Thanks to HiteshBhaias kind advice and after my own due diligence, Iave revised my portfolio as below and seek comments from esteemed fellow boarders. These allocations are as per cost price and not at CMP.

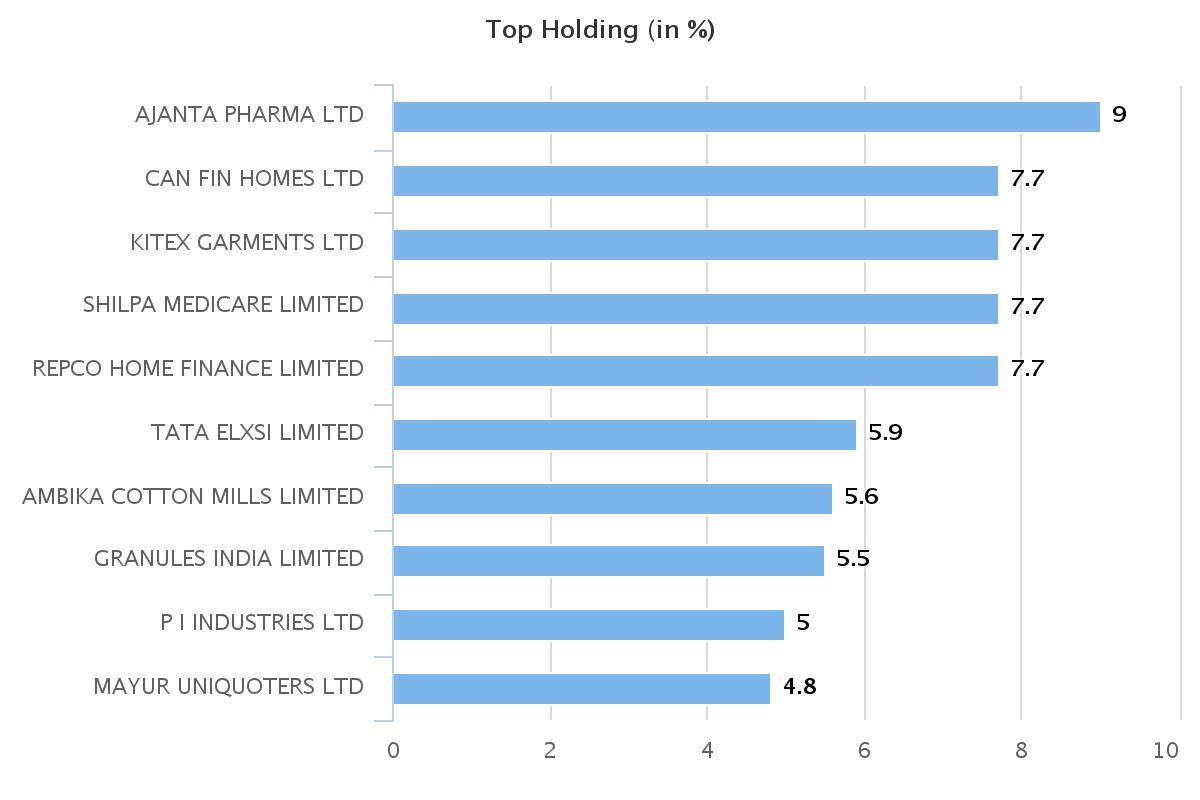

1 Repco@290 11%

2 Ajanta@974 11%

3 Kaveri@3809%

4 JB Chem@118 9%

5 Shilpa@290 6.5%

6 Pi Industries@227 6.5%

7 Alembic Pharma@199 5%

8 Polymed@327 5%

9 Muthoot Capital@83 5%

10 APM Industry@20 4%

11 Lumax Auto Tech@91 3%

12 Greaves Cotton@57 3%

13 Mayur Uni@289 3%

14 Gruh Finance@230 2.5%

15 Pidilite@261 2.5%

16 RS Software@142 2.5%

17 VST Ind@1450 2.5%

18 Accelya@560 2%

19 Amara Raja@294 2%

Total Approx 95%

Approx. 5% of stocks comprising of Dhanuka (149), Dynemic (20), Cummins India (400) and Eclerx (610).

Exited Astral, Infosys, Supreme and a few other stocks completely.

I want to add Mayur and Eclerx aggressively if there is big correction in them.

Ajanta is a recent purchase, mostly within a couple of month or so. I used to have a small quantity of it but after VPickr latest recommendation I studied it into detail and got more conviction. Stake is increased significantly in Repco, Kaveri and JB Chem. Muthoot Cap allocation in increased just before it shot up. Allocation is also increased in APM Ind, and Mayur etc.

Allocation in Pharmaceutical sector is 36.5%, which might be on higher side but I am comfortable with it. I request all for their opinion on this. My logic is that although they all are from the same sector but catering to different segment and having different kind of product range and not exposed to similar kind of business risk. While Alembic is most exposed to USFDA risk, Ajanta is in better position in this regards. JB chem is least exposed to this risk as they are well diversified and their exports are mostly to south african and south east asian countries. Polymed is in the niche business of manufacturing disposable medical devices and perhaps the only company in this segment, with a well equipped R&D facility. Regarding Shilpa, I came to know about it through Ayush blog (http://dalal-street.in/) , I studied it and convinced with the story. Many brokerage houses are very bullish on it. If it gets necessary USFDA approval it may be in different league.

My experience with equities are slightly more than two years and with this forum less than a year. But my learning graph is enhanced considerably since I joined ValuePickr. Once I used to have around 50 stocks in my portfolio but thanks to ValuePickr, which helps me to segregate the chaff, and now I have less than 25 stocks in my portfolio. The more I get understanding (of my foolishness:- )), the more I am convinced that a concentrated portfolio is desirable for a decent return. But it needs a lot of conviction, and it will come only with continuous learning and experience.

I request all and especially to Hitesh, Hemant, Surya, Rudra and Subash who are proactive in reviewing a novice portfolio; to have a skeptical look at my portfolio and comment over it.

Irshad