The company originally known as Principal Pharmaceuticals & Chemicals started manufacturing Beta Blockers (Chemical). Considering the environmental issues the plant is shutdown for 2 years then company became sick and plant was shut down there after. Only back in 2012 company came out of sick and changed path from chemical company to digital marketing and ecommerce business. Promoter Pradeep malu is a ecommerce professional since 1999. The chemical plant sold for 3.5 crores in May 2014. Currently promoters hold 60% of stake in the company. Company recently allotted shares to promoter related parties@24 rupees.

Business model:

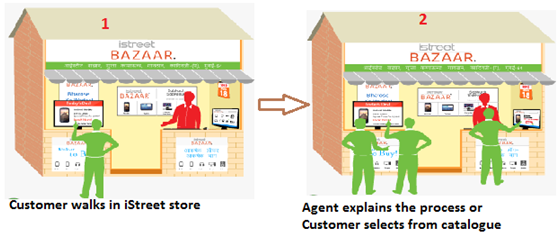

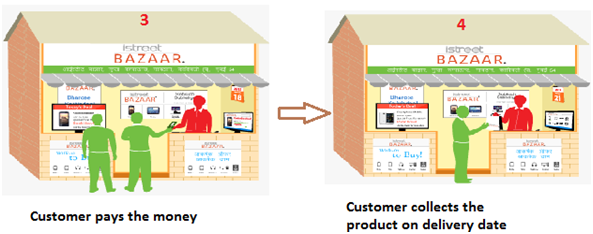

‘iStreet Bazaar’ is India’s 1st Internet Retail store, which is simple ecommerce business and easy to understand. A picture can depict 100 words and so the neighborhood iStreet business can be

seen in below fig

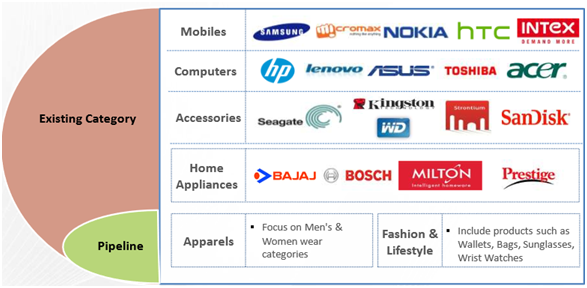

Product portfolio

Business scalability:

Key things to be considered

The uniqueness of istreet business is neighborhood store and seller trusting.

The main advantage of the business is payment first and delivery next.

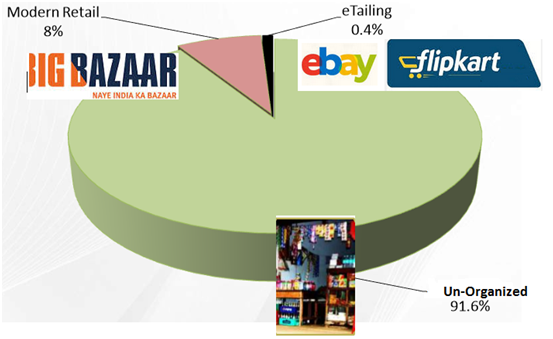

Company is focusing tier2 and tier 3 towns/villages where e-commerce still untouched mostly even by giants such as Flipkart, ebay, amazon and snapdeal (However this one can’t be comparable with those biggies considering their turnover, maturity and wide product portfolio). They are purely ecommerce versus iStreet’s neighborhood store.

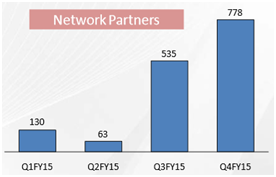

Initially company targeted to create 1100 network partners by 2015 March, they achieved the target 35% more by opening 1500+ stores. Company plans to create 3000+ network partners by current year to increase the topline.

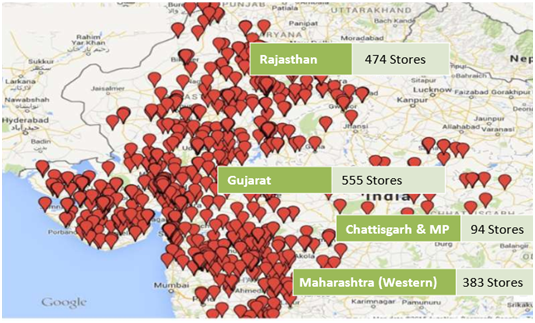

Current network partners stands at 1500+ spread across Maharashtra, Gujarat, Rajasthan, Chattisgarh and Madhyapradesh.

