Anyone have clearer ideas of HAM project cash flows. We know 40% NHAI funding, 10-15% equity and rest loan. NHAI reimburses at a growing amount per annum and interest on reducing balance is at (average) MCLR +1.25 %. Trying to get a handle on valuations…

I was going through Annual report for some info and just saw that EPC claim is part of Annual report on Page 24 of Annual . Thought of sharing on the forum as gives some credence to management .

IRB Pathankot Amritsar Toll Road Limited (“IPATRL”)

Other Proceedings involving IPATRL

- IPATRL has initiated arbitration proceedings against

National Highways Authority of India (“NHAI”) before

the Hon’ble Arbitration Tribunal. IPATRL requested to

NHAI to extend the concession period by 518 days, and

requested to release compensation of ` 252.25 crores

incurred during the extended period, as the Extension

of Time (EOT) of 518 days was duly recommended by

the Independent Engineer for delay in completion of

construction on account of the reasons not attributable

to IPATRL. However, NHAI rejected the claims of IPATRL.

Subsequently, IPATRL invoked arbitration against NHAI.

The matter is currently reserved for preparation and

pronouncement of the Award.

So the EPC claim on NHAI is disclosed ( which is an asset ). But any due to the EPC contractor is not disclosed … And it seems that has been an afterthought. Ideally all liabilities- contingent or such should be declared in the annual report.

2 Likes

There is no dispute to the fact that company is having opaqueness in between Invit and SPVs. With my limited financial ability, I can see that there is Cash held up between SPVs and DPU’s are kept on lower side. It can be a strategic call considering two main Tolls are going out next year and management can keep up DPU pace in that time with this cushion. This cash can be used in upcoming HAM project onboarding in Invit along with Debt.

Overall, market price of Invit more than captures above scenarios and seems worth investment as there is a value play for long term investors with last of Tolls currently projected for completion by 2040.

best to wait and watch if they deliver on promise of acquiring a HAM project within this financial year. If management delivers - it can lead to re-rating.

(Apology, deleted by mistake earlier)

Management in the call mentioned that this claim is nothing but a loss which was incurred by EPC contractor due to delays in construction caused by Govt/NHAI driven factors

However, two important questions to raise in this are:

-

whether the total cost of project (original EPC

contract value + cost over runs due to construction

delays) was charged to this pathankot SPV & factored

in by Invit, while acquiring. I mean Invit took over the

entire debt of SPV (including cost over runs related

debt if that was charged to SPV). If yes, than how did

EPC arm made a loss in the first place? -

since this project was acquired after the Invit listing, was this clause (of rerouting the lump sum arbitration

claims to sponser) part of the acquisition agreement?

