"According to Jefferies, the panel will analyse existing tax structure for all forms of tobacco, including smoking and smokeless. “It’s difficult to predict what the expert group would recommend and what government will implement at this stage,” the research house said. “However, this has clearly raised concerns on tobacco taxation in the run-up to the budget on Feb. 1, 2022.”

Operating leverage kicking in:

a. Gross Revenue up 11.1%, PAT up 13.7% on y-o-y basis

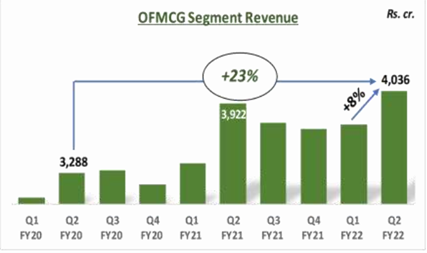

b. The FMCG Businesses delivered resilient performance growing on a high base quarter which witnessed exceptional surge in sales (Q2FY22 up by 19%). Segment Revenue and Segment EBITDA up 23% and 82% respectively over Q2FY21

Little bit concern: Rising Inventories: FY21 end it was 10397 cr. Now 11223 cr. Need to check debtors day.

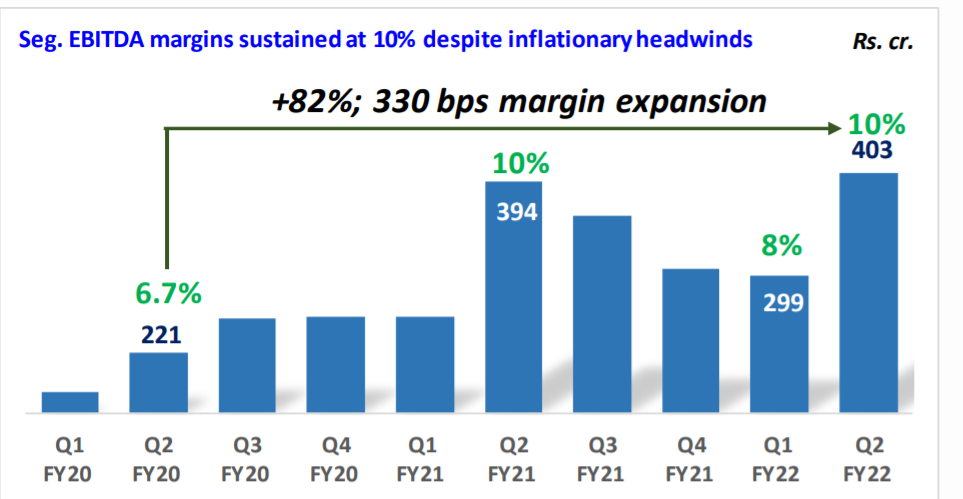

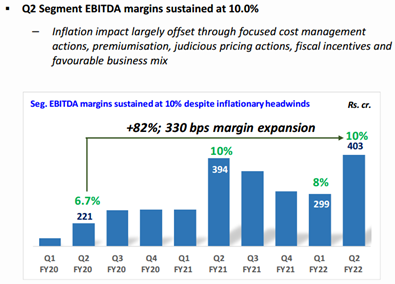

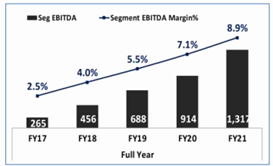

FMCG Segment EBITDA Margins sustained at 10% in spite of unprecedented commodity inflation

FMCG Others:

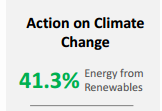

Usage of renewable energy ensures little effect of power crisis going on in India: 41% of energy comes from renewables

Disc: Invested since October 2020. Started my investment journey with this company

