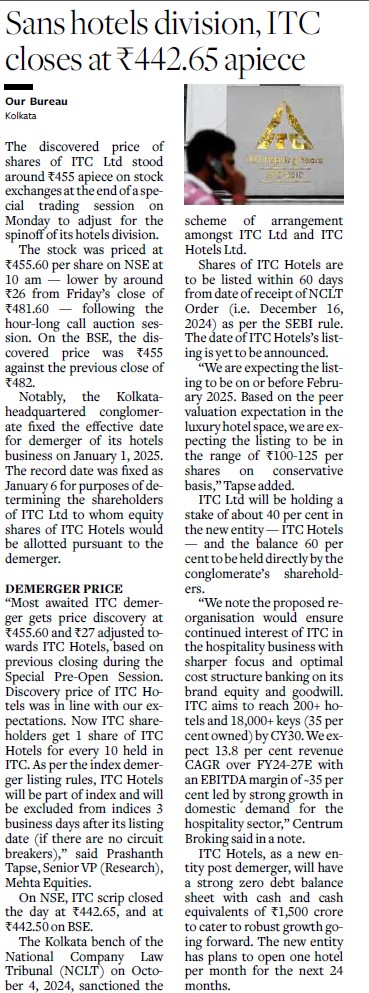

ITC Hotels Demerger: Stock price calculation, MSCI index addition

Disclosure: Invested. Have some ITC from 1-2 years back.

ITC Hotels Demerger: Stock price calculation, MSCI index addition

Disclosure: Invested. Have some ITC from 1-2 years back.

Tour and travel in India is under pressure from cheaper destinations like Vietnam, Thailand, SriLanka also many countries have made a visa free for Indian Nationals.

Goa has just experienced what it means to have empty hotels in peak Christmas season.

A 7-8 day stay in Vietnam budget with airfare works out cheaper , than spending on India.

With view of above , I would only venture in ITC hotels at < 30 PE

ITC on the other hand is a cash cow and if goes down is a better buy.

disc: Holding ITC as part of my PF since last 20 years

I completely agree with your view on the challenges faced by the hospitality sector in India. The pressure from more affordable travel destinations like Vietnam, Thailand, and Sri Lanka, especially with the added advantage of visa-free access for Indian nationals, is definitely making an impact. Goa’s experience with empty hotels during peak Christmas season further underscores this trend. It’s evident that a 7-8 day stay in Vietnam, including airfare, works out to be cheaper than staying in India.

That said, while I do acknowledge the enthusiasm around ITC Hotels, if you look at the historical trends, companies like IHCL were trading in the 20-30 EV/EBITDA range, which is more in line with the normal band. The current 50 EV/EBITDA multiple is largely driven by market sentiment rather than any fundamental change in the sector.

As you rightly pointed out, ITC’s cigarette business remains the primary cash cow for the company, and any decline in the stock price would certainly present a better entry point. The cigarette business is a key driver of the valuation, and if we are valuing ITC, a major chunk of that value comes from this segment.

I share your skepticism about the FMCG segment. It seems to have become somewhat commoditized, and the margin potential is limited. If we look at peers in the FMCG space, even the best performers are struggling to achieve EBITDA margins above 18-19%. Comparing ITC’s FMCG business to HUL doesn’t make much sense, as the dynamics are vastly different. If ITC wants to improve its margins in FMCG, it would likely need to diversify into more segments, launch additional products, and most importantly, invest more capital. The cigarette business could provide the cash flow needed to support such an expansion, but it’s clear that there is significant risk involved.

Regarding the Agri and Paper segments, they are cyclical industries that require significant capital, and while they do contribute to the free cash flow, their growth potential remains limited. As for ITC Infotech, I agree that its relevance is unclear in the larger picture. Perhaps it could be more valuable if sold to a specialized IT services company or, ideally, demerged to unlock value.

