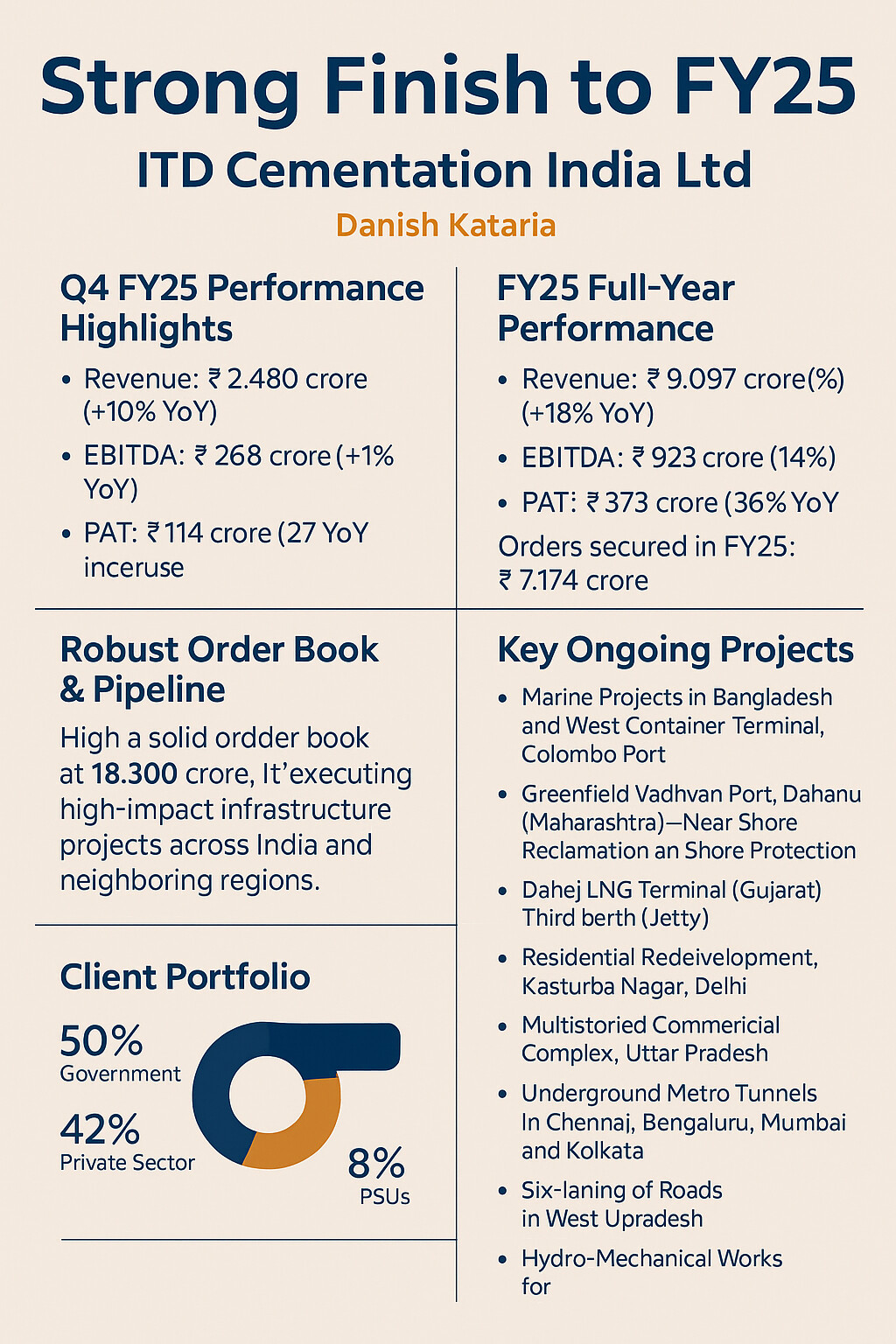

Strong Finish to FY25 | ITD Cementation India Limited Reports Stellar Growth and Project Momentum

ITD Cementation India Ltd continues to scale new heights with a strong financial and operational performance in FY25. We’re not just building infrastructure—we’re building the future of India and beyond.

Q4 FY25 Performance Highlights:

• Revenue: ₹2,480 crore (+10% YoY)

• EBITDA: ₹268 crore (+11% YoY)

• PAT: ₹114 crore (+27% YoY)

• New orders worth ₹804 crore secured this quarter

FY25 Full-Year Performance:

• Revenue: ₹9,097 crore (+18% YoY)

• EBITDA: ₹923 crore (+14% YoY)

• PAT: ₹373 crore (+36% YoY)

• Orders secured in FY25: ₹7,174 crore

Robust Order Book & Pipeline:

With a solid order book of ₹18,300 crore, ITD Cementation is executing high-impact infrastructure projects across India and neighboring regions.

Key Ongoing Projects:

• Marine Projects in Bangladesh and West Container Terminal, Colombo Port, Sri Lanka

• Greenfield Vadhvan Port, Dahanu (Maharashtra) – Near Shore Reclamation and Shore Protection

• Dahej LNG Terminal (Gujarat) – Third berth (Jetty)

• Residential Redevelopment, Kasturba Nagar, Delhi (Phase I & II)

• Multistoried Commercial Complex, Uttar Pradesh

• Underground Metro Tunnels in Chennai, Bengaluru, Mumbai, and Kolkata

• Six-laning of Roads in Uttar Pradesh

• Railway Tunnels in West Bengal and Sikkim

• Hydro-Mechanical Works for 500 MW Pumped Storage Project – Andhra Pradesh

• Micro-tunneling projects in Ahmedabad and water infrastructure in Karwar

Client Portfolio:

50% Government | 42% Private Sector | 8% PSUs

With a presence in 13 Indian states and 2 international markets, ITD Cementation is focused on timely project execution, innovation, and sustainable growth.