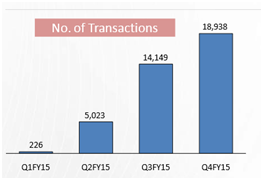

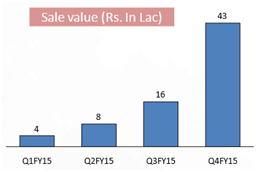

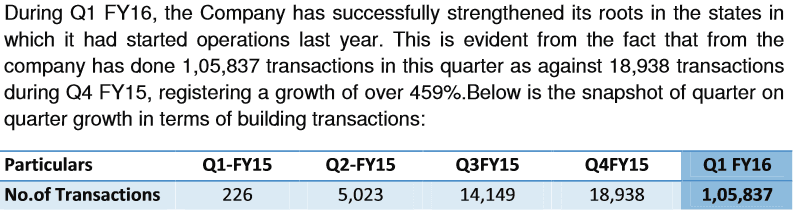

During Q4-FY15 istreet Bazaar achieved 18,938 transactions. This is equivalent to the transactions done during the whole of 9 months of FY15.

With stores ramping up and transactions soaring easily we can expect 2x-3x revenues more of last year.

Company plans to add fashion and lifestyle category to product offerings, which will improve the gross margins further.

Chances are also there for a takeover by any existing giant such as flipkart or snapdeal or some other.

Company invested temporarily 75lakhs for short term debt funds with a view of further expansion in business volume.

Negatives

Company Promoters don’t have proven history in this business.

Current market capitalization is very high compared with sales. But in next 2 years easily this will change considering the PAN india opportunity.

Future Growth:

Current business turnover is miniscule the growth phase can easily be sustained for next 3 years at least.

My View is biased because of personal holding : Since business growth is at nascent stage company can clearly outperform in the next 2 years horizon on the sales front. Stock is currently trading at 24 rs levels and request to know other side of the story by senior members.

When Internet & Smarphones will penetrate 10-15 years down the line, why someone will buy from iStreet and not from Flipkart or Amazon directly?

What is their Business model and arrangement with Network Partners?

They only earn affiliate commission on sales?

What is their Business model and arrangement with Suppliers or Brands?

How do iStreet earn? Profits on Selling products? Who delivers the product? How the inventory is managed? Who owns them? Whose money is invested in Inventories? What are the terms with Suppliers?

What is the practical maximum sales capacity per store?

How much time it takes to convert a customer? Accordingly, on an average how profitable one store can be?

One observation is that, Their No. of transaction is increasing rapidly but per transaction amount is decreasing. I mean to say, their sales are no increasing in the same speed as the transaction. There is a substantial difference.

Conclusion:

I will wait some more time and will research into this. The basic worry is what will happen to the business 10-15 down the line.

@chaitu: Very interesting business model. Went thru their presentation and company website.

We are talking about a number of new stores here. Looking at the company’s b/s, these stores must have been opened by Franchisees? - No rent nor employee cost - looks good

Goods are picked up at store - No overheads in the form of delivery expenses again. We are talking about lesser over heads here. -> Looks good

Inventory - Typically as with any e-commerce business model, this company also doesnot have to own any inventory -> Correct me if I am incorrect.

We are talking about asset-light business model here. Sounds good so far.

One question as of now(will have more in the next few days) -

it seems to be quoting at crazy valuations.

Mcap of abt 58 cr.

sales of only abt 1 cr ( 95 lacs)

cash of 1 cr, negligible investments.

Even if we assume that sales will grow 10 times to 10 cr in 3 years, assuming a NP margin of 5 % , i.e 50 lacs, and PE of 30 gives a Mcap of abt 15 cr in 3 years.

The business model seems to be good and is following an asset light model but the company is in expansion phase so the profits may not be there.

I feel the valuations are pretty high to justify any further digging.

@ravimba31,

Yes the business is very interesting, Your reply covers the basic questions raised by @mihir23192.

W.r.t Customer Stickyness my view as follows.

Their targeted customers are from villages and Talukas, where trust plays a major role. Since the Network Partner is placed in the neighborhood they will have product guarantee first upon delivery if the quality is not upto the mark, company returns back it to the vendor and returns the money to customer immediately, this will make customer more happy.

Company every day gives some freebies such as soaps,memory cards, gas lighters etc at discounted prices which will give good impression and make the customer to think of repeated buying.