1 Like

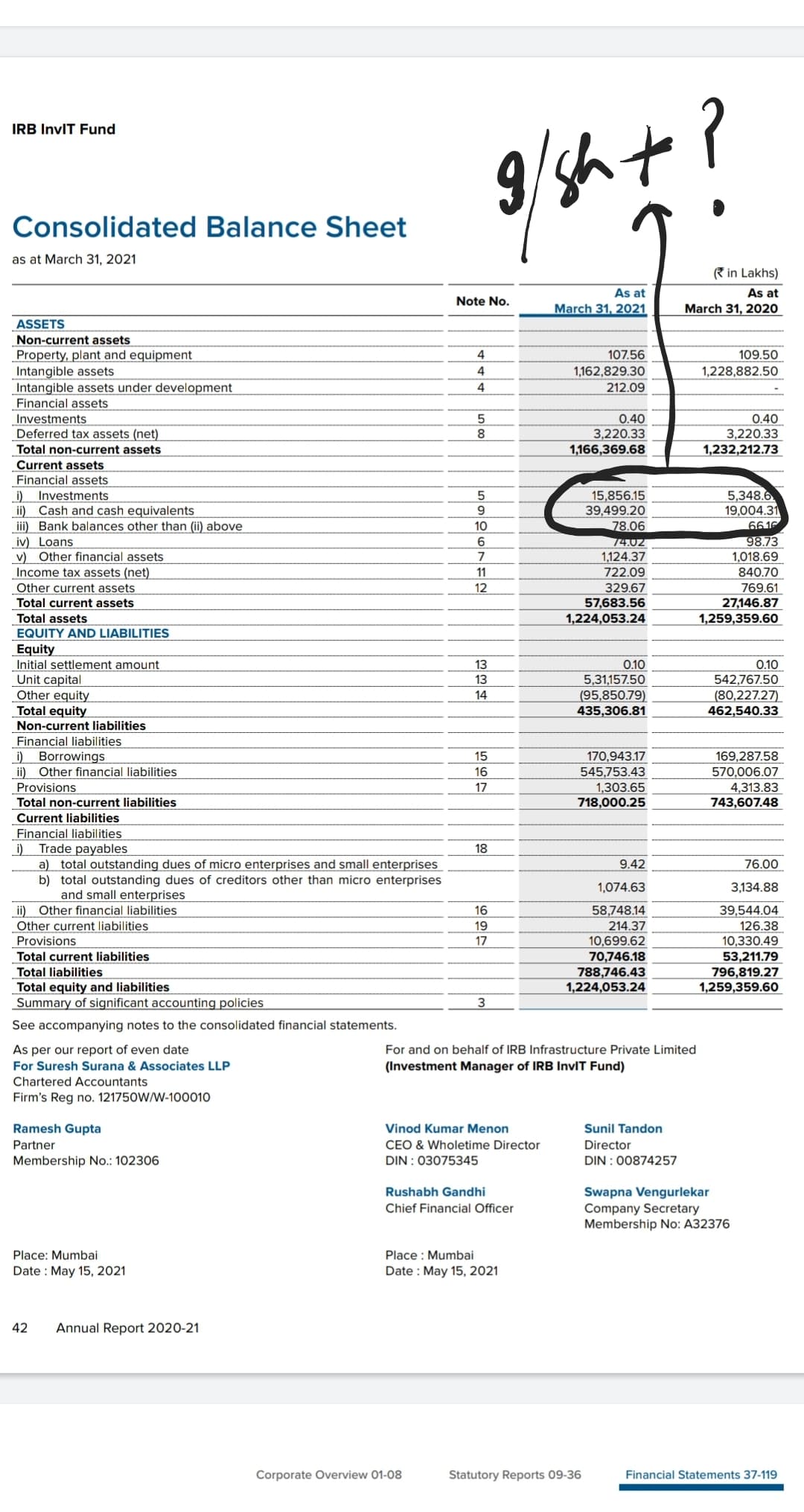

One more thing is that FY21 annual report shows significant increase in Cash & equivalents to ₹9/sh + (~₹550 crore) from less than ₹5/sh at the of FY20

However, management in the call was saying that along with ₹120crore kind of cash reserve creation in FY22, they will have free distributable cash of ₹200-250crore by end of FY22

But as per annual report, it will be 550 crore + 120 crore. Where is the gap coming from?

Or is it that they are trying to say 250 crore for distribution & 400 odd crores for equity funding of acquisition

Need to understand this…

2 Likes

You are spot bang on. And I would urge other forum members to do their own research and engage actively with management and trustees. Regarding your points here

- There is quite a chance that the earlier contract was a fixed cost contract then this over run may not have yet been accounted at SPV level. UNLESS there was a claim by EPC contractor which is not declared ANYTIME in the past.

- The important document here is the agreement to purchase the SPV by the Trust. Does it speak of any claim or cost reimbursement…!?