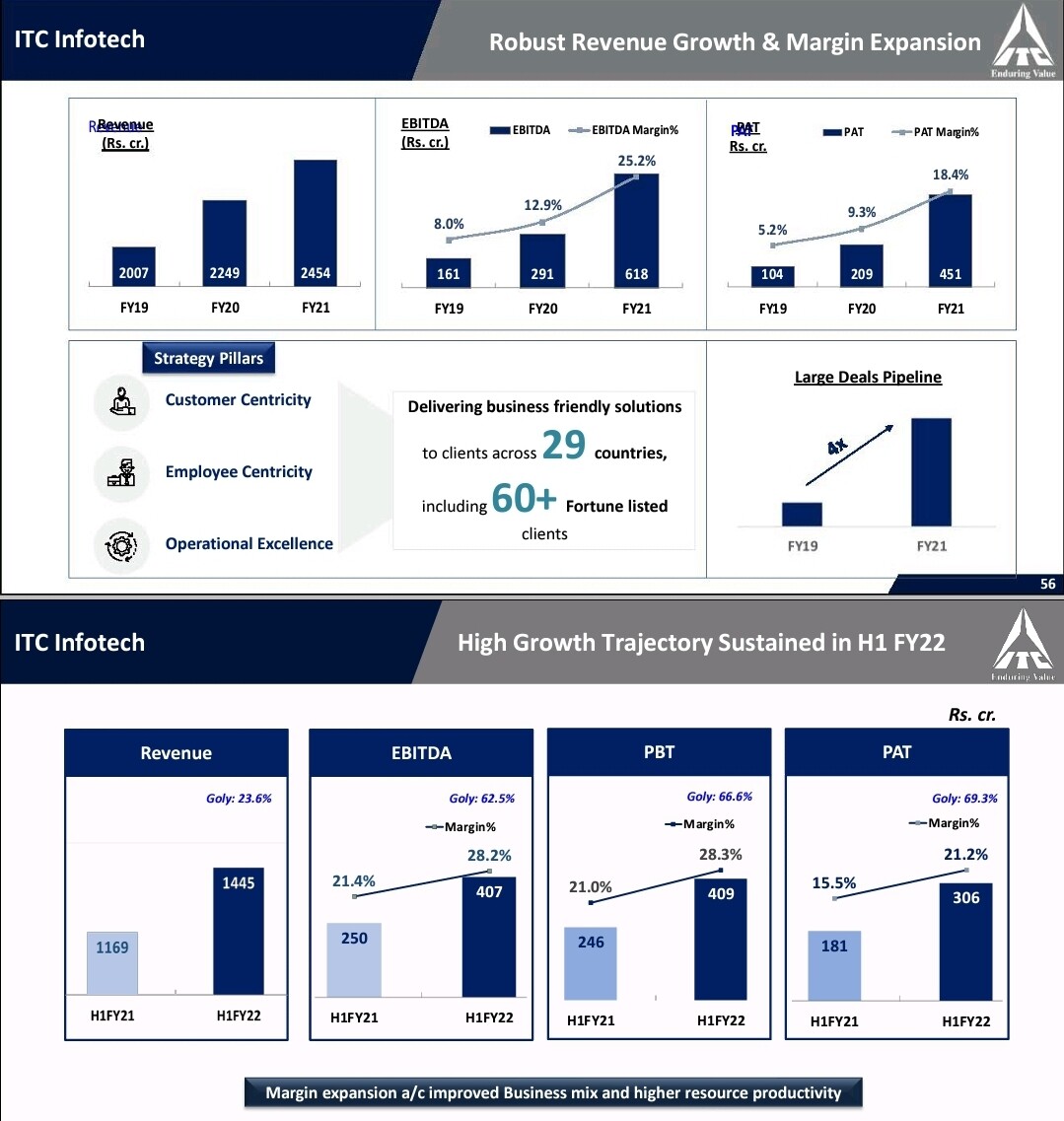

Interesting to see continued growth in ITC Infotech. It’s contribution becoming significant and hopefully noticed and recognised soon. Probably it should be a natural candidate for first demerged entity since it doesn’t require much additional capital.

Demerger or no demerger, this is excellent! Nice to see continuous increase on all parameters specially margins & deal pipeline…

Anyone aware of their client concentration and main areas of operations withing IT/digital?

