Does anyone have access/link to the latest valuation report of IRB Invit. In the last conf call, they had mentioned that they woudl be able to maintain DPU of 8 , even after the 2 projects go out in 2022 (based on the valuation report). However, i cant find this report anywhere on there website or exchanges.

My take on Management concall:

- Distribution likely to drop to Rs 7 post two projects are out of portfolio

- 1 Ham likely to come before these projects go out

- Company likely to go aggressive in 2/3 year time for acquiring low risk HAM projects

- Discount on NAV may remain for near future but IRR of 18% for long term investors should provide valuation comfort

Disclosure: Invested and adding on dips

3 Likes

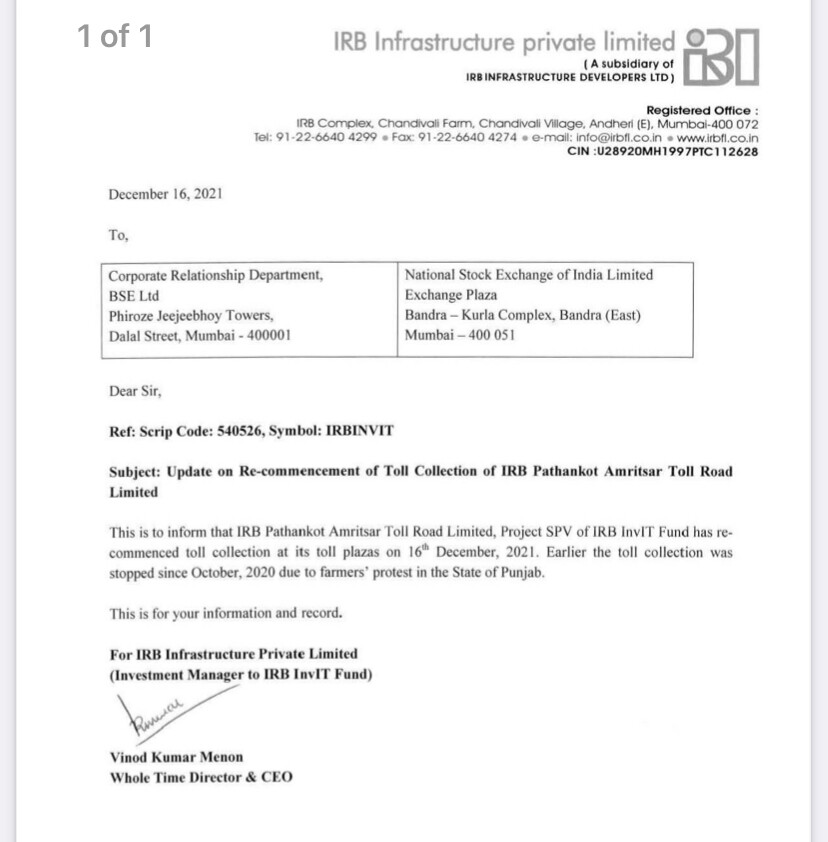

Amritsar pathankot shoudl start contributing now. Good news for IRB invit, especially since 2 projects will go out by may and june of 2022.

3 Likes

Temporary stoppage of Tolls at Amritsar-Pathankot route are not having any impact on valuation and current valuation of One unit of IRB Invit is Rs 104 as per independent valuation report shared by IRB.

Management only need to walk the talk of on boarding at least 1 HAM project in next 6 months and that may give some push to the current market price. Yield in worst case scenarios will still be better than most of other AAA instruments.

2 Likes

Most of IRB invits projects were started post 2008 and whill benefit in FY2023 from high WPI in december -in terms of hike in toll rates.

Lower maintennace spend in FY23 and FY24 (https://www.bseindia.com/xml-data/corpfiling/AttachHis/e02baba8-09e3-4354-b6d4-5846926f91bb.pdf). Page 44 of 64 of the valuation report shows that next 2 years should be lower maintennance expense.

So,it is possible that the invit gives or maintains its DPU in the coming years, due to the following:

- Higher toll rate increase in FY23, (which will act as base for FY24)

- lower maintenance capex in FY23 and FY24

- Amritsar Pathankot restarting

- Buffer cash kept to maintain DPU

- acquisiton of HAM assets

2 Likes

Thanks for sharing. Revenue should definitely increase due to increase in toll charges due to WPI and hopefully we would have a further bump up due to increase in the volume of vehicles due to higher economy activity.

Now management needs to complete acquisitions quickly which would help in rerating the stock. If acquisitions play out well we can have a DPS of ~Rs.9 per unit which would easily further re-rate the stocks to Rs.70+

1 Like

If you can help me out here, what’s the best price point to enter just going by dividend yield? At the current prices of Rs 56±, ticker is saying a yield of 14%+. How likely is this to continue given some toll roads are out of portfolio?

