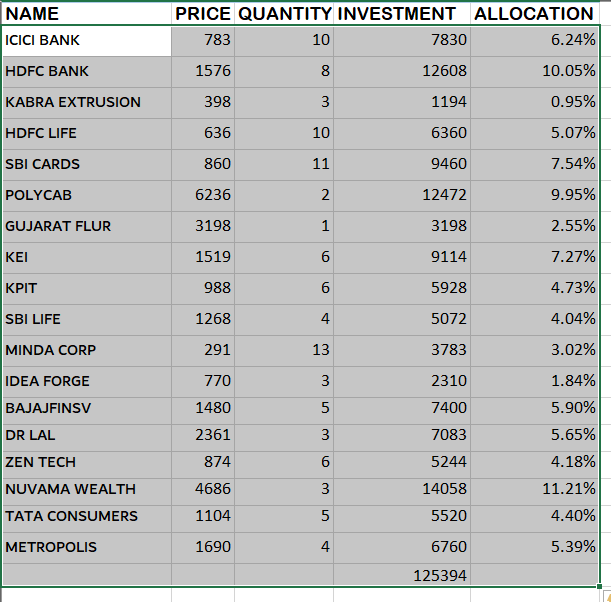

PORTFOLIO UPDATE!!

ICICI BANK

1] Avg price- 738

2] No.of shares- 8

3] Reasons- This is a part of my largecap, stable long term investment. With banking being major

part of our lives and it is unlikely that it’s significance to go down.

HDFC BANK

1] Avg price-1530

2] No.of shares- 2

3] Reasons- This is a part of my largecap, stable long term investment. With banking being major

part of our lives and it is unlikely that it’s significance to go down.

HDFC LIFE

1] Avg price- 664

2] No.of shares- 13

3] Reasons- In India the youth population and the young working class is huge and their earning potential is much better than that of the older generations. They know the importance of insurance and hence don’t hesitate to buy health and life insurance. This is a great positive for Insurance companies, who will have increasing cash flows for years to come.

ICICI LOMBARD

1] Avg price- 1145

2]No.of shares- 3

3] The general insurance sector in India is vert underpenetrated and is less than 1%. The scope of growth is huge and ICICI LOM has been delivering consistently since years in this segment.

BHARTI AIRTEL

1] Avg price- 740

2] No.of shares- 7

3] Reasons- With growing internet usage in our country, data consumption is about to go through the roof. India has one of the cheapest data plans and we have a lot of room for increasing increasing tariffs. Now we are at 2$ ARPU. I don’t see any reasons why this number won’t go to more than 4-5$ ARPU.

TATA CONSUMER

1] Avg price- 752

2] No.of shares- 4

3] Reasons- I love their products and its a company who has been successful in maintaining their market share for years. It has a range of products from necessities to luxury products. With increasing incomes we can see discretionary spending going higher. Also its starbucks business is growing aggressively. With increasing acquisition of small FMCG companies, we can see huge product diversification.

GALAXY SURFACTANTS

1] Avg price- 2727

2] No.of shares- 1

3] Reasons- This company has a big FMCG corporations as its customers. Since I cannot buy all these companies, I invested in this one as a proxy play on all the large corporations.

KEI INDUSTRIES

1] Avg price- 1067

2] No.of shares- 4

3] Reasons- With increasing number of solar farms, electrification of villages and the highest ever demand for wires from Auto industry, Housing Industry and Power companies, it has great long term earnings potential. It has strong and increasing market share and great pricing power.

KPIT TECH

1] Avg price- 564

2] No.of shares- 6

3] Reasons- The increase in spending on R&D of electric vehicles and the AD-ADAS system development and adoption is a huge a opportunity for KPIT. Their have big Auto companies as their clients who have invested heavily in this space and KPIT is a beneficiary of the EV growth and related services.

IEX

1] Avg price- 210

2] No.of shares- 21

3] Reasons- The increasing number of solar power plants will require a sophisticated market place for trading of the electric units. IEX has a monopoly in this space and with increasing solar output each year, IEX has great growth oppotunities.

