Ishita Drugs is undertaking a major expansion - increasing capacity from 2.5 MT/month to 23.9 MT/month.

The promoter has been actively buying stock. In fact, they purchased over 25,000 shares in a single day this month, which amounts to about 0.80% of the company’s equity.

On June 13, 2025, the company informed the BSE that it is moving ahead with the expansion plan.

They are also required to complete the implementation of the revised Schedule M (Good Manufacturing Practices provision) by December 2025.

https://www.pib.gov.in/PressReleaseIframePage.aspx?PRID=2102291

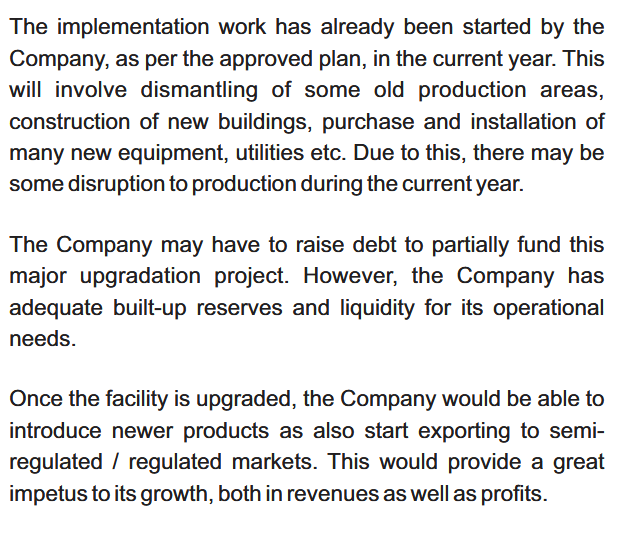

The company is currently debt-free, though management has indicated they may take on some debt to fund the expansion. They remain optimistic about the company’s future.

Here’s a screenshot from their latest annual report:

The company has listed 32 chemicals for which it is expanding capacity here:

https://environmentclearance.nic.in/DownloadPfdFile.aspx?FileName=zr7TjzSI2f5qdMLeJ6JrvC9uFQHa3DHz0LdeoEC7xiW4E7GYUAI1gmVIZjkHbTbGt7rGt2JPSff5h4gJyG72/Q==&FilePath=93ZZBm8LWEXfg+HAlQix2fE2t8z/pgnoBhDlYdZCxzXTbTpOQqzWjBW0IF63rxBVcDlG0LKdfbGNs0Ou/TEvAA==

What I like about this company is that it’s debt-free, and many of the chemicals they produce have applications across diverse industries. Even factoring in liquid assets, their balance sheet is clean. The fact that the promoters have been buying their own stock also inspires confidence.

That said, the company’s track record is less than impressive. Sales have barely doubled in the past decade, and it’s still run as a family business by a father–son duo. I’m not entirely sure they have the capability to manage a tenfold expansion and scale operations to that extent. Even when profitable, their operating profit margin has stayed in single digits - perhaps economies of scale could improve this. This is a microcap, with a market cap of around Rs.25 crores. The promoters have a 50% stake. As per BSE, they have not given a dividend in recent history.

I’ve also noticed their recruitment ads frequently on job portals, though their employee expenses look stagnant. Maybe they’re gradually building their team, which would be a good sign.

What do you think? Can this company really deliver on such an ambitious expansion plan?

A few key questions arise:

-

What is the current demand–supply position for these products?

-

Are they profitable?

-

Do they have any kind of competitive moat?

-

Are they impacted by tariffs imposed by Donald Trump?

-

What is your opinion about the management? Profitability has been erratic.

Please guide if you are aware of chemical industry’s economics. I’m a shareholder of this company.