1 Like

Lot of this cash …say about 300+ odd crores is locked up in escrow account of Tumkur Chitradurgha SPV. As soon as the dispute resolves this money will go from IRB to NHAI as premium payment which is accounted for but not yet paid ( of this amount )

1 Like

Ok. I didnt know this. But if this is held in Escrow & belongs to NHAI, then how come they r including it in Cash & Equivalents, without disclosing the escrow nature of it in footnotes (or have i missed it in Annual report)

Part of it is countered by increase in current " Other Financial Liabilities "…

1 Like

Yes, got it. Thanks for the info

As per latest fastag collection data (accounts for 90-95% of overall toll collections now) for Sep 2021 & Q2 FY22, toll collection in Q2 FY22 stood at ₹91bn vs. ₹75bn in 1QFY22. Given 2nd wave in 1Q22, better comparison would be 4Q21, which was ₹81bn. So 2Q22 numbers are 12% growth over 4Q21.

Assuming similar growth for IRB invit, 2Q22 revenues (net of NHAI share) could be around ₹370cr (4Q21 was ₹334cr). Plus, Amritsar Pathankot was NIL in 4Q22, which should contribute another ₹20cr, leading to revenues of ₹390cr. Most of these additional revenues should contribute directly to NDCF (around 0.7-0.9/unit additional), as expenses were already there. Apart from this, stuck money in escrow, if the issue is resolved, may contribute another 0.5/unit to NDCF

In 4QFY21, company distributed 2.5/unit, which means 2Q22 distribution could be between 3.0-3.5+.

Further, if these numbers continue, for which as of now no reason not to, then recurring quarterly distribution of ~₹3 for next 2-3 quarters.

Currently market is factoring ₹8.5/unit in FY22. So, this incremental distribution, if it materialises, would be 20-25% higher than market expectations.

Also, Vadodara Kim HAM project is nearing completion. So there could be more clarity on its transfer to Invit in 3Q22…

Therefore, 3Q22 could turn out to be the rerating quarter for IRB invit. As it is, sector rotation is in full flow in market currently. All high dividend, defensive plays are getting rerated. All in all, many factors converging for IRB invit. Fingers Crossed…

Note:

I am an investor in it, so my views may be biased

I am not SEBI registered, please do your own due diligence before taking any decision

2 Likes

Please see the latest credit rating report on IRB INVIT:

Good message is that (from the report): The net toll collection which was impacted due to 2nd wave of Covid has recovered significantly during last 2 months and per day net toll collection during 5M (from April 2021 to August 2021) in FY22 neared per day net toll collection in FY20 despite nil collections from Pathankot Amritsar stretch where tolling is suspended due to farmer agitation since October 2020.

1 Like

As per CARE credit rating report, the per day collection in first 5 months of FY22 is similar to collections in FY20.

In FY20, per day collection stood at Rs3.41 crore in first 6 months & 3.47 crore in FY20 overall.

Assuming a collection of Rs3.47 crore per day in 1H FY22 (assuming September 2021 to be similar to first 5 months average), H1 FY22 net revenues are likely to be Rs635 crore, less Rs253 crore cash revenues in 1Q FY22, leaves Q2 FY22 revenues to be around Rs380-385 crore. This is similar to my estimate in earlier post a week ago.

Continue to believe the distribution could be Rs3-3.5/unit in 2Q FY22…

Please read the disclosures in my post a week ago…

2 Likes

Revenue for last quarter were 337 Crores and still distribution was made as 1.8 per unit. I feel current quarter distribution would be atmost 2.5 and cash built up at SPV/Invit level will be used for distributions in 2022 when 2 projects go out.

Even distribution of 9 on annual basis is giving a yield of more than 15% and return of capital helps in tax efficiency.

Buy and forget type of Invit for a replacement of mine debt portfolio and now only waiting for management call on additional projects and any effort for reducing interest cost.

Annual increments of traffic growth and inflation adjustment takes care of any other potential downsides from current levels.

It includes non cash item of 80 crore + from Pathankot Amritsar for past 11 months. Cash revenues or actual revenues were 250-255cr in 1Q 22. Care report clearly talks about revenues without Amritsar project. Anyway, no point in arguing, its a point of view, u may disagree.

Hi

Is return of capital means reduction of face value of unit. If so what is present face value of the unit.

With this quarter distribution it becomes 89.1