@manishinlucknow,

Yes your observation is correct and that’s the reason why i stated it as one of the negative. But we need to think on these points as well.

it is the only listed player and as we have seen many cases where they attain premium valuation.

As Peter Lynch says “Company business is in nascent stage” and it can grow multi-fold with out any obstacle in next 2-3 years.

Company did pilot project from Maharastra and sold 40 watches in 5 hours duration. Then they implemented the project in Maharastra and replicated the same in Gujarat,Madhya Pradesh and Chattisgarh. Now it just needs copy paste the business from north india to south india. So the success story is easy to replicating the business in other parts of the country.

Considering the December equity/warrant allotment to promoters/non-promoters @24 rupees(20 premium + face value 4 rs), i considered there will be limited downside below these levels.

Company is a debt free and they have ready to deploy cash of 75 lakh to spur the growth in near term + 2.4crores will come in next 18months because of completed allotment as specified above.

These kind of business going forward will create more brand value and chances are also there for any biggies to acquire these at hefty valuation.

@chaitu_1614 : I have taken a token position here in this idea. Now time for some more questions to develop more conviction in this idea:

Sales/Store: As of Q4 2015(March Qtr) they have 1506 stores. (An increase of 100% from 727 in Dec 2014 qtr). Even assuming all new stores were opened in the last month of the qtr, with the total sales of 70.59 Lakhs in Q4 means sales/store of ~10,000.(7059000(q4 sales)/727(stores as of q3 end) I have excluded all the stores opened in q4 for this calc).

This # is too low to me. In a retail franchise, for a branded product, you are looking at 10-15% kinda margin. so Rs 1500 is the net earnings for a store - how will the franchise pay for real estate and employee with this earning?

Buying Habit: In a tier3 town, when you purchase a new appliance the entire family would go, visit the local appliance store, have a look and feel at that appliance before they make the decision(as purchasing an appliance is not a frequent buying process. having said this, we have seen change in buying habit as the e-commerce players offer a different form of value to the customer - which is price - that leads to my next question:

Value for the customer: iStreet is not selling anything different from a normal local appliance store. It is selling the same product. Unless iStreet offers them value by cutting down the price (compared to the local retail store), what is the incentive for the customer to change his buying habit? To understand if iStreet has room to cut down the price, we should look at the value chain and see if iStreet cuts down 1/2 levels in the supply chain.

eCommerce is about scale. Higher the scale, you will be able to run at thinner margins(even losses initially using PE money) and beat the competition out(or entice the customer to build a new buying habit). I understand that iStreet is trying do something on this by building a large network. But sales/store as of now is a big concern area for me!.

Thanks,

Ravi S

Disc: Initiated a token position as I like the idea, but I dont have conviction as of now.

didn’t get this - why would’nt a franchisee start cirvumventing istreet and start fulfilment on his own over a period of time ? He knwos the customers, knows what he wants and eventually will know the vendor who fulfils. Why bother paying istreet ?

model seems flimsy - on top of it, collecting payment in tier II /tier III cities where there is a trust defiiciency is not aan easy one. He might as well order from flipkart - which has a renowned brand name.

Overall, I think this is going to be a dud - for the record, there were such business models - a hyderabad based company called zero stock retail which did this for men’s wear and shirts that went bankrupt. In a store, a customer wants fulfilment immediately if he is parting with cash - that’s unfortunately a habit that can’t be broken easily.

In any case, I question the capital allocation capabilities of the promoters to get into this area where there are already 1000’s of well funded players - if this succeeds a little, DCM shriram’s hariyali bazaar and ITC’s ec-choupal can copy this in no time.

@varadharajanr

“didn’t get this - why would’nt a franchisee start cirvumventing istreet and start fulfilment on his own over a period of time ? He knwos the customers, knows what he wants and eventually will know the vendor who fulfils. Why bother paying istreet ?” - The franchisee cannot circumvent iStreet practically. iStreet’s value is not in the product. It is the price. An individual franchisee cannot offer an appliance at the price point that iStreet offers.

“collecting payment in tier II /tier III cities where there is a trust defiiciency is not aan easy one. He might as well order from flipkart - which has a renowned brand name.” - Note that, the customer pays for it in advance before the product is delivered. iStreet will fulfill the order only when it receives the payment. I dont see any risk here for iStreet.

But I agree with your other views:

Another observation - Just look at the snapshot from their website:

They have 3 types of franchisees - Look at the table above. I assume, looking at the sales/store, most of the stores should fall in the non-serious silver category. The mindset should be “hey, there is nothing to loose, lets just see what we can do by experimenting” - So the push should really come from iStreet to increase the sales/changing the buying habit.