2 Likes

The current price is a good point to enter:

- With my limited understanding, the 2 assets going out of portfolio in FY23 is around 40-50% of NDCF (since there is revenue share with NHAI and hence gross toll collection revenue is not the right number to look at).

- Now, question of maintaining DPU of Rs. 8:

a) If you look at cash generated per unit for last 3 quarters, its is above Rs. 4 per unit (IRB InvIT || Q1FY22 Update || Total Cash Flow (for Investor) over Life of InvIT - YouTube, check around 3:45 time stamp). However, the mgmt has been giving dividend between Rs. 1.8 to 2.5. Which means, they will have buffer cash to manage Rs 8 in FY23). Remember: this was without Amritsar pathankot, whcih will truly start contributing from 2022. So fy 23 is covered in terms of DPU.

b)So, to maintain FY24 DPU of Rs. 8. onwards Lets assume the current run-rate per quarter of Rs 4 drops by 50% post 2 asset exits. the new cash per unit is now Rs 4 per quarterx4 quartersx50% drop in NDCF = Rs. 8.

c) Even if the 2 assets contributed more than 50% to NDCF, then we will have suppot from amritsar pathankot, possible acquisition of HAM asset and as mentioned earlier lower cash expense due to lower maintenance. ( Lower maintennace spend in FY23 and FY24 (https://www.bseindia.com/xml-data/corpfiling/AttachHis/e02baba8-09e3-4354-b6d4-5846926f91bb.pdf ). Page 44 of 64 of the valuation report shows that next 2 years should be lower maintennance expense.)

4 Likes

Just to add that all future projections are based on assumptions and if all assumptions come true , we are getting units at 50% discount to the NAV and a return of 14% from current levels.

Although, I invested at lower levels but still keep adding in family accounts as I feel worth the risk and valuations paid at 56 per unit.

If management walks the talk and ensure perpetuity by onboarding more value accreditive new projects , we can expect gap closing between market price and NAV

1 Like

agree entirely. at Rs. 56 and 14% yield (sustainable, in my humble view), this is as good an investment as one can get. People find it very difficult to get 14% CAGR over long periods. Here, we are getting 14% cash yield (not notional or paper profits). Also, the concern over near term drop in DPU is just too high, if an investor gets 10% yield (Rs. 5/unit) for 1-2 years and then it increases from there on - its still a great cash yield investment.

Disclosue: invested form lower levels and adding from gains made in markets

1 Like

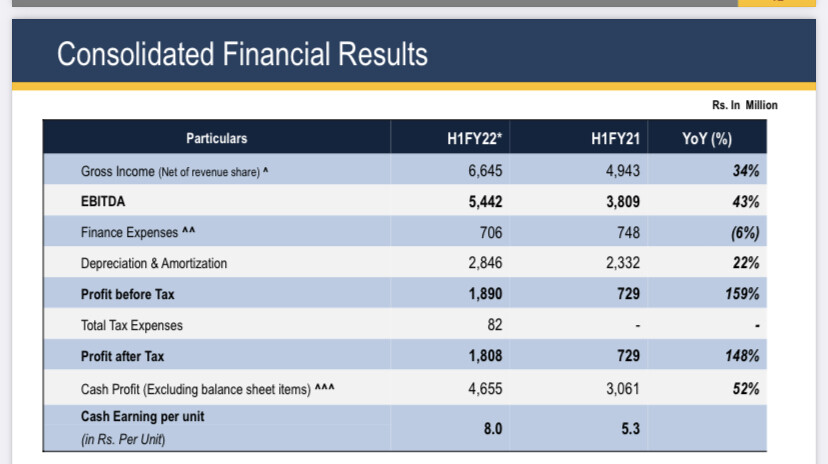

+1. They should be able to distribute Rs 8-9 dividend even after the two projects go away as they have earned Rs 8 cash per unit in H1FY22. There will also be a toll price hike starting April 1st + additional profits from Pathankot Amritsar project.

1 Like

794e7da1-2b7a-494f-a8ba-90627e3fef90.pdf (1.6 MB)