In conclusion, while I remain cautious about ITC’s growth prospects in the FMCG segment, the valuation of the stock is still largely driven by the cigarette business. The stock remains an attractive buy, especially if it corrects, as the cash cow continues to generate solid cash flow

Disc: Invested

According to this article, ITC shares adjusted by Rs 26 on NSE and Rs 27 on BSE. But end of the day it corrected Rs 40.

I believe it’s the reaction from fund houses that has dragged the stock down. As far as I’m concerned, this demerger will improve ITC’s free cash flow, assuming the tax structure for the cigarette business remains stable.

The expected growth driver for ITC is its FMCG segment. Let’s wait and see how this story unfolds in the coming years. I’m not biased despite being invested—I have conviction in ITC’s fundamentals. The cigarette business remains the cash cow, and I’m closely watching how the company will thrive in its FMCG segment over time.

Disclosure: Invested. ITC constitutes around 19% of my portfolio. I am not a SEBI-registered advisor.

Hi,

The special trading session of ITC due to demerger also coincided with market being not in good mood. Today there was broad based selling which might have given more tailwind for the downfall.

If we see today’s volume it is less than 3rd and 2nd January volume so I believe the downfall might be a temporary blip. But I think nervousness will still be there for ITC till the budget event because of the fear of increase in sin tax.

Demerging ITC hotels should improve return ratios for ITC as the reinvestment of profits can be more into FMCG which is asset light compared to Hotel business and contributes more to EBIDTA. Also, the dividend payout also might improve in new future because of 80-85% profit sharing rule of PAT.

Disclaimer: Invested in ITC, so views may be biased

Thanks,

Deb

ITC hotels script in BSE website : Stock Share Price | Get Quote | BSE

strange, not sure which script it is as trade date shows as April 2005.

ITC Hotels was listed earlier before merging with ITC around 2004-05.

1980s Purchase:

In the early 1980s, ITC’s hotel operations were managed through a separate entity. Originally incorporated as Rama Hotels Pvt Ltd in 1972 and renamed Vishwarama Hotels in 1973, the company was acquired by Vazir Sultan Tobacco Co Ltd. (VST Industries) in 1980-1981. Subsequently, in 1984, ITC Ltd. purchased the entire equity capital from VST, and the company name was changed to ITC Hotels in 1986.

2004 Merger:

In 2004, ITC decided to merge its hotel business back into the parent company. At that time, the hotel division’s revenue was approximately INR 350 crore, with a profit of around INR 50 crore. The merger aimed to streamline operations, leverage synergies, and enhance the utilization of the ITC brand across its diversified businesses.

Helpful information, starts from 08:54.

Invested.

Hi,

ITC Hotels Ltd. has allotted 125.11 crore equity shares to its shareholders as part of the ongoing restructuring process. The allotment was confirmed at a Board meeting held on Jan. 11, 2025, following a scheme of arrangement between ITC Ltd. and ITCHL.

As part of the process, ITC Hotels also stated that it will initiate necessary applications to list the newly allotted shares. However, these shares will remain frozen until the listing and trading permissions are granted by the stock exchanges.

Read more at: ITC Hotels Allots 125.11 Crore Shares to ITC Shareholders, Ceases To Be A Subsidiary

Copyright © NDTV Profit

So soon we can see the ITC hotel shares in demat account, but listing will take its own sweet time.

Disclaimer: Invested in ITC, so views may be biased. Not a buy sell recommendation.

Thanks,

Deb

Anyone having demat a/c with HDFC bank have received the ITC hotels shares ? I havent yet.

Thanks!

Yes,

I have acount with HDFC and have received the shares.

I will delete this message after some time.

(post deleted by author)

Every 10 shares of ITC yields 1 share of hotels. What happens to the leftover shares e.g. if someone has 19 ITC shares ?? I did not get any fractional shares, no cash payout as well.

The value of fraction will be credited in cash to your account.

Once ITC hotels shares are listed for normal trading … all leftover (unallocated due to fractional ownership of all eligible shareholders) shares will be sold on exchanges… and then only cash payout in proportion to fractional ownership of an individual will be paid.

It’s a standard process for such event.