I will not cover what ITC does, but will straight away jump into Ratios to understand more insight about the business and recent run.

Cigarettes Business: The Engine of Profitability:

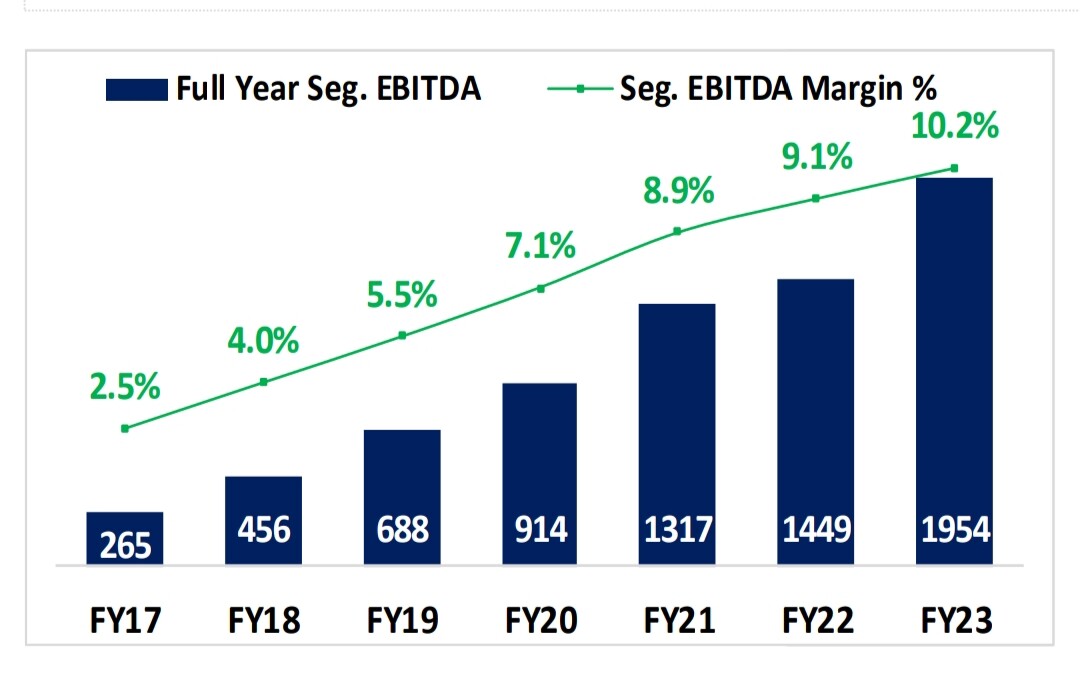

ITC’s cigarette business continues to be the primary driver of the company’s impressive EBIT margin growth. Despite regulatory challenges and increased awareness of health concerns, the sheer volume growth in the cigarette segment has proven resilient, maintaining its financial prowess within the organization. By leveraging its established brand equity and distribution network, ITC has managed to navigate through headwinds and sustain its dominant position in this sector.

Agri/Core FMCG: A Tale of Limited Progression:

In contrast to the thriving cigarette business, ITC’s Agri/Core FMCG division faces challenges in achieving a significant jump in growth. Despite its strategic foray into diverse product categories, including packaged foods, personal care, and home care, the performance of this segment has yet to mirror the remarkable success of its tobacco counterpart. Factors such as fluctuating commodity prices, supply chain complexities, and intense competition have posed hurdles for ITC to achieve exponential growth in these markets.

Debunking Misconceptions:

While ITC’s diversified business portfolio may spark conversations about its potential sources of profit, the reality remains that the lion’s share of its financial success is derived from the cigarette segment. Oftentimes, speculative narratives about alternative growth drivers overshadow the robustness of the company’s primary revenue stream. As investors and stakeholders, it is crucial to acknowledge that the key to ITC’s continued profitability lies in understanding the core strength of its cigarette business and its implications on the overall financial performance.

Lastly, another factor like not increasing the taxes by the Government on the tobacco business and volume growth in the cigarette market reflects in the recent stock run.

Let’s look at the fact below -

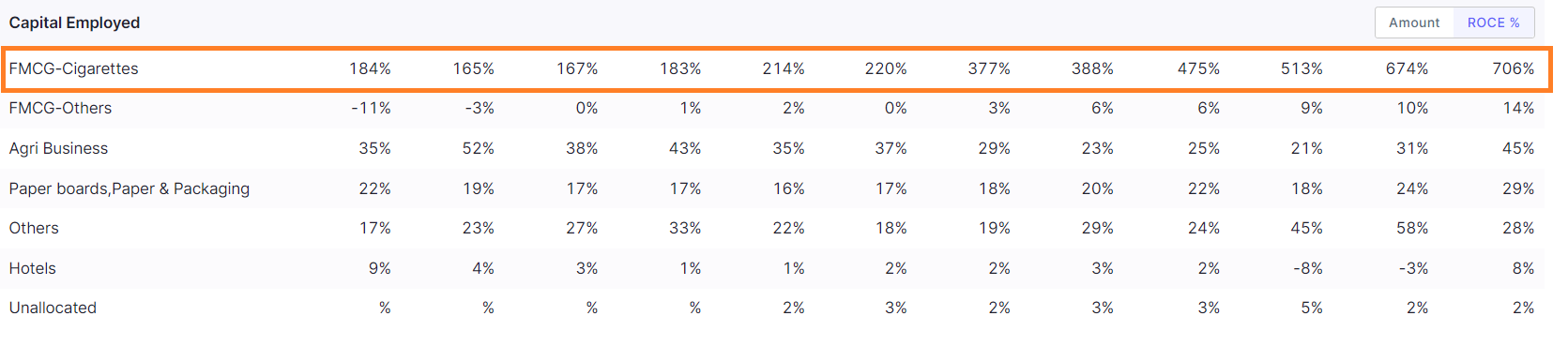

Let’s look at the Ratios and understand the importance of the Ratio:

If we look at the ratio very carefully, we see an immense jump in the ROCE for the cigarette business, have you ever thought why is that?

Let’s decode together, due to the nature of the cigarette business ITC does not need a high ROCE but due to High Asset Turnover, Margins are high, and Working Capital is low that directly has an impact on the insane ROCE percentage.

Conclusion:

In conclusion, the recent EBIT margin growth in ITC’s business is intrinsically linked to the relentless performance of its cigarette segment. As the cornerstone of the company’s financial success, the cigarette business continues to dominate the revenue landscape.