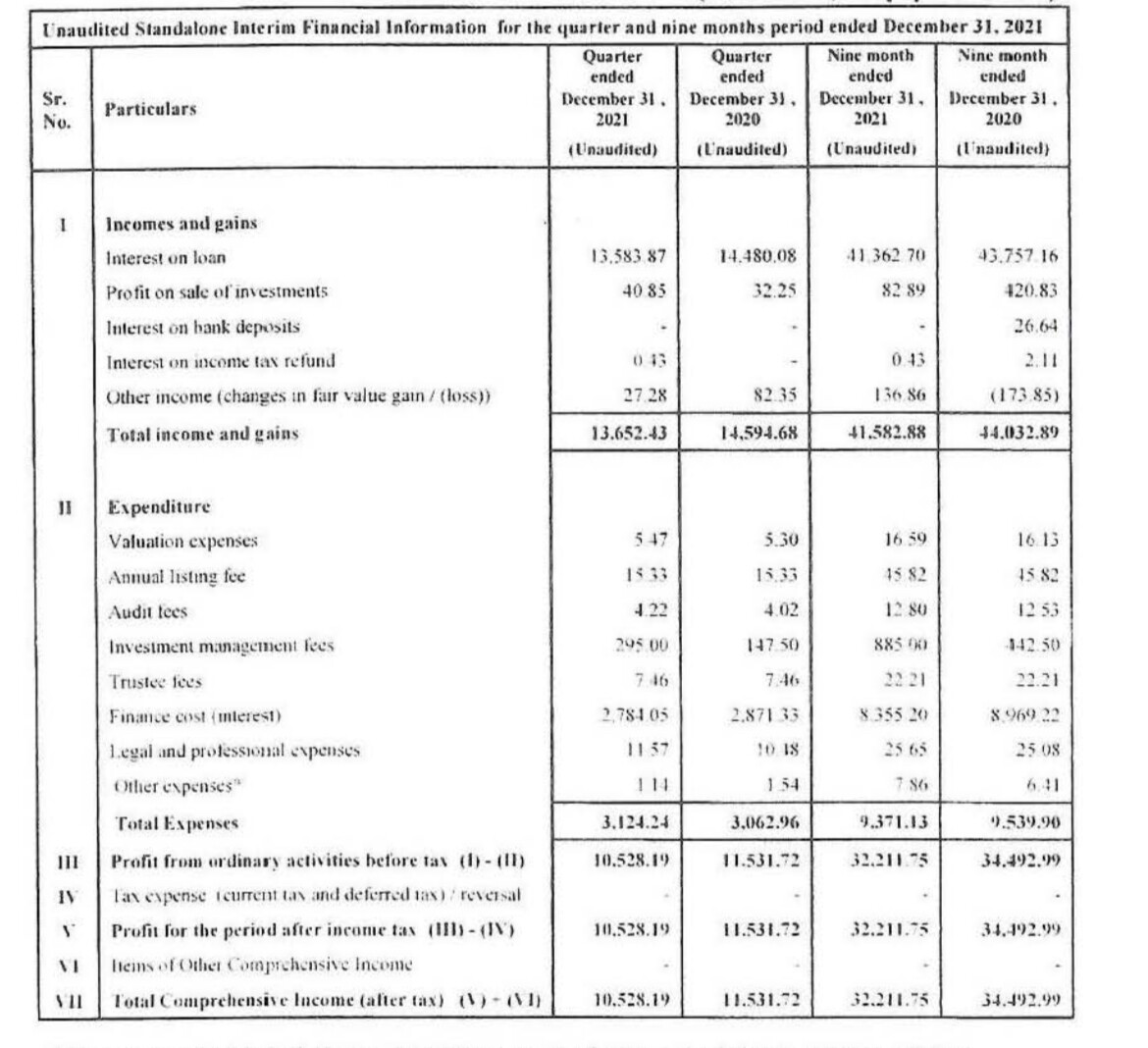

Results declared with increased distribution of 2.40 per unit and reduction of the interest costs from 7.6 to 7.25 as key highlights

4 Likes

Reported Consolidated quarterly numbers for IRB InvIT are:

Net Sales at Rs 346.60 crore in December 2021 up 7.31% from Rs. 322.98 crore in December 2020.

Quarterly Net Profit at Rs. 17.44 crore in December 2021 down 69.9% from Rs. 57.96 crore in December 2020.

1 Like

According to the management, the DPU will decrease by Rs 2 per quarter after the two projects go away in the next quarter. So, the DPU per year will be between Rs 7-9 as the management has guided. I will go with a DPU of Rs 7 till a new project gets added. They also have around Rs 150 crores in cash that translates to DPU of Rs 3.

Even if they are able to distribute a DPU of 7(which they mostly will), the dividend yield comes to around 12% which is very good.

One can listen to the Q3 concall here:

2 Likes

Yes, DPU of Rs.7 per unit is more realistic and achievable number. Further increasing it to Rs.8 per unit would require acquisitions to be completed (they would be almost 100% debt funded). Hopefully then we have the unit price increasing to early 70s (india grid is trading at ~9% yield and IRB with corporate governance issues and riskier asset class would trade at a discount of 20% so yield of 10+% is what the investors would be looking at.

4 Likes

The latest distribution includes 1.20 for interest and 1.20 for return of capital. I wonder:

- What happens if all the capital is returned. Does that means we are no longer trustees.

Disc: invested.

1 Like

Invit utilizes three methods to get cash for Unit Holders - Dividend from the SPV and via Debt servicing of loans given by the Trust to the SPV - Principal Repayment (Return of capital) & Interest Payment.

So when capital is fully returned - you don’t have debt outstanding from the Trust to the SPV. Profits can still be utilized to pay dividends.

2 Likes