Maximum bank fd rate is 6.5% but is it possible to invest in some other financial product which guarantees 9% for 4 years?

Thanks

Maximum bank fd rate is 6.5% but is it possible to invest in some other financial product which guarantees 9% for 4 years?

Thanks

Yes, you can buy M&M financial 9% yielding bond.

Thanks, I don’t know much about bonds. How do I purchase them? I have a Zerodha account.

I don’t know much too about Zerodha but i purchased through IPO offering the same bond. Bond investing is risky better to buy bond funds through zerodha coin.They are less risky and can give you that kind of return.

You can invest in company fixed deposits. They offer around 8.75% to 11% based on risk profile. Again nothing is guaranteed and you could lose your capital.

But is it true that money in bonds is not compounded because you paid coupons?

You can re- invest coupons .

One option is to invest in either liquid funds or ultra short term debt funds… In case of liquid funds risk is minimal and you can expect 7.5- 8‰. With some risk, you can can get 8.5 to 9% in ultra short term debt funds…

But is this guaranteed return and is there a tax to be paid?

You can invest in 1 to 2 year fixed deposit of Ujjivan Small Finance Bank. You can get 8%.

Every investment comes with a risk.

You can try arbitrage mutual fund if you want to go tax free after 12 months.

No, it’s not risk free… But in case of liquid funds, due to shorter maturity period of underlying securities, risk is minimized… For that matter even the FD is not completely risk free… As far as, tax treatment is concerned, you get the benefit of indexation after a holding period of 3 years… Hope this clarifies…

For those seeking comfort in safety of returns, the Government of India issued 8% savings bond

While it is not exactly what the OP is looking for, I think many investors are not aware of this option which retail investors like us can easily invest in. Unlike corporate bonds and debentures, this is a ‘non-risky option’. You are counting on RBI to repay your principal and interest. I think this is as risk free as it can get in India

Thanks to everyone for sharing such excellent knowledge. And this info on the 8% govt bonds also sounds interesting. I just want to ask you experts another question. If in case you had to invest this amount for 4 years how would you go about investing it, considering your target was to get a minimum interest rate of 9% or above. I know that nothing is guaranteed but still could you please share some of your ideas.

Sir, It is really simple.

Stocks are surely Risky and No returns are guaranteed. Even the topmost companies, HDFC, TCS or Asian Paints, are NOT guaranteed to give you returns.

There has been a period of 10 years where Infy gave 3% CAGR returns

HUL gave 1.5% CAGR for a stretch of 7 years. Provided the investor held on. Most investors book loss and get out within 2 years.

In normal circumstances I would recommend Mutual Funds, but the market is so high, everything is going to crash and fall. It is likely that you will lose much before you gain a little.

Be careful. Now is not the time to be ambitious. But to only learn.

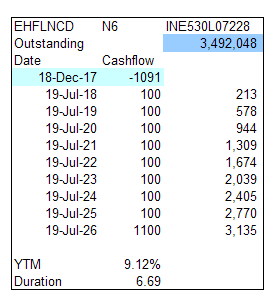

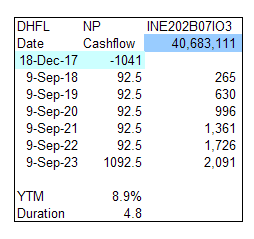

You can consider few NCDs trading on NSE and BSE that have a yield to maturity of close to 9% with duration close to 4 years.

Here are a couple I found.

NCDs come with default risk and interest rate risk. Returns are largely fixed, not assured. DFHL and Edelweiss may (but unlikely to) default in next 4 years. Price of these bonds can also drop if interest rates rise. Especially for Edelweiss, price can be lower than current price in 4 years since it will have residual maturity of 5 years. DHFL -NP has lower price risk since it will have residual maturity of 2 years (after 4 years from today).

Other similar issues I found are DHFL-N6, EHFLNCD-N5, RHFL-N6, RHFL-N8. There will many more especially from NBFCs.

Thanks for the info. Can you tell me how I can go about investing in these bonds? Also, aren’t bonds a better bet considering the stock market to be at an all time high? Isn’t the bond market inversely proportional to the stock market?

Short term bonds mutual funds should be safe enough , You can invest through Coin Zerodha.

If you are new don’t start with investing directly into bonds .

Bonds have asymmetric risks upside limited and downside 100% loss. So, go through a MF.

If you have a time of 4 yrs then why don’t you invest in equities? if you dont have time to research and look for companies try to go via mutual funds way…I think you can make tax free returns…time in market is important for equities as long as you hold good compounding/growth oriented companies…all debt instruments are taxable only equities if held more than 1yr are tax free…everyone and every anyalsts says market are high…wait for correction but markets will make new highs as economy is on a recovery path…even debt mutual funds are not tax free

Thanks, you seem very positive on the stock market in spite of the fact that nifty pe being close to 27. Any particular reasons for your confidence in the stock market?

Anyway, I think I might start an SIP in a balanced fund. Could you recommend any good funds?