TATA POWER

1] Avg price- 225

2] No.of shares- 15

3] Reasons- We all might have Tata Power for some obvious reasons so I am gonna just skip the reasons for this one.

M&M

1] Avg price- 960

2] No.of shares- 3

3] Reasons- The auto sector in India is undergoing a huge change. Indians now prefer buying SUVs rather than buying the entry level hatch backs and sedans offered by Maruti. Mahindra has an obvious advantage over other Auto companies in the SUV market because of their MOAT and huge fan following for their SUVs. With huge R&D spends and innovation in every product they launch, it’d market share is bound to improve in coming years.

SBI CARDS

1] Avg price- 872

2] No.of shares- 6

3] Reasons- Credit Card spends in India recently broke through 1.1 lakh crore and it will keep increasing. India is shifting from saving society to a higher spending society. This change will benefit the card companies. The avg spends per user is increasing annually and there is no reason for it to slow down. UPI can dent its growth a little bit, but if you want huge rewards on your shopping, lounge access and all, you will require a credit card.

METROPOLIS HEALTHCARE

1] Avg price- 1754

2] No.of shares- 3

3] Reasons- People are getting conscious about their health and preventive tests are increasing yearly. These diagnostic companies have high profit margins. Coupled with low penetration of organized diagnostic chains, we can see some market consolidation over the years.

ANGELONE

1] Avg price- 1860

2] No.of shares- 2

3] Reasons- Interest rates in India are at all time lows and with limited options to get higher returns, people have started investing actively in the markets. There are traders and direct equity investors, who trade and invest actively in the market. With investment options like the smallcase where one ca directly buy portfolio of shares which is managed by a managers, the number of investors will increase. Also the increasing positive attitude towards trading and investing will support Angels growth. Being the only listed discount broker, Angel can get scarcity premium as well.

OLECTRA GREENTECH

1] Avg price- 630

2] No.of shares- 2

3] Reasons- Their order pipeline is so strong for the next 12 months and if they are able to honor their contracts and deliver the said number of vehicles, apprx. 2100 the revenue amounts to more than 3500cr. Their revenues for this year total were less than 600cr. So if we take their EBITDA margins for this year, which are around 14%, the EBITDA on their order for 2100 busses comes to 420cr, much higher than their current 85cr. I will decide to buy more or don’t invest at all after their every Quarterly results.

LARSEN AND TOUBRO

1] Avg price- 1850

2] No.of shares-2

3] With Indian government speeding and increasing the capital expenditure every year and also the incremental business from Middle East will benefit this company greatly. Also they have made great strides in the Green Hydrogen space and I believe if India wants to become a pioneer in this space then LnT will be very important for achieving this goal.

DEEPAK NITRITE

1] Avg price- 2200

2] No.of shares- 2

3] The valuations are reasonable and it has been a compounder with steady growth for many years. The management is very confident and clean with their business. Improving profit margins and stedy topline growth will be key triggers for the stock going forward. Also they have huge capex lined up, with a view to become an important domestic producer of chemicals.

AVENUE SUPERMATS

1]Avg price - 4038

2] No.of shares-1

3] The valuations of this stock will always be really high, so instead of valuations its better to focus on the opportunity it can capture in the Indian Retail segment. Dmart follows a PRODUCER-WHOLESALER-RETAILER model of distribution and is able to provide variety of products at competitive prices. It currently has just 300 stores nationwide and its revenue per sq.ft is 20000rs. What excites me is, what if Dmart has 1500 stores in coming years and are able to maintain their revenue per sq.ft. Also their Online Delivery model has started to grow and accounts for 2% of their overall revenues. An increase in this segment will be key beneficiary for increasing the margins and profitability.

MOTHERSON WIRING

1] Avg price- 61

2] No.of shares- 27

3] Their focus on High voltage harnesses for EVs will be a growth sector going ahead.

MINDA CORP

1] Avg price- 209

2] No.of shares-10

3] Looking at the increasing interest, sale and investments in Electric vehicles auto ancillary companies with their product mix suitable to the new space will benefit hugely.

Added Minda corp and ICICI LOM and sold V-guard, Marico, HUL and some of ICICI BANK.