Apart from the numbers and the steady growth (4x profits from 2019 to 2021), some of the key qualitative factors which are working that the article speaks of are:

Bringing in Sudip Singh as chief executive officer (CEO) - he was previously global head for the energy and utilities, and the engineering services segments at Infosys and had engineering services’ revenue from $100 million to $750 million from 2013 to 2018

Strategy of focus on business segments in which they are strong and letting go of weaker segments - looking at segments where there is apossibility to be among the top two players - presently banking, financial services, and healthcare (BFSH), manufacturing, and hospitality

Focusing on large deals (25-30 Cat A clients) - earleir the focus was on more deals, invariably small ticket size. Large deals improve margins as well

The bottom line for IT is competing with FMCG others for being the second largest contributor for ITC.

It is time that ITC refocuses on Infotech and contributes equal resources as FMCG others.

A few acquisitions will also go a long way in augmenting this sectors’ revenues in the immediate future.

This arm should not be demerged unless topline and bottomline are comparable to the likes of Persistent, Mphasis, Mindtree and LTI (midcap space). The same strategy that L&T utilized. Its shareholders are a happy lot right now. This will ensure healthy returns for the shareholders of ITC.

just my 2 cents.

discl: invested and not giving any recommendations to buy/sell.

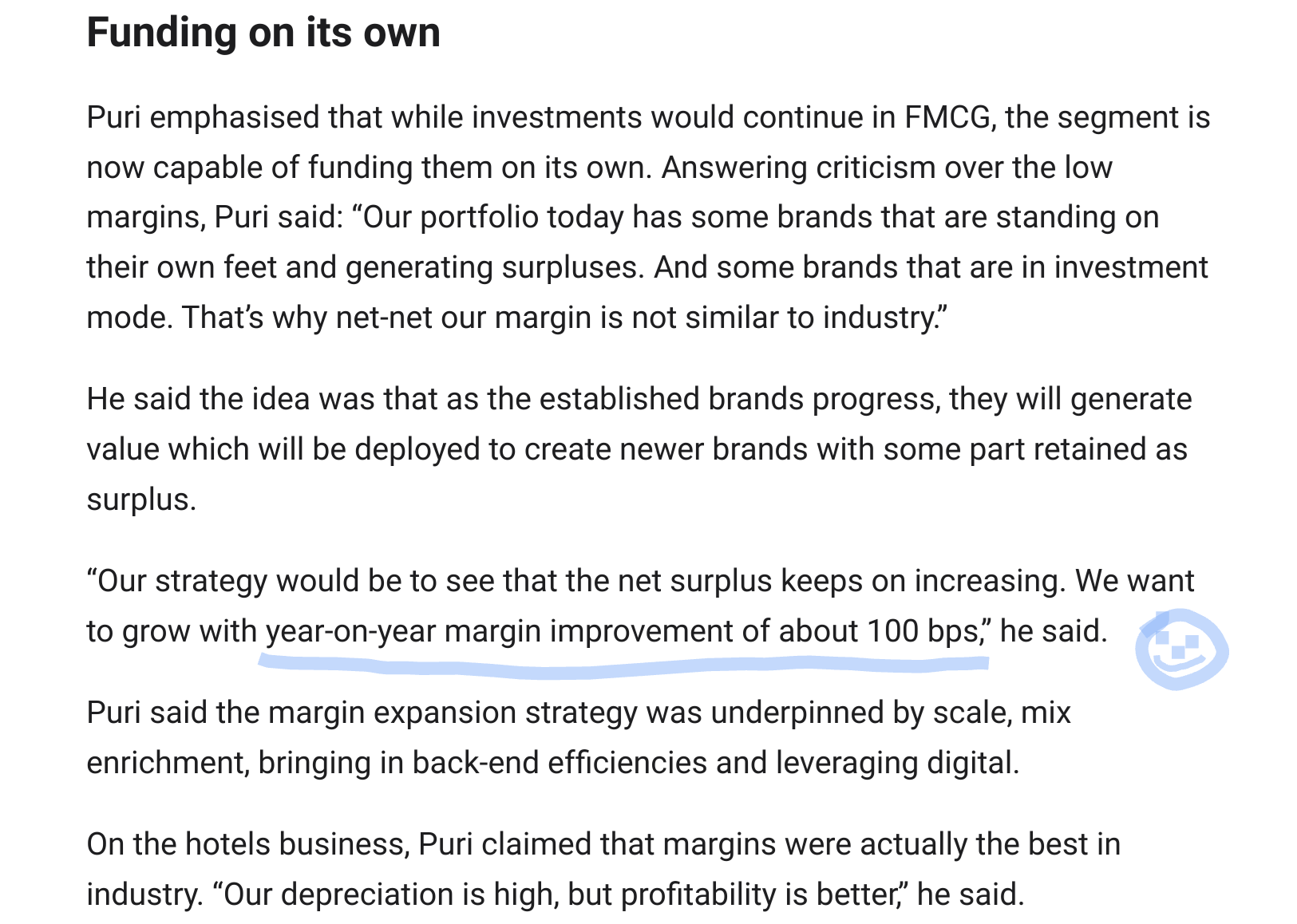

ITCs management not having to do concalls is considered bad by many shareholders but whenever they do speak to the media, you really get a hang of their gross incompetency and lack of hunger. Here’s an excerpt from Mr Puri’s latest interview with the BusinessLine

For folks wanting to see 20% operating margins in FMCG, kindly wait for another 12-15 years

There’s also a mention that ITC has the best margins in the hospitality segment as well. A basic check on screener shows that Indian hotels had OPM ranging from 16-22% between 2016 & 2019. If he’s taking only 2021 margins, this statement would be a sick joke.

While the interview had many good insights, it also contained the usual “aha moments” we are accustomed to from this management. He says that the ROCE has gone up 1100bps from 2017 to 2021. Infact, it’s the other way around

For me, this one answer (kudos to Interviewer for asking such a succinct question) wraps it up. Only the CEO can understand/ explain which hotel brand represents what, for me as a customer, I am just confused.

The ease with which he explained those 6-7 brands, seems to be that they don’t know that customer likes it ‘simple’. Taj means luxury and Lemon hotel means Budget. Why to have 6-7 categories one above and below each one. And this is a business no shareholder likes, but you are offering a bouquet with no real difference for the customer.