Model is basically to get best of both the worlds, e-commerce plus a bit of customer/sales support. with this model you save alot on personnels and rentals. You can have presence in prime locations with small front office and storage may be in the basement.

I don’t know much about the Istreet and it’s promoters. Bases on the write up here, I think the company business model is something like Argos in UK. They have a catalog of all products from various companies and also keep some fast moving items. People go through the catalog and select the product and pay for it at the counter. If the product is available it is delivered immediately otherwise sales person gives approx deliver date for the customer to come and pick it up. The cost of the product is attractive as the store space is usually small without much inventory overhead.

This is around six years - now the things would have changed. Please check Argos website www.Argos.co.uk

@ravimba31 ,

Management is good in sharing the info and clarifying the retail investor doubts , see the reply from company to some of my questions.

Please find answers to your questions in italics below :-

Can you elaborate on who is delivering the product, profit on product and about inventory management: The product is delivered to our iStreet Bazaar stores by using courier companies. We work on ‘store pick up’ model where the buyer picks up the delivery from our store. These are neighborhood stores and from where where the buyer had booked his order. Gross margin on the

products depend upon the category. The project envisages ‘vendor managed’ inventory model where we normally avoid taking position in the inventory.

2 Once the store matured to 20 lakh revenue, how much profit the store can contribute.

As covered in the answer in point #1, our gross margin is % that varies upon the category and products.

How much Company profits are dependent on sales commission. Presently, our model works on trade margin and not on commission.

My analysis:

For 18k transactions company reported 52 lakhs as turnover thus avg ticket size comes to 270 rs. Current qtr with 1lakh transactions with lower estimation of 200 as avg ticket size sales should be reported more than 2 crore for Q1 versus 1 crore sales last full year. Anything above this figure will be good.

Management targets 16lakh transaction in current year.

Even if they really achieve 10lakh transactions which translates to 20 crores as sales (20 times of last year sales) with lower estimation .

Company last year targeted 1000 network partners and achieved 1500 stores ,Current Q1 is completed only day before yesterday and management immediately shared the details, so good to see an active management.

Management says “Phased growth” so this year we should get more clarity in turnover front.Company is clearly in growth trajectory of phase 1 according to peter lynch.

Let us wait for Q1 results to get more clarity on sales front.

Disclosure : Initiated tracking position at 25 levels and analysis is biased.

@Chaitu: Thank you.

I have an interesting idea to find out the veracity of the information posted. I am planning to talk to some network partners (who have franchised) and understand their feedback on sales. Talking to a sample, would help us understand on the ground scenario. I am planning to talk over phone, although, some folks in Gujarat can help us out on this.

Thanks,

Ravi S

Disc: Have ~1% position only to track this.

I have collected some 10-15 iStreet outlet store contact numbers(already have) and I am going to talk to them about how is the sales going on, their margin,etc.

I spoke to iStreet today saying that I am going to set-up a franchisee in Maharastra(I had to take this risk). Currently, they support franchisees in Maharastra, Gujarat, Rajasthan, Surat, MP. They said their franchisee head will call me back within 2 days with more details. I have asked them to provide me with 2-3 contacts with whom I can speak to and understand about sales, etc.

This approach is something similar to how Peter Lynch explained in his book “Beating the street” to track Bodyshop stock. To understand the sales, speak to the franchisee owner. Although iStreet is NO Bodyshop, to understand ground realities by speaking to Franchisees makes more sense in this case than Bodyshop(because here u might have a lot of research agencies tracking this company)

It might take a few days before I post my findings. I will be happy if someone can volunteer and help me with my findings. Bigger the sample, better the analysis.

I must admit, with my broken hindi it is going to be interesting, when i speak to them, but I am sure I will manage

Thanks,

Ravi S

Disc: Have ~1% position only to track this.

M’cap 80 crs sales 1 crs promoter integrity suspect earlier this was a api co - auditor qualifications in quarterly accounts-overall avoid for me stock may go up but cant bet big in these type of stocks too risky i feel-personal views do your own diligence

I had stopped researching in detail this temporarily due to workload. But I did follow their investor presentation report(after q1) and recent announcement(on Aug 19th) that they have crossed 1.7 lakh transactions in July itself compared to 1 lakh transactions in q1. There has been significant store additions too in July. This story looks too good to be true.