Even if you don’t buy property, there is huge investment in terms of Interiors, Staff training etc. And you will have to do it differently for each different category of hotels (that’s my understanding, pls correct me if ITC does it differently).

ITC had 4 traditional brands … This are based on historical classification of travellers

Luxury Collection - International who recognised international brands and move as international travel loyalty points - This was for top end international travellers

India specific 5 star hotels - welcomhotel - This compete with India specific 5 star brands

Fortnue : Budget hotel like Ginger , Taj & Lemon Tree

Historical Hotels - Haveli , Palace etc … for tourist at historical places

Now they have 2 more brands Mementos ( unique but not necessarily Historic ) and other basis Travel experience - service focussed rather than property focussed

Thank you for the details.

The link for the full article is below

Here I want to make a point regarding listing of different business. If I am not wrong, earlier management’s logic for not going ahead for listing was FMCG business not generating enough cash flow for its own growth. From the above interview it is clear that FMCG business is now big enough to stand on its own foot.

Even in the article there was a direct question of listing of ITC infotech but no concrete reply regarding that. Want to do a simple comparison for the ITC infotech with Tata Elxi (though not an apple to apple comparison) being not big enough to be listed.

If I see the financials of ITC infotech its revenue was 2454 crore(Fy21) which is more than Tata Elxi(1826 crore) and EBIDTA of 618 crore compared to Tata Elxi’s 522 crore for FY21.So in my view the logic of ITC infotech not big enough to be listed doesn’t have any significant logic.

ITC may have a bigger expectation for ITC infotech. There could be the consistency of revenue for 4-8 quarters should be about certain crores. It shouldn’t be transitory revenue due to covid. We may not understand all the things but definitely, management must be aware of it.

Before ITC Infotech listing proposal becomes reality, the below events are likely to happen:

Rebranding of ITC Infotech. The company may get rechristened with a more apt name.

Bringing in strategic investor(s) into ITC Infotech (could be a PE firm or some of their big clients). One of the example of this kind of scenario is Cyient (in which some of its major clients hold stake). This way can help BAT to exit from ITC Infotech which is not its core business.

ITC infotech is aiming for 3000 crore revenue this financial year.A jump of around 23% from last finance year’s revenue.Intrestingly company seems to be looking for inorganic growth opportunity even in the current market of hefty valuations for most of the IT or tech companies with backing of management of parent company(ITC).